(Disclaimer: this article is more or less a rambling thought-experiment, and should not be taken as a concrete prediction of Canada’s future)

The province of Ontario has long been the most dominant force in Canadian politics. Though it has never been powerful enough to simply impose its will on the rest of the country, neither has the rest of the country been powerful or united enough to sidestep its interests. Ontario’s strength rests on six pillars:

It has the largest economy, with an estimated 37% of Canada’s GDP, compared to just 19.5% for Quebec, 17% for Alberta, 12% for British Colombia, and 4% for Saskatchewan.

It has the largest population, 39% of the Canadian total. By contrast, Alberta, despite having 17% of Canadian GDP, only has 11% of Canada’s population.

It has by far the largest commercial relationship with Quebec, nearly 8 times as large as any other province has.

It has the largest commercial relationship with Alberta, 1.5 times greater than BC’s relationship with Alberta.

It is tied with Alberta for having the largest commercial relationship with British Colombia.

It is the least dependent on inter-provincial trade: it conducts 2.5 times more trade with other countries than it does with other provinces, compared to just 1 – 1.5 times more for Quebec, Alberta, and British Colombia.

A number of these pillars could be undermined in the near future. First, Ontario’s economic size advantage could be cut into by either or both British Columbia and the three Prairie provinces (Alberta, Saskatchewan, and Manitoba). The Prairies will continue to grow if commodity prices continue to rise, since they depend heavily on exporting energy, food, and other natural resources like potash and iron ore. (Of course, the reverse is also true: if commodity prices drop, their economies might shrink relative to Ontario’s). Already the commodity price boom that began in 2002 has boosted the Prairies’ output from 19 to 24% of Canadian GDP, helping to push Ontario’s share down from 42% to 37%.

British Columbia, meanwhile, may outperform Ontario over time for a number of different reasons. For example, BC may benefit more than other provinces from continued economic growth in Asia. BC has the largest proportion of Asian inhabitants of any Canadian province: approximately 25% of BC’s population is of East Asian or South Asian origin, compared to around 17% of Ontario’s, 10% of Alberta’s, and just 3-6% of Quebec’s. An estimated 11% of BC’s population is of Chinese origin in particular, compared to just 5.5% of Ontario’s population, 4.5% of Alberta’s, and 1.3% of Quebec’s.

Much of BC’s Asian population is comprised of bilingual second-generation immigrants who, with a median age of roughly 15 years old, are only just on the cusp of participating in BC’s workforce. BC also has the shortest and cheapest time shipping back and forth between Asia, since, unlike in most other Canadian provinces, doing so does not require two roundabout trips through the far-away, busy Panama Canal. Asia’s economic growth has already helped BC to maintain its share of Canada’s GDP over the past decade, in contrast to Ontario which has seen its share of Canada’s GDP shrink.

Other factors also bode well for BC’s long-term growth prospects. British Colombia has long been the most physically isolated province in Canada, apart from Newfoundland. Not only is BC situated far away from Canada’s largest economies of Ontario and Quebec, but it is also far from those of the eastern half of the United States, where a large majority of Americans live. It is even far from Las Angeles and San Francisco. As such, British Columbia may benefit more than other parts of Canada from globalizing forces like the spread of digital technology and cheaper air travel or shipping, which help to overcome the limitations of physical distance.

To some extent this has already begun to occur. BC has booming film and video game production industries, for example, and regularly attracts tourists from as far away as Australia. BC may continue to benefit from this type of thing in the future, if and as globalization deepens. Given its unique combination of warm weather (by Canadian standards), beaches, mountains, and rare temperate-climate rain forests, the increased accessibility that may be provided by globalization could be a serious boon for the British Columbian economy.

BC has also been limited in the past by the relatively low – and falling of late – cost of natural gas and electricity in North America. BC accounts for more than 25 percent of Canada’s natural gas production (and Canada is the world’s 4th largest gas producer), and it also has a huge amount of shale gas and hydroelectric potential. However, because natural gas and electricity cannot cheaply be exported long distances, or across the Rocky Mountains, or by ship to other continents like oil and coal can, BC has not profited from energy resources to nearly the same extent as its super-rich neighbours in Alberta and Saskatchewan have.

