With the downward revision of Japan’s GDP growth figures last month, the Japanese economy is technically back in recession, projected to shrink by a slight amount during the year as a whole. Even though most analysts had previously forecast Japan’s economy to expand at a rate of 2 percent in 2014, nobody was too surprised by the news that is contracting instead. The recession is the country’s fifth since 1997, and its third since the global credit crisis of 2008. While some might see a silver lining in this – namely, that Japan’s economic growth going forward could not possibly get any slower than it has already been – many economists do in fact view the country’s problems as likely to grow more rather than less acute during the years ahead.

Unlike in recent decades, Japan must now grapple with an empowered China, with slowing economic growth among key trading partners like South Korea, Taiwan, coastal Chinese provinces, and Europe, with net government debt that has risen from 80 to 145 percent of GDP over the past decade, and with a Baby Boom generation that has reached between 65 and 70 years old on average (about a decade older than those of Europe or America). These trends arguably provide the backdrop to Japan’s current slowdown, even as the catalyst for the recession has been viewed as a rise in the country’s consumption tax, from five percent to eight percent, which came into effect earlier in the year.

What might be more surprising than the recession itself is that investors in Japan’s stock market seem basically unperturbed by the news of it. The Nikkei 225 index is actually higher now than it was before the recession become public knowledge; it continues to trade at around a seven-year high, virtually double the price it averaged between 2008 and 2013. Admittedly, this is a far cry from the Nikkei’s all-time highs in 1992, when it was worth well over double what it is today. In fact it does not even match the highs of 2000, 1997, 1994, and several other years going back all the way, astoundingly, to 1986. That’s right: Japanese stocks were worth more 29 years ago than they are today. Still, a seven-year high amidst the onset of an economic recession is something that is difficult to ignore.

Of course, the rise in the Nikkei may simply reflect the fact that investors have become so accustomed to seeing Japan’s economy shrink that they built in the risk of a recession to the price of Japanese stocks ahead of time, which meant that those prices did not require much revising when the recession actually arrived. The Nikkei’s rise may also reflect the fact that investors have faith in prime minister Shinzo Abe, who has loudly promised to stimulate the Japanese economy and revive Japanese prestige, and who is already using the recession as an excuse to call a snap election intended to extend his party’s leadership by an additional two years, from 2016 (when parliamentary elections would have otherwise been held) to 2018. [update: the elections have now happened. Abe’s party won a two-thirds majority, though with the lowest voter turnout since WW2].

Or it may be that investors have so little faith in Europe, China, and commodity-exporting economies like Brazil or Australia, and see US equities as being too expensive now that the S&P 500 has again reached all-time highs in recent days, that they have been forced into Japan’s stock market almost by default. Finally, and most intriguingly, the Nikkei’s performance may reflect the possibility that the potential of Japan to achieve a renewed, meaningful pace of economic growth is actually more promising than most Japanese themselves recognize.

With Japan’s stock market and GDP indicators pointing, almost paradoxically, in far-opposing directions, Japan’s economy now resembles Schrodinger’s infamous Cat: its true health is in a state of uncertainty, the resolution of which seems to depend on the specific approach at which it is observed. Of course, unlike the Cat itself, Japan’s economy is a paradox that we know can probably be resolved. All we need to do is take a look underneath the lid, so to speak, at the underlying fundamentals of the country’s medium-term (say, within the next decade or two) economic prospects. What are those underlying fundamentals? It turns out that the originator of the Cat query, Albert Einstein, might be of some use here as well:

General Economic Relativity

One of the most fundamental theories of conventional economic forecasting is the idea that, in general, countries that are relatively poor will grow at a faster pace than those that are relatively rich. This is, of course, why a country like India disappointed investors when it grew at 6.5% in 2011 and 5% in 2013, whereas even 2% growth in the European Union or 3% growth in the United States would be a widely celebrated event.

