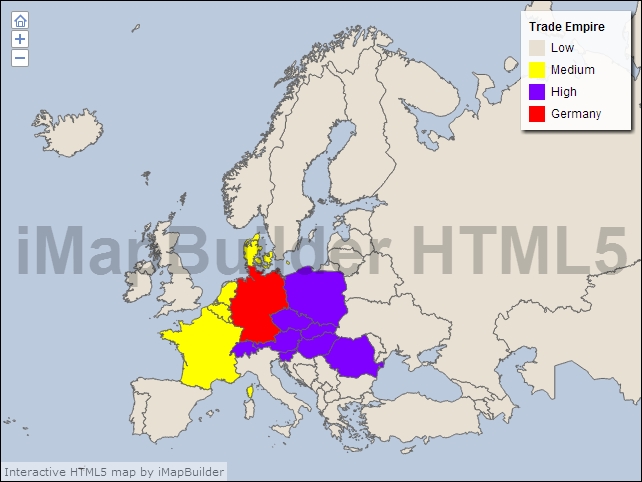

The age of formal European empires may be over, but that does not mean that nations no longer possess meaningful spheres of influence. Germany in particular retains an impressive trading empire in the heart of the European continent. This “empire” exists in spite of the fact that Germany’s economy accounts for less than 20% of Europe’s overall economic output. To varying degrees, it encompasses Austria, Switzerland, Poland, Romania, the Czech Republic, Slovakia, Hungary, and Slovenia, forming a geographically contiguous region with a population of 185 million and an economic output of about $5.5 trillion.

France, the Netherlands, Belgium, and Denmark could be said to fall within this sphere as well, albeit to a lesser extent, adding to it another 100 million people with an economic output of $4 trillion. To put these numbers into context, the United States has a population of 315 million, and China has an economic output (at least officially) of $9 trillion.