BC had recently hoped to get in the LNG (liquified natural gas) exporting game, and is still likely to do so; however, the shale revolution that has provided US states like Texas with huge gains in natural gas production will probably make such exports far less profitable than they otherwise would have been. The US not only has a glut of natural gas right now, but also has a huge lead on the extremely expensive infrastructure required to liquify and export natural gas overseas, since it is much cheaper to convert LNG import terminals (which Texas and other US states already have a lot of, but which no Canadian province apart from New Brunswick has) into export terminals than it is to build LNG export terminals from scratch.

Over the longer term, however, BC may benefit from new labour-saving technologies that move global manufacturing back from countries that have cheap labour to those which have cheap energy and capital. If, in other words, industrial mechanization technologies reach the next level of sophistication, manufacturing could flood back into North America, causing the price of North American electricity and natural gas to rise. This would be very helpful to the BC economy, not only because BC has an abundance of energy, but also because its lack of non-mountainous land has limited the size of its population, which has caused its labour costs to be relatively high. BC hydroelectric and natural gas production (and wind power, which BC has an enormous potential for as well) could also benefit from any regional, continental, or global effort to safeguard the environment by reducing dirtier oil and coal consumption.

While the economies of BC and/or the Prairies grow faster than Ontario’s, Alberta and BC are also likely to begin trading much more with one another than they currently do. Today, most of the goods produced in Alberta are either consumed in Alberta or exported to Ontario or the United States. The emergence of Asia’s economies, however, may lead Alberta to send a greater share of its energy and food exports westward to the Pacific, via BC. Already Asia accounts for around 40% of the world’s imports of oil, 70% of the world’s imports of liquefied natural gas, and more than half of the world’s imports of food, even as its per capita gdp is still only around $6000. If Asia continues to grow, so too will Alberta’s reliance on British Columbian roads, railways, and ports.

The shale oil industry that emerged in the United States during the past few years might also lead Alberta to send more of its exports westward to BC. Producing shale oil releases enormous amounts of natural gas from the earth as a by-product, such that American natural gas production has risen by more than 25% since 2008. Unlike oil, natural gas cannot be shipped cheaply overseas; only 7% of the world’s natural gas is transported via ship, compared to more than 50% percent of the world’s oil. As a result, Americans have begun looking to export gas to Mexico and Canada by way of overland pipelines.