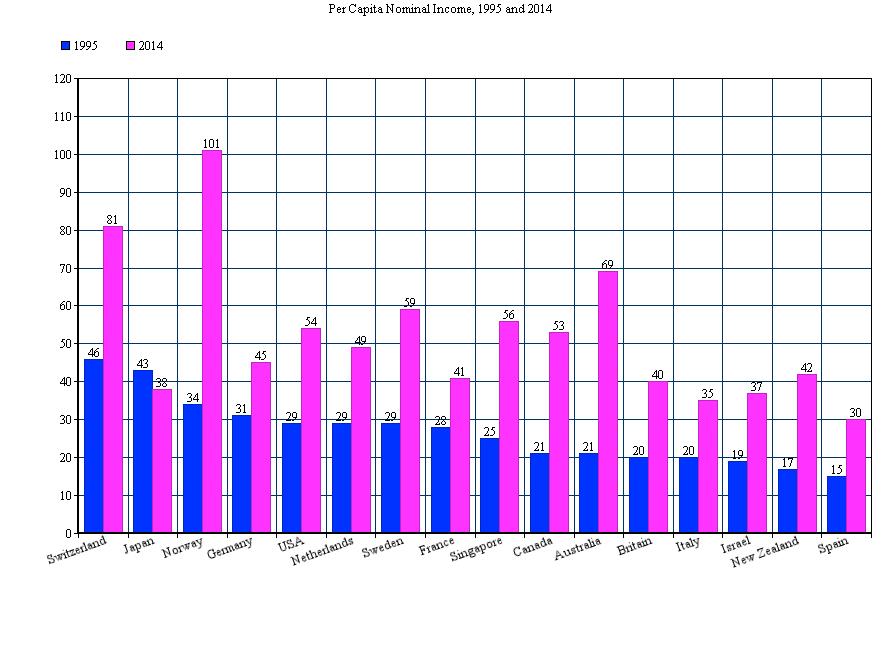

In the case of Japan, the extremely high income levels the country had two decades ago might have limited its economy’s ability to grow. According to the IMF, in 1995 Japan’s per capita income was 1.5 times higher than that of the next wealthiest large developed economy (the United States), 2 times higher than that of the next wealthiest large economy in the western Pacific (Australia), and 3.3 times higher than that of the next wealthiest economy in Northeast Asia (Taiwan). As a result of being so wealthly at the time, Japan’s room to expand its economy further may have been somewhat constrained.