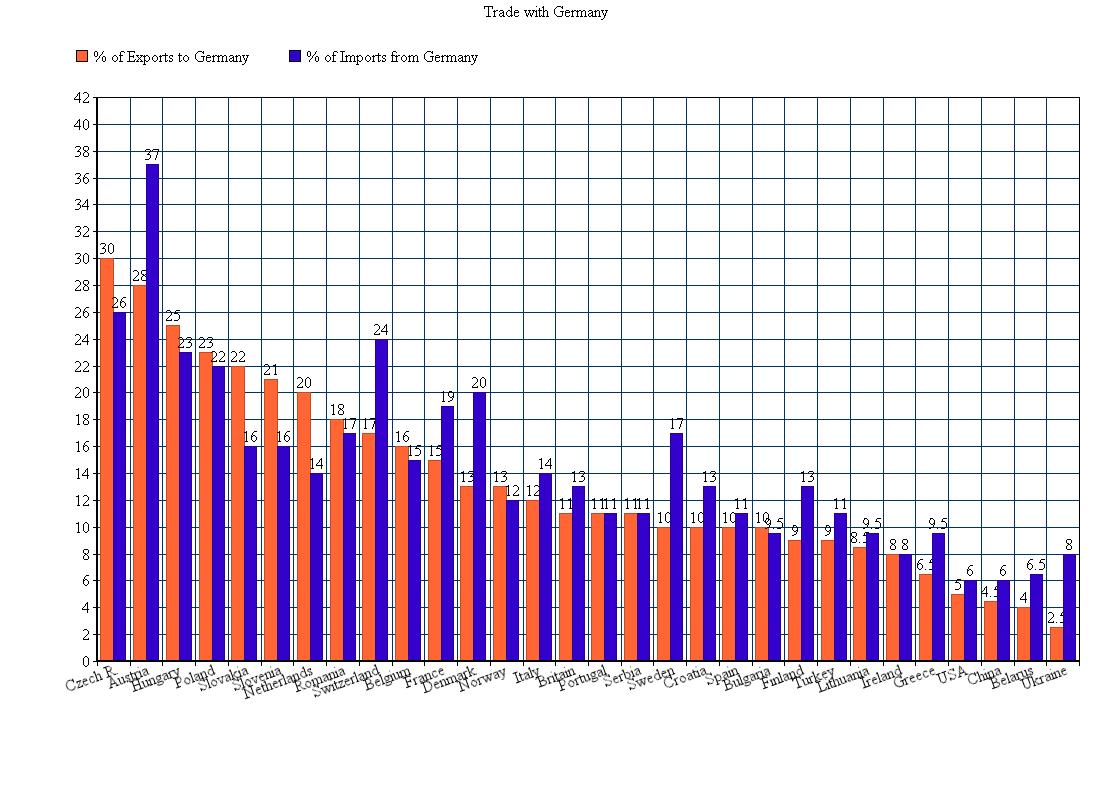

The statistics behind this trading sphere are rather impressive, considering that most of the countries within it only began trading seriously with Germany during the last two decades, following the end of the Cold War. The Central and Eastern European countries within the sphere rely on Germany for an average of 28 percent of their trade. These numbers may not be as high as, for instance, the 75-80 percent of Canadian and Mexican exports that go to the United States, but they are substantial nonetheless. By comparison, Germany accounts for only 12 percent of Britain’s trade.

None of the countries within Germany’s trade sphere have any other economy they depend nearly so much on. Their second largest trade partners account for an average of just 9 percent of their overall trade. Most of the countries in Central and Eastern Europe also trade a considerable amount with one another, such that when you look at their trade with countries that are not a part of the German trading sphere, it generally accounts for only around 40 – 50 percent of their total. This is a lot of economic exposure for these countries to have to a single bloc of nations.

None of the countries within Germany’s trade sphere have any other economy they depend nearly so much on. Their second largest trade partners account for an average of just 9 percent of their overall trade. Most of the countries in Central and Eastern Europe also trade a considerable amount with one another, such that when you look at their trade with countries that are not a part of the German trading sphere, it generally accounts for only around 40 – 50 percent of their total. This is a lot of economic exposure for these countries to have to a single bloc of nations.

In France, Belgium, the Netherlands, and Denmark, the countries located in between Germany and the Atlantic Ocean, the numbers are somewhat less decisive. France sends 17 percent of its exports to Germany and receives 20 percent of its imports from Germany. Germany accounts for about 17 percent of the Netherlands’, Belgium’s, and Denmark’s trade, with the Netherlands particularly dependent on exporting to Germany and Denmark particularly dependent on importing from Germany. In addition, these countries trade a lot with one another, so that their exposure to Germany`s commercial sphere as a whole is equal to roughly 35 – 45 percent of their trade.

Of course, not all states depend equally on trade for their economic activity (see graph below). Exports, for example, account for 75-95 percent of the GDPs of the Netherlands, Belgium, the Czech Republic, Hungary, Slovakia, and Slovenia, but just 25-35 of the GDPs of France, Romania, and all of the major European economies outside of Germany’s trade sphere (namely Britain, Italy, Spain, Russia, and Turkey). This makes countries like the Czech Republic and Slovakia particularly dependent on trade with Germany, and countries like Romania and France much less so.