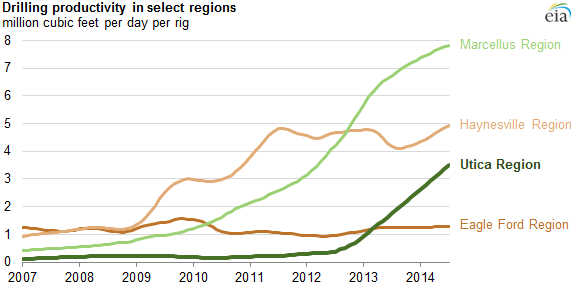

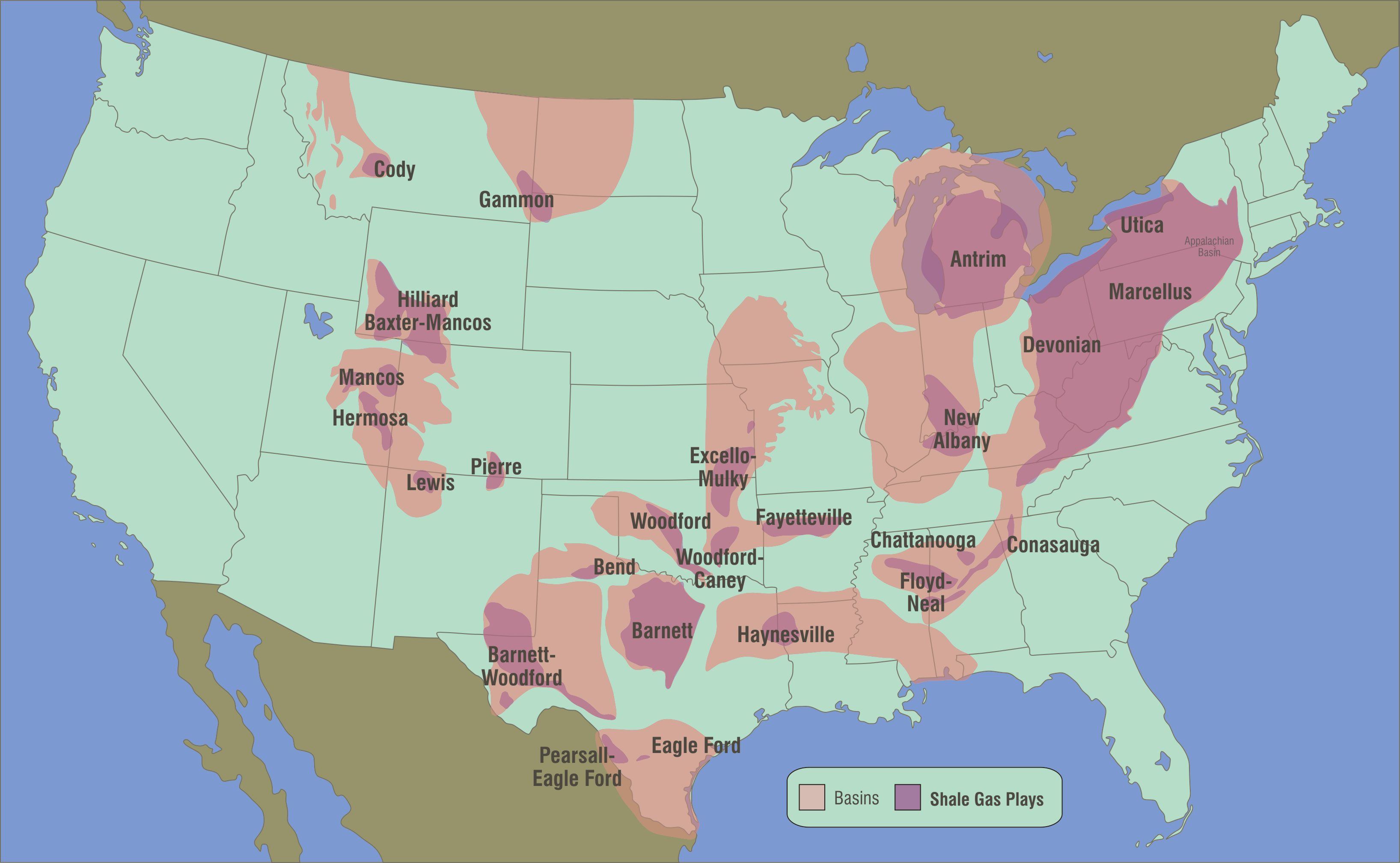

Mexico’s imports of natural gas from Texas, which already doubled between 2010 and 2013, are expected to double again during the next few years. Ontario (and perhaps Quebec), similarly, can expect to see big increases in imports from US states within the Marcellus shale basin, such as Pennsylvania and West Virginia. The Marcellus basin has seen by far the largest and most rapid increase in gas production in the United States of late; Pennsylvania alone has become the third largest American shale gas producer by raising its output by more than 300% since 2011.

The Utica basin, meanwhile, which is located in states like Ohio and Michigan, has seen enormous increases in gas production during the past year as well. This may continue, particularly if New York state ends its ban on natural gas fracking. And, crucially, pipeline infrastructure between Ontario and this part of the US is already in place, since in previous decades Ontario used to export Albertan gas to American states on its borders. There are ten gas pipelines linking Ontario to the US; by comparison, British Columbia and Quebec together only have five gas pipelines that connect to the US.