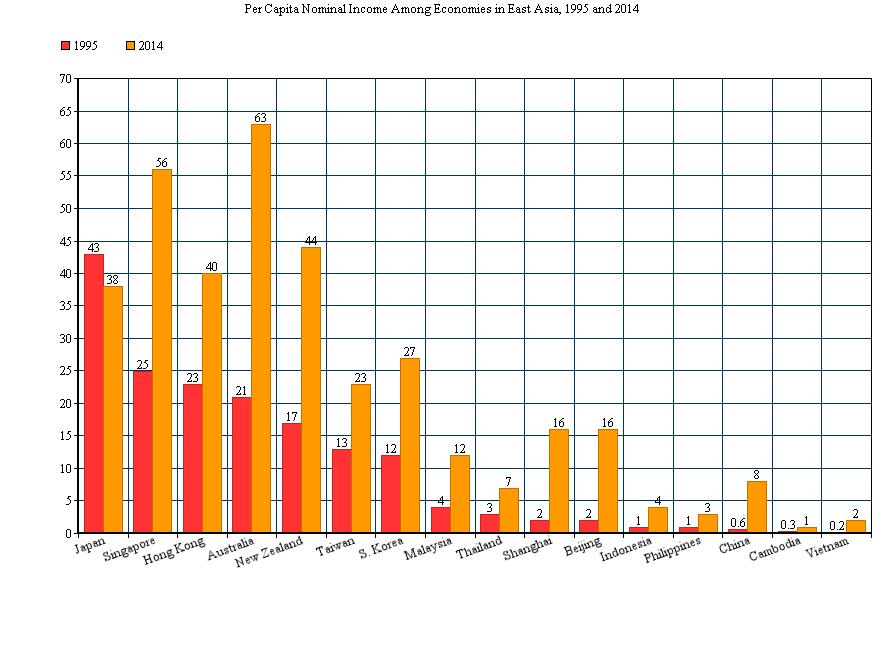

Today could scarcely be any more different. If the idea that relatively poor countries are in general likely to grow relatively quickly (i.e., the theory of general economic relativity) is to be believed, Japan is now in a much more favourable position where its growth potential is concerned. The country has become much poorer than other developed economies in terms of its per capita income, especially in comparison to regional counterparts like Australia, New Zealand, and Singapore, which have grown rapidly since the mid-1990’s. Japan’s lead over developing East Asian economies is also not nearly as large as it used to be (see charts below), as a result of the emergence of China and the strong rebound of other East Asian economies following their financial crises in 1997 and 2008. Arguably, this comparatively low level of nominal wealth bodes well for the Japanese economy going forward, relative to how it has performed during the past two decades.

Special Economic Relativity

Another fundamental principle of economics is that of “comparative advantage”, the idea that economies will tend to construct themselves in ways that reflect their greatest advantages (or smallest disadvantages) in relation to other economies. This begs the question: what makes Japan special, relative to other countries? More to the point: is what makes Japan special likely to help its economy grow at a decent pace during the years ahead?

One of the main qualities that makes Japan special is its “economic mass”. This does not only refer to its economic size — Japan’s economy is the third largest in the world, 1.7 times larger than fourth-place Germany and just 1.6 times smaller than second-place China, according to the World Bank — but, just as important, refers also to Japan’s internal unity and compactness. Unlike in other major economies like the US or China, Japan’s population is not spread out over a vast territory, but is instead crammed into an area that is only about the size of Montana. Japan’s economic activity is even more highly concentrated: the Greater Tokyo Area alone accounts for an estimated 40 percent of Japanese GDP, and the island of Honshu (in which Tokyo is located) for upwards of 80 percent of Japanese GDP.

Japan is also socially cohesive. Its income inequality is relatively low (unlike the US, China, or Brazil, where income inequality is extremely high), and its unemployment rate is the lowest of any developed nation apart from Switzerland. Japan also possesses no major ethnic, linguistic, or religious divisions. An estimated 98 percent of Japan’s population is ethn0-linguistically Japanese, and, religiously, less than 2 percent is Christian. By comparison, Japan’s neighbour China is home to an estimated 23 million Muslims (mainly living in the country’s northwest), more than 100 million non-Muslim ethnic minorities (mainly in the southwest), 250-300 million native speakers of a variety of non-Mandarin Chinese languages (mainly in the southeast), and perhaps as many as 100 million evangelical Protestants.

Even Japan’s developed-economy competitors cannot compare to it in terms of internal unity. In the German economies, there has been a slowly (re)emerging commercial divide between eastern Germany, Austria, and Bavaria on the one hand and western Germany on the other, reflecting the fact that Eastern Europe has been growing quickly while Western Europe has been lodged in a seven-year economic funk. Within both France and Italy, meanwhile, northern regions have been growing while southern regions have been virtually in depression. And in Britain and Spain, secessionist movements like those of the Scots and Catalans have been growing in prominence of late.

Even in the United States there has been a growing divide between the Northeast and the South/West, a result of the fact that Texas alone has accounted for more than one-fifth of US economic growth since 2007, and that globalization and demographic shifts have had the effect of integrating states like Texas, California, and Florida more closely with Latin America than ever before, and states like California, Oregon, and Washington more closely to the rest of the Pacific world than ever before. (In Canada a similar trend has been occurring). All of these developed countries remain internally cohesive, of course; just not as potentially cohesive as Japan. Indeed, many of the above trends may be likely to continue in in the years ahead, which could make Japan’s internal unity even more distinctive.

