Canada, the world’s sixth largest “developed” economy, has been on an excellent run in the recent past. According to figures from the World Bank, Canada’s GDP grew at a faster pace than those of the United States or Britain during five out of six years between 2008 and 2013, and during 10 out of 15 years since 2000. It grew at a faster pace than those of Japan, Germany, and France during more than 20 out of 25 years since 1990.

In 2014, however, Canadian growth appears to have trailed that of the US and Britain, the first time since 2003 that it has lagged behind both at the same time. Now, with oil prices having fallen by more than 50 percent since just the start of October, many Canadians are worried their economy will disappoint even more during the months ahead. These fears may be justified: the Canadian economy could have to face a number of significant challenges in 2015.

Challenge #1: Oil Prices

Lower oil prices, assuming they persist, represent a fourfold threat to the Canadian economy:

1. Oil exports account for a larger share of GDP in Canada than they do in any other nation in the rich world, with the exception of Norway or the Gulf Arab monarchies. In fact, apart from Canada, Norway, or Denmark, every noteworthy developed economy in the world is actually a net importer of oil. Canada, in contrast, is the world’s 10th largest net exporter of oil, and the world’s 5th largest net exporter of oil outside of the Middle East.

As of August 2014, the value Canada’s oil exports were the equivalent of approximately 3.6 percent of Canadian GDP, which means that the 50 percent reduction in the price of North American crude oil that has occurred since August should lead, all other things being theoretically held the same, to a 1.8 percent contraction in Canadian economic output. By comparison, during the “Great Recession” of 2009, Canada’s (and the US’s) GDP shrunk by an estimated 2.7 percent, which is the only year Canada’s GDP has contracted since 1991, when it shrunk by 2.1 percent.

2. Canadian oil sands projects, which in 2013 accounted for roughly 60 percent of Canadian oil production, are on the higher end of the production cost range, with average break-even costs estimated (by some) to be around $80-85 per barrel. This, of course, is without even taking into account most of the environmental costs associated with its production, which tend to be substantially higher than those of other oil projects as well. Newfoundland, meanwhile, which accounts for around 9 percent of Canada’s oil production, also has high break-even costs, since it is primarily engaged in offshore drilling.

3. Most Canadian oil is of the heavy or extra heavy variety, and has a high sulphur content. There are currently very few refineries capable of handling this type of oil; most of the ones that are able to refine it are located either in the US Midwest or along the US Gulf coast. The rapid growth of oil production from shale deposits, however, which is ultra-light oil and “sweet” (meaning it has a low sulphur content), and which in most cases has lower production costs and does less damage to the environment than Albertan oil sands production does, is causing some of these refineries to be retrofitted to handle light, sweet oil instead, potentially leaving much of Canada’s oil output less valuable.

4. None of Canada’s most important trade partners are likely to be among the main beneficiaries of falling oil prices. Canada has one primary trade partner, which is the United States, and three secondary trade partners: China, Mexico, and Britain. The US accounts for more than half of Canadian trade, while China, Mexico, and Britain combined account for close to 20 percent of Canadian trade.

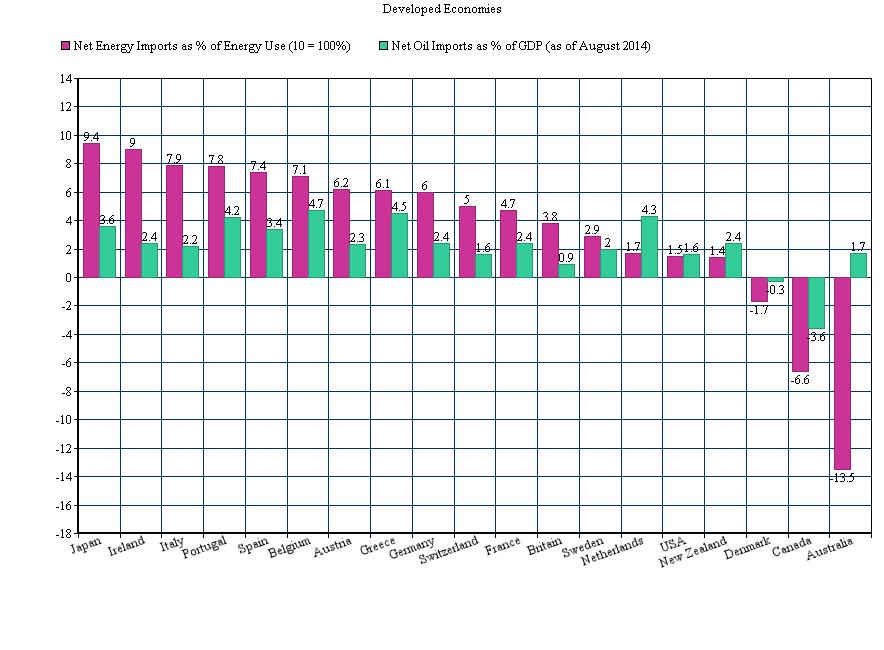

None of these four countries, however, are significant importers of oil, or of energy in general. Net energy imports account for less than 15 percent of the US’s total energy use, and net oil imports were (as of August) equal to just an estimated 1.6% of US GDP, both much lower than in most other developed economies (see graph below). In fact, if oil prices continue to fall, they might drop below the break-even prices of US shale production, Alaskan oil production, or offshore oil production in the Gulf of Mexico, which could hurt the US energy industry and grant oil market share back to the lowest-cost producers such as Saudi Arabia and the other Gulf Arab monarchies.