Just as Alberta finds its gas markets in Ontario and Quebec squeezed by closer-by production in eastern American states like Pennsylvania, it will also face a greater level of competition in US markets as a result of shale production in nearby states like North Dakota. Almost all of the Prairies’ exports of energy and food to American markets travel by way of pipelines or trains that pass through North Dakota. North Dakota has already increased its production of energy by more than 500% since 2007, so these trains and pipelines are now much more expensive to use. Indeed, due to a shortage of oil pipelines, the share of North Dakotan oil that is transported via train has risen from roughly 20% to 75% in the past six years, nearly overwhelming the state’s rail network.

Finally, the shale boom in the Gulf states of Texas and Louisiana, the first and third largest energy producers in the United States, combined with economic development in Mexico and the Caribbean, is making the use of Gulf of Mexico’s ports and refineries much more competitive than they have been in the past. This matters to Alberta, since much of Alberta’s oil was supposed to have been refined in the Gulf region. Now, however, many of the Gulf’s refineries might begin to be retrofitted to refine the ultra-light oil released from shale instead of heavier types that Alberta and Venezuela produce.

Alberta and the other Prairie provinces are also affected by this because their exports of food, coal, and some other resources are usually shipped to global markets via ports in the Gulf of Mexico (after being trained through North Dakota and then barged down the Mississippi River), such as the ports of New Orleans and Houston, both of which handle more cargo in terms of sheer tonnage than any other port in the United States. As a result, Alberta and Saskatchewan may soon have to rely more heavily on BC, where there will be far less competition from American shale energy, and where more export facilities will be built to transport fossil fuels, food, and other commodities to Asian markets.

Quebec too is likely to degrade its economic relationship with Ontario. Quebec has the most rapidly aging population of any major Canadian province, and so may soon face challenges in producing or consuming enough to keep its economy growing at a pace it is satisfied with. This challenge is compounded by Quebec’s feeling of cultural insecurity and lack of control over its borders, since not only is Quebec relatively wary of immigrants, but any immigrants it does bring in can always choose to go live in other parts of Canada that are wealthier, warmer, and more welcoming.

One of Quebec’s solutions to this problem will be to attract French-speaking immigrants from nearby Haiti and from northern and western Africa. In turn, these immigrants will create economic relationships between Quebec and their native countries. Indeed, with a large wave of second-generation immigrants in Quebec coming of age during the next decade, this process may soon begin to accelerate with or without further immigration. Already Quebec`s most common foreign languages are Arabic, Spanish, Italian, and Portuguese, in contrast to most of the rest of Canada where they are Punjabi, Cantonese, Mandarin, and Tagalog.

Quebec will also use the introduction of the internet in the developing world to interact much more with these countries, in areas like media, banking, and software development. The internet might also allow Quebec to engage increasingly with France, which is still the world’s fifth largest economy and has the youngest population of any large country in Europe. To get an idea of just how significant Quebec’s linguistic affinities might soon become, consider that even today Quebec`s largest foreign trade partner apart from the US and China is Algeria, an Arabic country in North Africa that is only so-so at speaking French. Unlike other Canadian provinces, Quebec has chosen to import much of its oil from Algeria. This is particularly noteworthy given that oil is not even an industry in which speaking the same language would seem all that important. If Quebec can let such ties influence its oil purchases, imagine what its future might be in industries where language actually matters.

Quebec could perhaps also find that globalization will give it greater affinities with Romance economies like Latin America, Italy, Spain, Romania, and Angola. It is, after all, far easier for a speaker of Spanish or Italian to learn to get by in French than it is for an English speaker to do so. Plus, Latin America speaks English less than almost every other part of the world, so there may be less competition there for French speakers than would otherwise be the case. As a result, Quebec’s commercial patterns are even more likely to diverge from those of Ontario. This is because Ontario’s focus in a globalizing world will probably be oriented more towards the places its immigrants are from, such as China, South Asia, and the Philippines, as well as towards English-speaking economies like the United States, Britain, Australia, Jamaica, Nigeria, South Africa, and Singapore.