Japan’s unique combination of economic size and internal unity may become increasingly significant during the years ahead, as it may allow the Japanese to throw their weight around in a world economy that, cliches of globalization notwithstanding, is in many ways still becoming rapidly smaller and smaller. The continuation of the Internet Revolution will probably be the most significant near-term driver of such globalization, but further leaps in conventional transport — by air, sea, or land — cannot be ruled out either. If rapid globalization does continue, and if large, internally cohesive economies like Japan are among its beneficiaries, economics may increasingly resemble Einstein’s actual theory of special relativity, with an economy’s mass beginning to directly correlate with its economic momentum.

Commercial Entanglement

Another characteristic that makes Japan special is its relative level of isolation from the rest of the global economy. According to the World Bank, the value of Japan’s international trade of goods and services is equal to just 30 percent of its GDP, a lower share than any other large developed economy apart from the US, and much lower than Japan’s most notable neighbours, China (50%), South Korea (103%), and Australia (41%). Indeed, many East Asian economies, such as Thailand, Vietnam, Malaysia, and Singapore, are among the most trade-dependent economies in the entire world. Japan, by comparison, is not only not dependent on trade in general, but is also not dependent on either imports or exports in particular.

What this means is that Japan might be able to manage a regional or global economic slowdown more easily than most other economies can. During the past few decades this ability has not mattered much, since global growth, and particularly East Asian growth, has been so formidable. Going forward, however, Japan may find itself able to manage persistently slower growth in places like China and Europe more easily than most other countries around the world will be able to.

A slowdown in China, for instance, would hurt Japanese neighbours like South Korea, Taiwan, and Australia, countries in which 30-40 percent of exports go to China and exports in general are equal to 20-60 percent of GDP, far more than it would hurt Japan, which sends just 23 percent of its exports to China (including Hong Kong) and where exports in general are equal to just 15 percent of GDP. This ability to withstand external sluggishness could be a major advantage for Japan. It has certainly been helpful for the US, where a low dependence on exports is currently shielding the American economy from simultaneous recessions in most of Europe and Japan.

Crucially, even as Japan’s trade patterns might shield its economy from the full brunt of external crises, Japan also has the potential to benefit from becoming a more vigorous trading nation in the future. In the past, Japan’s ability to access global markets has been limited by its lack of proximity to the Atlantic world, where most of the globe’s economic and consumer activity is located. As a result, Japan is likely to benefit from the expansion of the Panama Canal, which is finally set to be completed in 2016, with significant consequences for inter-oceanic shipping. (In fact, arguably the most important consequence of the canal expansion is that it will allow 80% of LNG tankers to use it — currently none do — which will benefit Japan specifically, since Japan accounts for nearly 40% of the world’s LNG imports, and since, on the opposite side of the canal, Texas, Lousisiana, and Latin America may account for much of the world’s LNG export growth in the years ahead). Similarly, Japan could benefit from the continued growth of the East Asian and Indian consumer markets, as well as from more efficient cargo shipping worldwide, by air or by sea.

Finally, Japan might benefit from being able to use the Trans-Siberian railway to directly access European markets. This may finally occur because: a) the Russians increasingly need Japan as an ally because of their growing concerns with both China and the West; b) Russia’s rail network is becoming less crowded as a result of falling commodity prices and falling European demand for coal (since coal accounts for one-third of Russian rail freight, and commodities in general account for two-thirds of Russian rail freight); and c) because technology may make it cheaper and faster to maintain and operate railways and to load and unload cargo containers, which on the Japan-Russia-Europe route you expensively have to do twice: once at the seaports on Russia’s Pacific coast, and a second time in Eastern Europe because Russia’s and Europe’s rail networks use different gauges.

In addition to its foreign trade, Japan’s global investment position looks to be relatively strong. Japan has the highest NIIP in the world (NIIP = Net International Investment Position; basically, this is the amount of money a country’s government, businesses, and people are owed after you take into account the amount of money they owe to other countries). Though trustworthy, up-to-date NIIP statistics are notoriously difficult to come by (which is why people often focus instead on public and private debt-to-GDP ratios, which can be misleading because they only take into account a country’s foreign liabilities, while ignoring its foreign assets), as recently as 2010 Japan’s NIIP was estimated to be the same as those of China and Germany – which are the world’s next two largest creditor economies – combined. Indeed, while in America the media tends to obsess over Chinese ownership of US government debt, Japan owns just 3 percent of US debt less than mainland China does, and only 13 percent less than mainland China plus Hong Kong. Japan may have lots of assets with which it can potentially revive itself, in other words.