What is more, the US is a leading exporter of a number of commodities that may see their prices fall as a result of lower oil prices, such as coal and food. Compared to Northeast Asia or Europe, the US is also barely dependent on importing most important minerals, such as iron ore, copper, or aluminum, the prices of which often correlate with oil prices as well to a certain extent. The US is a net exporter of iron ore, in fact, which has the largest international market of any commodity apart from crude oil, and which has seen prices fall by around 30 percent in the past six months and 50 percent in the past year. (Canada, meanwhile, is the world’s fourth largest net exporter of iron ore). The United States’ wealth of natural resources could prevent it from benefiting too much from falling oil prices.

What is more, the US is a leading exporter of a number of commodities that may see their prices fall as a result of lower oil prices, such as coal and food. Compared to Northeast Asia or Europe, the US is also barely dependent on importing most important minerals, such as iron ore, copper, or aluminum, the prices of which often correlate with oil prices as well to a certain extent. The US is a net exporter of iron ore, in fact, which has the largest international market of any commodity apart from crude oil, and which has seen prices fall by around 30 percent in the past six months and 50 percent in the past year. (Canada, meanwhile, is the world’s fourth largest net exporter of iron ore). The United States’ wealth of natural resources could prevent it from benefiting too much from falling oil prices.

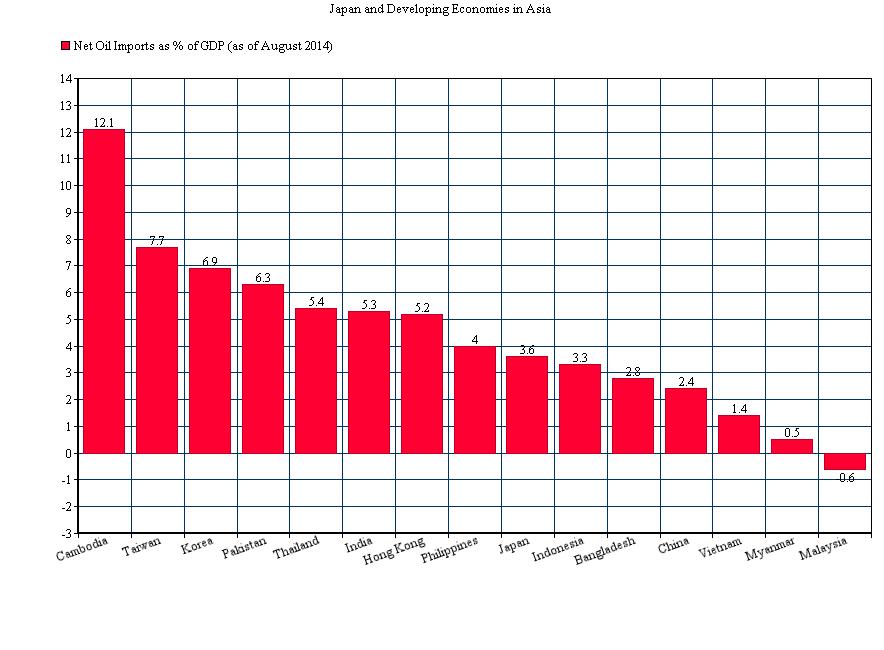

While China, Canada’s second largest trade partner, has become the world’s largest oil importer, it is actually not too dependent on its oil imports either (see graph), since it produces so much coal domestically, and coal continues to account for over two-thirds of its overall energy consumption. China is actually the world’s fourth largest oil producer, sixth largest natural gas producer, fifth largest nuclear power producer, and largest producer of hydroelectricity, wind power, and energy from biomass. Energy imports account for only around 10-15 percent of China’s total energy usage, which is many times less than in most other economies in Asia, or than most countries in the developed world.

Britain and Mexico are not significant net importers of oil either. Britain, unlike other large European economies, is only a very minor importer of oil (it is actually one of the world’s top 20 oil producers, because of the North Sea), while Mexico is the world’s 15th largest net exporter of oil and, despite importing more natural gas from the United States than it ever has in the past, also remains a net exporter of energy in general.

Britain and Mexico are not significant net importers of oil either. Britain, unlike other large European economies, is only a very minor importer of oil (it is actually one of the world’s top 20 oil producers, because of the North Sea), while Mexico is the world’s 15th largest net exporter of oil and, despite importing more natural gas from the United States than it ever has in the past, also remains a net exporter of energy in general.