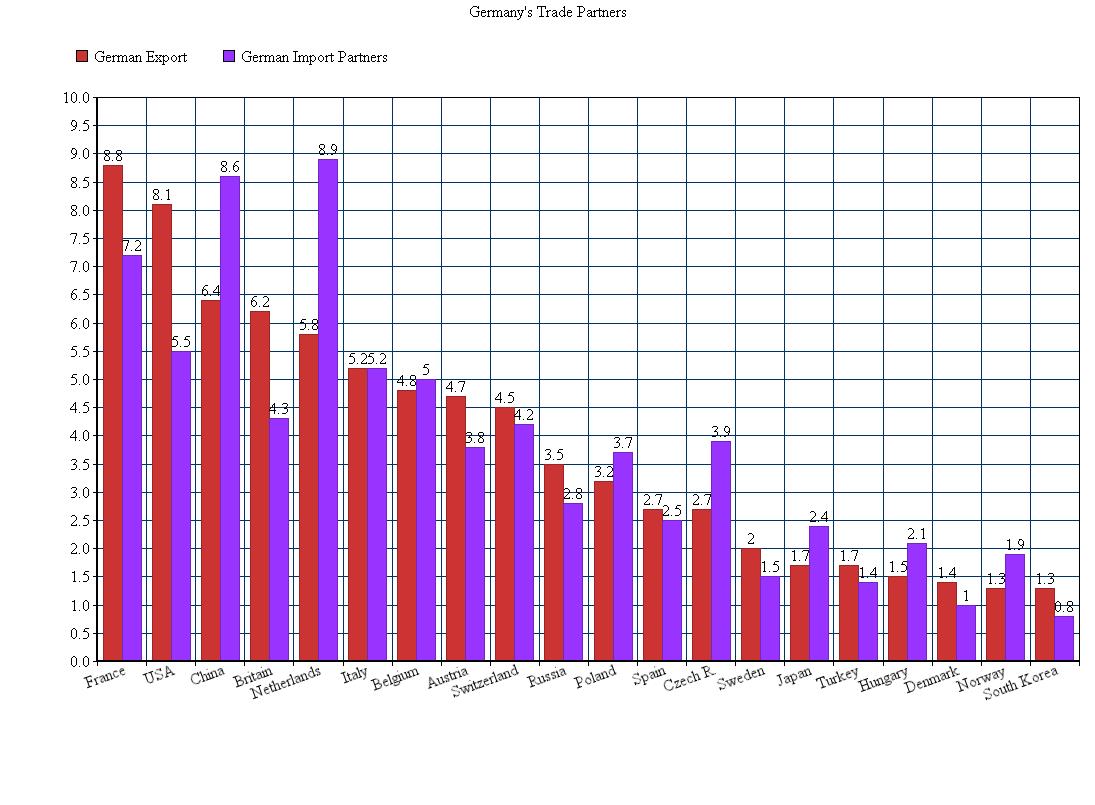

Unlike any of the countries within its trade sphere, Germany is well-diversified in its import and export patterns. It not only spreads out its trade throughout its “empire”, but also engages significantly with many different countries outside of it, such as Italy, Britain, Spain, Russia, China, and the United States. Germany’s only real trade dependence – without getting into specific industries, such as natural gas production, where it receives over 65 percent of its imports from Russia – is receiving 14 percent of its imports from the Netherlands. However, this same trade accounts for 23 percent of the Netherlands’ exports, and the Netherlands is one of the most export-dependent countries in the world, so in general the Dutch cannot easily threaten to raise the prices of the products they sell to Germany.

Unlike any of the countries within its trade sphere, Germany is well-diversified in its import and export patterns. It not only spreads out its trade throughout its “empire”, but also engages significantly with many different countries outside of it, such as Italy, Britain, Spain, Russia, China, and the United States. Germany’s only real trade dependence – without getting into specific industries, such as natural gas production, where it receives over 65 percent of its imports from Russia – is receiving 14 percent of its imports from the Netherlands. However, this same trade accounts for 23 percent of the Netherlands’ exports, and the Netherlands is one of the most export-dependent countries in the world, so in general the Dutch cannot easily threaten to raise the prices of the products they sell to Germany.

Although they need to be taken with a very large grain of salt, these trade statistics reveal a pattern that is much too large to ignore. One thing that stands out – glaringly, given the current political debates in Europe – is that this trading group barely corresponds with the European monetary zone. Poland, Switzerland, the Czech Republic, Hungary, Denmark, and Romania are all in Germany’s trade sphere, yet use their own national currencies instead of the Euro. On the other hand, a number of economies located outside of the trading sphere, such as Spain, Italy, Finland, Greece, Ireland, Portugal, and Estonia, do use the Euro as their currency.

Although they need to be taken with a very large grain of salt, these trade statistics reveal a pattern that is much too large to ignore. One thing that stands out – glaringly, given the current political debates in Europe – is that this trading group barely corresponds with the European monetary zone. Poland, Switzerland, the Czech Republic, Hungary, Denmark, and Romania are all in Germany’s trade sphere, yet use their own national currencies instead of the Euro. On the other hand, a number of economies located outside of the trading sphere, such as Spain, Italy, Finland, Greece, Ireland, Portugal, and Estonia, do use the Euro as their currency.