Energy Matters

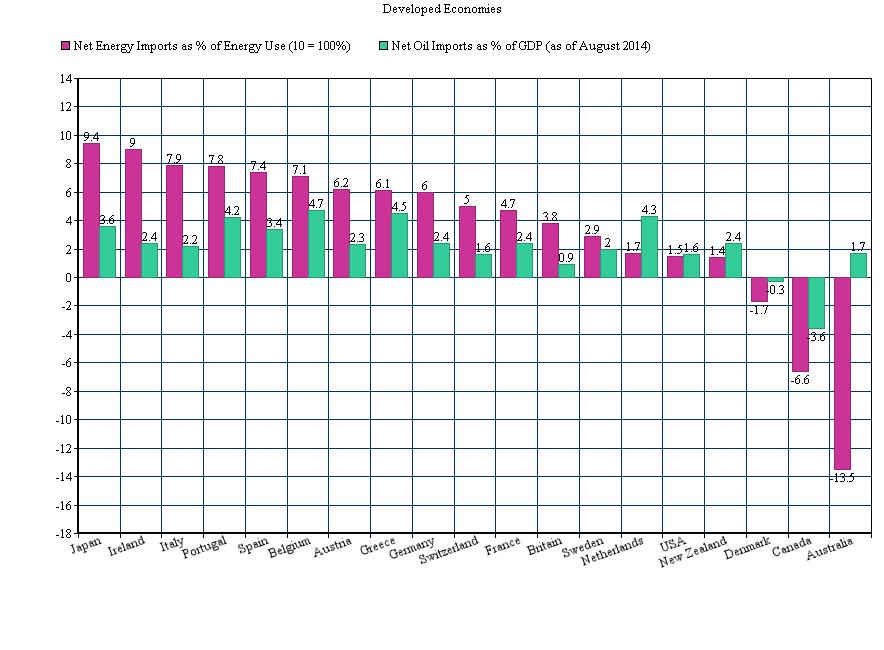

Does the inertia of a body depend upon its energy content? In economics, the answer to this famous question of Einstein’s appears to be yes. Developed countries in which energy imports account for a high share of GDP, such as Japan, Spain, Italy, Greece, and Portugal, have suffered some of the worst growth rates in recent years, when oil and gas prices have been very high. Developed economies that are major energy exporters, on the other hand, like Canada, Australia, and Norway, or that are relatively energy neutral, like the US, Sweden, or Denmark, have generally performed much better.

With oil prices having reached a five-year low, falling by well over 50 percent since just the beginning of October, countries like Japan may now be better positioned for success than they have generally been in the recent years. In fact, it is not only lower energy prices that will have a positive impact on the Japanese economy, but lower prices for other commodities as well, which to varying extents are often correlated with energy prices. Japan, to be sure, is the world’s largest importer of tin, the second largest importer of iron ore, aluminum, copper, nickel, and silver, the largest food importer among developed economies, and by far the largest spender on coffee imports apart from the US.

