According to an article in The Economist, the value China’s outbound M&A activity rose sharply in 2016, up approximately fivefold since the summer of 2015 and eightfold above its average rate between 2010- 2015.

The article mentions that this increase could represent a troubling trend for China, of capital fleeing the country in response to its slowing economic growth rate and gradually depreciating currency in recent years.

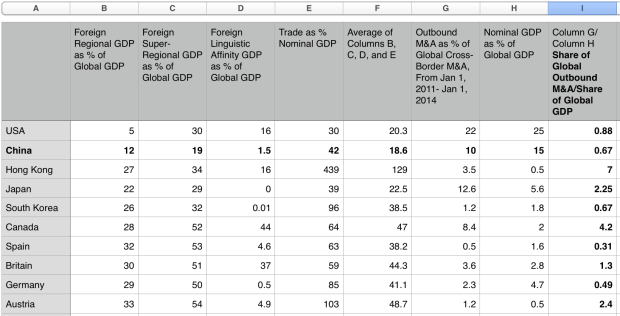

It then largely dismisses this theory, however, saying, “rather than sparking a stampede [of money] to the exits, it is more accurate to say that these changes [in China’s economic performance] have alerted Chinese firms to the fact that they are still woefully under-invested abroad. China’s share of cross-border M&A has averaged roughly 6% over the past five years, despite the fact that it accounts for nearly 15% of global GDP”.

In other words, the article assumes that, if a country’s share of global M&A does not exceed its share of global GDP, its M&A is less likely to be capital flight. This assumption is not justified, however. It overlooks other key factors that may determine a country’s propensity for engaging in outbound M&A. Such factors include:

1. A country’s physical proximity to other large economies

In order to have cross-border M&A, you need borders to cross. Economies with large neighbours, for example Canada or the Netherlands, tend to have a relatively high propensity for engaging in international M&A.Canada’s cross-border M&A, for example, has tended to be 25-50% as large as the US’s in recent years, in spite of the fact that Canada’s GDP is less than 10% as large as that of the US. China, unlike Canada, does not border any large economies. This impacts not just its M&A, but also trade: in China trade counts for 37% of GDP, whereas in Canada it is 64% and in the Netherlands it is 151%.

2. A country’s cultural and linguistic affinity with other large economies

Most economies in the world speak European languages; Northeast Asia remains something of a linguistic outlier. This may make Northeast Asian countries less likely than other regions to engage in global M&A. Japan, for instance, currently accounts for 6.5 percent of global GDP, yet has accounted for less than 1 percent of global inbound M&A in recent years, and less than 4 percent of cross-border M&A in general. Arguably, China too might be expected to have a low propensity to engage in M&A.

3. Capital availability versus investment opportunity

One of the reasons that Japan’s outbound M&A far exceeded its inbound M&A is that capital in Japan has been cheap (its interest rate is below zero), yet investment opportunities in Japan have been limited (its economic growth rate is 1 percent). Thus, the Japanese borrow money cheaply at home, and often invest it abroad. In China, however, interest rates frequently top 4 percent, while economic growth is estimated to be 6-7 percent. We might, then, expect China to be less M&A-intensive, and generate more of its own investment opportunities domestically rather than seek out ones in foreign markets. Unless, of course, as many economists suspect, China’s true growth rate is much below 6-7 percent.

4. A country’s political relationship with other large economies

Outside of mainland China itself, approximately 45 percent of East Asia’s GDP is generated in Japan, China’s historic regional rival. Outside of mainland China, approximately 29 percent of global GDP is generated in the US, China’s potential global rival. Because China’s relationship with Japan and the US is sometimes a tense one, its investment relationship with Japan and the US may be less than it could otherwise be. For instance, when a territorial spat between China and Japan, over the Senkaku/Diaoyutai islands, heated up (rhetorically) around 2012, cross-border M&A between China and Japan fell sharply. Indeed, in spite of relatively close cultural connections, Japan was not even one of China’s top ten targets of outbound M&A spending in the past decade. China has tended to invest in Europe; Japan in its political ally the US. 43 percent of Japan’s outbound M&A in the past decade went to the US.

5. A country’s relationship to foreign financial hubs

Relatively independent financial hubs, like Hong Kong, Singapore, or Luxembourg, tend to be significant net providers of M&A capital. Their outbound cross-border M&A spending tends to far exceed their inbound M&A, and their global share of cross-border M&A tends to far exceed their global share of GDP. From 2011-2014, for example, Hong Kong’s outbound M&A was about 25-40% as large as mainland China’s, even though Hong Kong’s GDP is only around 2% as large as mainland China’s. (Rightly or wrongly, M&A statistics tend to treat Hong Kong as if it was an independent entity). The fact that the world’s top two financial city-states (Hong Kong and Singapore) are Chinese may suggest that mainland China’s propensity for outbound M&A should be relatively low—just as, for example, US outbound M&A would plummet if (hypothetically) Manhattan were to secede from the US.

The value of China’s outbound M&A as a share of global cross-border M&A should, perhaps, be lower than China’s share of global GDP, then. Yet in 2016 Chinese buyers accounted for an estimated 15 percent of the value of all cross-border M&A, slightly higher than the 14.5 percent of global GDP China had. The Syngenta deal alone, announced in early 2016, was roughly large enough to eclipse all outbound Chinese M&A in any year prior to 2014. China has kept up its M&A pace thus far in 2017, not counting Syngenta.

The explanation that you often hear for why China’s M&A boom is not capital flight — namely, that Chinese firms are seeking foreign expertise and technology, as China transitions to a more knowledge-intensive economy — may have some merit, but still it ignores the fact that money has also been pouring out of China into other assets in the developed world in recent years. To take the most notorious example, Chinese capital been pushing up real estate values in Pacific cities (Vancouver, Seattle, Sydney, etc.) and hub cities (NY, London, Toronto, etc.). The M&A boom, then, may be part of the greater trend of Chinese capital seeking safe haven. China’s 2016 M&A investment in the global safe haven, the US, was roughly triple what it had been in 2015, 2014, or 2013. It was larger than in every year from 1990-2012 combined.

If much of China’s M&A boom really is a result of capital flight, it is also likely to be unsustainable. In part two of this article we will analyze China’s geopolitical structure, to see when (or whether) this boom will end.