Countries that use the Euro:

(the graph above is a few years old: Latvia and Lithuania should now be highlighted too)

Trade with Germany:

This disconnect is for the most part a legacy of the Cold War, as the precursors of the Eurozone were built at a time when Russia still dominated Eastern Europe. Now that Eastern Europe is sovereign and commercially integrated with Germany and Austria, however, the shape of the Eurozone seems to make little sense. It actually conforms more to the trade spheres of France, Italy, Spain, the Netherlands, and Belgium than it does to Germany’s.

France, for example, relies on Spain and Italy for more than twice the share of its trade that Germany does, and on Poland, Hungary, and the Czech Republic for three times less than Germany does. Even Britain, which still uses the pound, conducts almost 10% more of its share of trade with Eurozone countries than Germany does. (Britain trades a lot with Ireland, Belgium, the Netherlands, and France, each of which uses the Euro).

One of the results of this disconnect is that even though Germany has the largest trade surplus in the world apart from Saudi Arabia, it actually buys slightly more from the countries within its trade sphere than it sells back to them. This is partly because the Netherlands and Switzerland have incredibly large trade surpluses relative to the size of their gdp’s, but it is also because Germany’s largest trade surpluses tend to be with countries which, unlike Eastern Europe, have relatively high wages and/or strong currencies, such as the United States, Denmark, and Eurozone countries like Italy and Spain.

Another thing these statistics show is that while German influence is pronounced in all of the countries within its trade sphere, it is decisive in none of them. Apart from Austria, a German-speaking state, no country relies on Germany for more than 40 percent of their overall trade, and most less than 30 percent. In contrast, if all of these countries were to band together, Germany would be dependent on them for approximately 45 percent of its trade, and more than 20 percent of its trade even if you exclude France, the Netherlands, Belgium, and Denmark.

In other words, Germany is dependent upon these countries as a group, just not (with the possible exceptions of France and the Netherlands) on any of them individually. As such, for these states to exert any meaningful leverage over Germany, they would have to cooperate closely with one another. Within Eastern Europe, the only country that could potentially provide enough leadership to promote such cooperation is Poland.

Poland is by far the biggest of the Eastern European countries in the grouping of states that are heavily dependent on German trade. Poland’s gdp, at around 515 billion a year, is not much smaller than the combined gdp’s of Romania, Hungary, the Czech Republic, Slovakia, and Slovenia. Its population of 39 million is similarly close to these countries’ combined population of 49 million. Poland also relies on exports in general for around half the share of its gdp that the Czech Republic, Hungary, and Slovakia do, making it much less dependent on Germany. And Poland is also slightly more diversified in its trading partners than the Czech Republic or Hungary are. For example, only 27% of Poland’s trade is with Germany and Austria, whereas Hungary and the Czech Republic conduct 30-35% of their trade with Germany and Austria.

It will, however, be difficult for Poland to exercise leadership in Eastern Europe, not only because of its trade dependence on Germany, but also because of its distraction with Russia to its east. Even though Poland’s economy grew an estimated 2.5 times faster than Germany’s and twice as fast as Russia’s last year, its gdp is still almost seven times smaller than Germany’s and four times smaller than Russia’s. Poland’s population is less than half the size of Germany’s and almost five times smaller than Russia’s. Russia is also Poland’s sixth largest export destination, and supplies Poland with natural gas.

As has often been the case in the past, therefore, the question of Poland’s relationship vis-à-vis the Germans and Russians is of critical importance to the political trajectory of Europe as a whole. How much will Poland’s economy grow in the years ahead? How much leadership will it be able to provide in Eastern Europe? How much support will Poland receive from countries that may want to turn it into a regional counterweight to Germany and Russia – countries, for example, like the United States, Britain, France, or even Sweden? Among other things, the answers to these questions could help determine whether or not Germany can keep hold of its relatively newfound commercial empire.

Interesting articles, nice to see a blog like this today! x