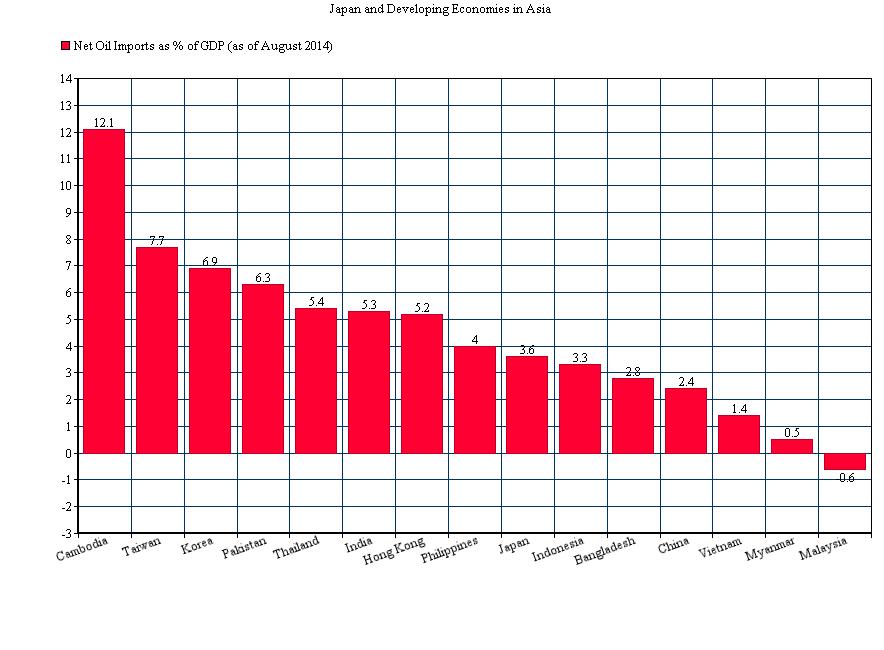

Of course, a developed, energy-efficient economy like Japan is not going to benefit nearly as much from falling energy prices as an energy-intensive, import-dependent emerging market like India, Pakistan, Thailand, the Philippines, or, on the wealthier side of the emerging market spectrum, South Korea or Taiwan (see graph). Even China, which only imports an estimated 13 percent of its energy (compared to 94 percent for Japan), will probably benefit much more from falling energy prices than Japan will, since the Chinese use about 5 times as much energy per dollar of GDP than the Japanese, are enormously dependent on importing commodities in general, and may be able to reduce some of their domestic pollution by replacing coal production with oil and gas imports.

But in this way too Japan stands to gain, relative to most other developed economies. This is because most of the main buyers of Japanese exports are energy-intensive emerging Asian economies, many of which are among the greatest beneficiaries of falling energy prices. Indeed, more than 40 percent of Japanese exports go just to China, South Korea, Thailand, or Taiwan, whereas no energy-exporting country receives more than 2.5 percent of Japan’s exports. In contrast, the US sends 25 percent of its exports to Mexico or Canada, both of which are substantial oil exporters. The Europeans, meanwhile, trade mainly among themselves, and include enormous energy exporters like Norway and Russia.

Japan is also in a unique position where alternative energy sources are concerned. It has far and away the most nuclear energy potential in the world, since it has the world’s third highest nuclear energy-generating capacity (virtually double that of fourth-place Russia), but has not been running any of its nuclear plants since the Fukushima incident in 2011 soured public support for them. Japan could, and might, turn many of them back on in a fairly short period of time.

Japan also has the fourth highest hydroelectric energy generation among developed countries (double that of fifth-place Spain), the third highest biomass/waste energy generation among developed countries (more than 50% higher than fourth-place Britain), the third highest geothermal energy production among developed countries, and the third highest solar energy generation of any country in the world (50% higher than fourth-place US). In addition, because of the growing possibility of using industrial machines to run manufacturing plants overnight, Japan may no longer be forced to waste much of the energy produced by hydroelectric, nuclear, geothermal, and wind, which unlike oil or gas cannot be shut off at night.

Finally, Japan may be able to get more commodities from Pacific Russia. First, as mentioned above, Russia is increasingly in need of allies outside of China or the West, and Japan is the obvious choice in this regard (South Korea is also an obvious choice, but South Korea is very closely embedded into the economies of both China and the West, and it is also much smaller than Japan). Second, as technology may continue to make resource-extraction much less dependent on labour, the commodity-producing potential of the Russian Far East could perhaps finally be realized in spite of the region’s tiny population of just around five million (less than one million of whom live in the gigantic territory to the north and east of Lake Baykal). Sakhalin island and the Kamchatka peninsula, both of which are relatively inhabited, rich in natural resources, and particularly accessible to Japanese influence, could be two interesting places to watch in this regard.