Romance languages global map

Finally, the Atlantic Maritime provinces of Nova Scotia, New Brunswick, Newfoundland and Labrador, and Prince Edward Island could become better integrated with one another than they are today, and better integrated with the economies of western Canada, Quebec, Europe, and the Northeastern United States than they are today.

Today the Maritimes are, to a certain extent, divided from one another by the ocean. Both Newfoundland and Prince Edward Island are islands (though PEI was connected to the rest of Canada by a 13-km long bridge in 1997), while Nova Scotia, the most populous Maritime province, is a peninsula with a large island, Cape Breton, on its northern edge. To drive, for example, from Halifax (the largest city in the Maritimes) or Yarmouth (on the southern tip of Nova Scotia) to Fredericton or Saint John in New Brunswick can be about 350 – 600 km, even though flying is only around 150 – 250 km. To drive from Halifax to Charlottetown on Prince Edward Island is 285 km, but only a 175 km flight. And St Johns on the island of Newfoundland is about a 900 km flight from Halifax or Fredericton. As a result, if short-distance airplane costs become cheaper, it could help the Maritime provinces to become better integrated with one another.

A similar thing is true of the Maritimes’ relationship with Quebec and with the Northeastern United States. Currently it is 550 km drive from Saint John, New Brunswick (a province where about a third of people speak French) to Quebec City and a 790 km drive from Saint John to Montreal. If, however, the American state of Maine builds an east-west highway, those numbers could drop to around 400 – 550 km. (This would also shorten the drive between the Maritimes to Toronto, Ontario, but that would still remain over 1000 km long). Meanwhile, cities like Halifax and Yarmouth are about 1000 – 1400 km away from from Boston and New York City by road, but only 450 – 950 km from them via airplane.

Commercial ties between Quebec and the Maritimes could also deepen as a result of the development of areas in northern Quebec and Newfoundland’s mainland territory of Labrador, which share a land border with one another that is over 2000 km long (see map above). These areas have been too remote to populate in the past, but over time it is possible that they will become less remote, or that the development of their natural resource sectors – which have a great deal of potential – will be realized with fewer humans and more machines.

In recent years, the Maritimes have been becoming much better integrated with the Canadian Prairies, as large numbers of young people from the Maritimes have moved to oil-rich cities like Edmonton and Fort McMurray to find employment. This trend may continue in the future (though, if oil prices fall, it may also be reversed), and, if globalization deepens, so too might the general trend of the Maritimes being able to interact with faraway western Canadian provinces that in the past they have had relatively little to do with. It is, by the way, almost 5000 km from Halifax to Vancouver via land, and more than 11,000 km to ship goods between Halifax and Vancouver by way of the Panama Canal.

Finally, the economy of the Maritimes could become better integrated with Europe. The Maritimes tend to have closer ties of identity to Europe than other Canadian provinces do, and they also have a decent-sized French-speaking population that might increasingly interact with France as a result of globalization. The Maritimes are, in fact, located closer to Europe than they are to the Canadian Prairies.

Perhaps most importantly, it is possible that the Maritimes will begin exporting significant quantities of natural resources – particularly oil from Newfoundland, but potentially also liquified natural gas from New Brunswick, as well as other commodities – to European economies. Newfoundland today accounts for around 17 percent of Canadian oil production, most of which is exported to the US or other Canadian provinces. However, as the US and other Canadian provinces have increased their oil supply in recent years as a result of shale energy and the Albertan oil sands, Newfoundland has been looking further abroad for customers. Europe would seem like a natural fit; not only is it relatively nearby, but it is also increasingly in search of energy imports, given that its traditional energy suppliers in Russia and the Middle East have been consuming a growing share of their oil and gas instead of exporting it, and exporting a growing share of their oil and gas to India and Asia instead of to Europe.