Demographic Entropy

Analysts who are bearish on Japan ultimately tend to focus on one factor above all others: Japan’s aging population. This is certainly not an unreasonable concern; Japan’s population is the oldest in the entire world, with a large Baby Boom generation that is on the cusp of old age, a large Echo Boom population that is on the cusp of middle age, and a population of seniors (above 65 years old) that accounts for 26 percent of Japan’s total population, compared to only 14 percent in the US, 17-18 percent in Britain, France, and Spain, and 20 percent in Germany. This is, really, the main reason the Nikkei 225 index has been trading at prices that are just 13.9 times its earnings and just 1.3 times its “book value”, compared to a 19 price-to-earnings ratio and 2.8 price-to-book ratio for the S&P 500 in the US, or 15-19 price-to-earnings ratios and 1.8-2.1 price-to-book ratios in France, Britain, and Germany, where populations are more youthful.

While it would be unwise to ignore Japanese demographics, or try to spin them somehow as being an economic advantage rather than a disadvantage, it may nevertheless be useful to play devil’s advocate here for a bit, and explore the possible reasons why Japan’s aging population may not end up being even close to as bad for its economy as it is generally expected to be.

Reason 1: Japan’s retiring population means that it alone among countries in the developed world may not be negatively affect by the one-two punch of outsourcing and automation, which could rapidly lead to unemployment and income inequality crises in other countries. This could further increase Japan’s internal unity compared to other nations, giving it even more of an edge in terms of its economic “mass”.

Reason 2: Japan’s economy is not a closed system: it can decrease its demographic entropy by way of immigration. While it has become common for journalists to point out the fact that Japanese culture is not accustomed to dealing with immigration, the truth is that Japan has historically been able to adapt its mode of behaviour in very short periods of time, so it would not really be such a surprise if the Japanese were to begin bringing in lots of immigrants in the future, breaking with tradition. Certainly Japan’s high standard of living and proximity to Asia means that it can probably attract immigrants if it wants to. Japan has not needed immigrants in the past, but if and when it does, it may turn out that it doesn’t have such an affliction to them after all.

In fact, one way of looking at the fact that foreign-born individuals only account for an estimated 1.9 percent of Japan’s population (compared to 12 percent for Germany, France, and Britain, 14 percent for the US, 21 percent for Canada, and 28 percent for Australia) is that Japan still has a lot of room to increase the share of its total population that immigrants account for. Japan could actually bring in millions of immigrants and still have them account, for example, for less than one-fifth of its population, whereas a country like Germany or even the US would perhaps start feeling uncomfortable with immigration if immigrants were to make up more than a quarter or a half of their total populations.

Reason 3: Another way to look at Japan’s population of seniors is as the first wave in an enormous global demographic shift, with the aging populations of the developed world (particularly Europe and Canada) and the former Soviet Union only about a decade behind the Japanese, and with China not too far behind them. What this means is that many of the age-related issues that Japanese populations have already been dealing with for a while may now be coming to much of the rest of the world. This might actually help the Japanese economy, if it finds some of the goods and services it has been focusing on — among them robotics, health care, pharmaceuticals, and age-related consumer products — in demand from other countries.

In other words, Japan may be able to export some of its expertise and products to aging Western, Russian, Korean, and Chinese populations who are dealing with their own increases in age-related illnesses. In fact, because of the pollution in China, the coming decade may see an enormous increase in certain types of environment-related illnesses in China, even though China’s population is still somewhat younger than most Western populations. Many wealthier Chinese may even go to Japan to receive health care. The aging of China and the West is obviously not the happiest of prospects to contemplate, but it may nevertheless be something the Japanese economy is relatively well-positioned to benefit from.

Reason 4: Even if Japan’s aging population is a long-term problem, it may not be such a burden for its economy during the next decade or so. Japan’s Boomer population is only around 65-70 today, and is still extraordinarily healthy for its age. Because of the Internet, Japanese seniors may also be able to keep their productivity and consumption up more than people of the same age have historically been able to do. Japan’s Echo Boomers, meanwhile, are still just around 40-45 years old. Because Japanese have so few children (13 percent of Japan’s population is below the age of 15, compared to 19 percent for the US, Britain, France, and Australia), they have more time and money to spend on other things, whether work-related or leisure, which can be economically stimulative. Spending time and money on children may be great for an economy over the long term, but in the short term it can arguably hold an economy back.

Alternate Dimensions

Economists have historically tended to view wealth as being derived from a combination of three “inputs”: capital, labour, and land. Japan is very well endowed in the capital and labour departments, but it has been held back to a certain extent by its scarcity of land. Excluding mountainous regions, which constitute an estimated 75 percent of Japanese territory, Japan is only about the size of Michigan. Even including its mountains, Japan’s population density is 1.5 times higher than Germany’s and ten times higher than in the US. Among significant economies, only India, South Korea, and the Netherlands are more densely populated than Japan (and none of them by much).

Japan has paid a steep price for its density: according to the Economist, between 1980 and 2000 Japanese property prices were consistently the highest in the world, both in real terms and in relation to average income levels. Japan’s lower property prices today are simply a reflection of its slow pace of population and economic growth; if the economy of Japan is to rebound, it will need to find a way to make due without much physical space. Indeed, even today, following two decades of deflation, Tokyo is the fifth most expensive city in the developed world and the eighth most expensive city in the entire world to buy an apartment in.

Can technology finally allow Japan to overcome its lack of space? To a certain degree the answer may be yes. Japan’s vast multitude of mountain valleys, for instance, are no longer nearly as isolated as they were even just five years ago. Today, with the modern Internet, their inhabitants can access national markets and social networks, and can increasingly bargain collectively for goods and services. Over the next decade they may become even less isolated, as technology is likely to sharply reduce traffic on the country’s crowded road network (which will also free up plenty of room in Japan’s large cities), gasoline prices may remain lower than they have been in recent years, and elderly and retired Japanese may travel less frequently than Japanese populations have done in the past.

Japan’s mountain regions may also be aided by technologies like the Aeroscraft, an airship the length of a football field that is currently being developed in the US as a response to the difficulties its military has faced in mountainous landlocked Afghanistan. The Aeroscraft could allow non-bulk goods to be shipped efficiently in mountain valleys where there is not enough cheap land available for significant airports, and where the need to take-off and land in each individual valley makes ordinary airplanes (which have extremely high take-off costs) highly inefficient. While it is impossible to know for sure, it seems possible that Aersocraft airships will be ready for regular use within five to ten years. In addition to helping Japan’s mountainous territories better participate in the Japanese economy, they could potentially also help Japan access markets in nearby economies like South Korea and northern China more quickly than can be done by ship.

Another way to overcome a lack of conventional space is to construct high-rise apartment buildings. Japanese cities have already done this, of course, yet they have been somewhat limited in their efforts to do so by the high cost of construction. Going forward, however, such costs may decline. As Japanese workers retire en masse, for example, and as many white-collar jobs in Japan begin to be automated or outsourced while more work can be done from home offices because of the Internet, Japan is likely to see a large number of its commercial high-rises transformed into residential buildings. While this transformation is not inexpensive, it can be done at a tiny fraction of the price of building a high-rise from scratch.

In addition, if commodity prices remain low, and if China’s enormous construction frenzy finally ends, Japan will find it much cheaper to import building materials. It might even be able to import some skilled Chinese engineers, or Chinese-built apartment modules. Indeed, modular construction might might significantly reduce both the costs and the required labour and time of high-rise construction. This could be a huge help for a country as incredibly compact and mountainous as Japan.

In Search of a Unified Theory

How will Japan’s real estate, demographic, commodity, commercial, sociopolitical, and income factors combine in the years ahead? It is not clear. What is clear, though, is that ignoring Japanese stocks remains something that cannot be done lightly. Japan’s economy continues to have Potential. With the Nikkei still relatively cheap on a price-to-earnings and price-to-book basis, then, it is not surprising that the recession has not led to a market drop. The cat may yet be alive.

2 Comments