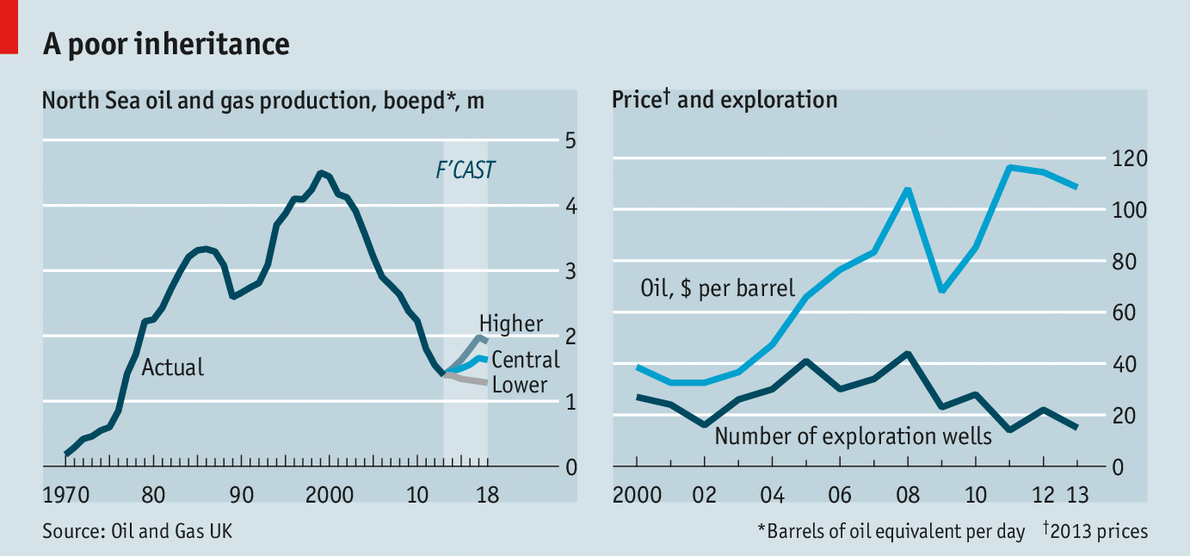

The relationship between Newfoundland and Britain could become particularly interesting. In the past, Britain has not been an oil importing economy, but instead produced its own oil from the North Sea. In the past few years, however, British oil production in the North Sea has been dropping very quickly, forcing the British to become net oil importers for the first time in a long time. Britain still only imports a relatively small amount of oil, but if North Sea energy production continues to fall (as many believe it will, not only in British waters, but also in Norwegian, Dutch, and Danish ones) Britain could quickly become one of the world’s largest oil importers. Especially given the historical ties between Britain and Newfoundland – as recently as 1948, 14 percent of Newfoundlanders voted to essentially continue being part of Britain, and 45 percent voted to be independent rather than join Canada – this could potentially help create close economic ties between the two.

To sum up, Ontario`s economy could be likely to shrink compared to BC and/or the Prairies and become relatively less integrated with Quebec and Alberta, at the same time as the economies of Alberta and BC become much better integrated with one another and the Atlantic Maritime economies become better integrated with Europe, with Quebec, with one another, and possibly with western Canada. As a result, it is not impossible to imagine that Ontario’s dominant position in Canadian politics could largely disappear, possibly even within a fairly short period of time.

If this were to occur, Canadian unity might be forced to rely much more heavily on sentiments of national identity than it does today. This could be problematic, as provincial economic interests (and environmental interests) may in many cases run counter to one another. It might force parts of the country to have to decide between economic development and national cohesion.

With potentially divergent economic interests, and with each individual major province already conducting an average of around 1.7 times more of its trade outside of Canada than with other provinces, and with the continued existence of Quebecois nationalism, Canadian political unity could become strained, perhaps to the point of provinces or regions becoming effectively or even formally independent. I am certainly not predicting that this will happen – I am a Canadian, so I know firsthand that Canada’s sense of national identity is relatively strong – but I would also not rule it out entirely, given the factors discussed above.

On the bright side, if the Canadian state really was ever to dissolve, it could make for some really interesting hockey tournaments at future Winter Olympics.

3 Comments