Thus, Canada’s main trade partners are not likely to be among the leading beneficiaries of falling oil prices – at least, not unless their populations respond to cheaper gasoline prices by going out and spending far more money than they otherwise would have. As a result, Canada should not necessarily expect these trade partners to boost their purchases of its exports during the months ahead.

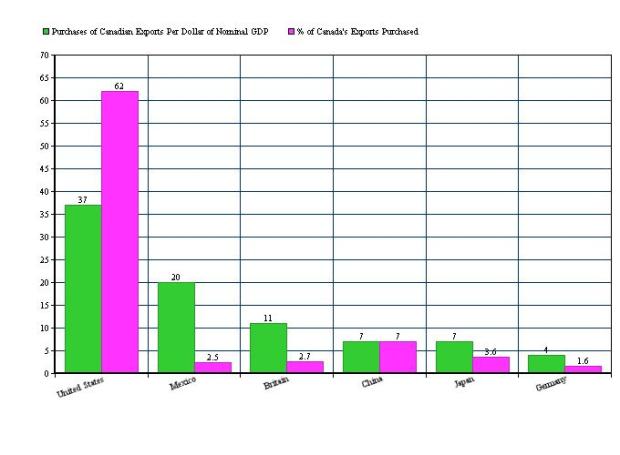

[Note: Japan’s trade with Canada may actually be a little bit larger than Britain’s or Mexico’s. However, this is only because the Japanese economy is much larger than Britain’s or (especially) Mexico’s. Per dollar of its GDP, Japan buys significantly less from Canada than Britain, Mexico, or the US do relative to the size of their own economies (see graph below). This means that British, Mexican, or American economic growth might be more likely to have a stimulative effect on the Canadian economy than the same amount of Japanese economic growth would. Similarly, Mexican growth would probably help Canada more than growth in any country apart from the US would, so it is a shame for Canada that Mexico is a net exporter of both energy in general and oil in particular] Challenge #2: Other Commodities

Challenge #2: Other Commodities

The price of oil is often correlated with the price of commodities in general, since bulk commodities tend to require a lot of energy to produce and a lot of fuel to transport. This presents an additional risk for Canada, given that Canada is not only a massive exporter of oil, but also of many other commodities. Commodities other than oil account for an estimated 20-30 percent of all Canadian exports. Most of Canada’s most important non-oil commodities have prices that tend to correlate at least somewhat with oil prices. These include not only natural gas and coal, but also industrially used metals like nickel, copper, and iron ore, as well as nonmetal commodities like potash (used for fertilizer) and timber (which in Europe accounts for half of all energy produced from “renewables”), both of which Canada is the world’s largest exporter of. Canada is also the world’s third largest net exporter of electricity, trailing only France and Paraguay, and the world’s largest uranium producer apart from Kazakhstan.

Canadian natural gas, which is by far the most valuable Canadian commodity export apart from oil, has recently been fetching prices far below the global average, since natural gas is costly to ship overseas, and since the US market is already over-supplied because gas is coming up as a by-product in shale oil production. Coal prices, meanwhile, have been hurt by a combination of falling oil and gas prices, slowing Chinese industrial growth, and concerns over pollution in various countries (China included). While coal in Canada receives little media attention because of the prominence of Canadian oil and gas, it nevertheless remains one of Canada’s top four or five commodity exports.

Canada is also the world’s second or third largest exporter of wheat, trailing only the US and maybe France. Canadian grain production tends to have relatively high break-even prices, a result not only of the latitude and climate of farmland in the Prairies, but also of the fact that the Prairies are landlocked and have no access to commercially navigable waterways (unlike US, European, or Argentinian farmland, for example), which are necessary to reduce costs given that grains are bulky goods which even today are expensive to transport long distances overland. In Canada, therefore, export revenues might be hurt more by falling grain prices than they would in other significant grain-exporting countries. The Food and Agricultural Organization of the United Nations estimates that in 2014 global food prices fell by 3.7 percent, the biggest fall since 2011, led by grain prices which fell by around 12.5 percent, with nearly all of that fall occurring during the past six months.

Finally, there is marijuana, which, though it is difficult to be certain, arguably accounts for more of Canadian export revenues than any commodity apart from oil or natural gas. Indoor marijuana production, which is responsible for a large share of Canadian production, is an extraordinarily energy-intensive enterprise, such that falling energy prices may cause Canadian producers to save on input costs. On the other hand, there is the legalization of marijuana in Washington state, which is just across the border from marijuana-growing British Columbia, as well as in states like Colorado and, most importantly, California. Legal marijuana production in the US has taken off in the past year or so, and it will probably squeeze the value of Canadian (and Mexican) marijuana exports.

Challenge #3: China

The relationship between Canada and China is based around more than just exports of Canadian natural resources to China and imports of Chinese manufactured goods to Canada. British Colombia in particular has a close economic relationship with China, the result of Vancouver’s (and Victoria’s) Pacific coastline and physical isolation from most of the rest of the Canadian and North American markets. British Colombia sends approximately 35 percent of its overseas exports to China, which is almost twice the share that the rest of Canada does, and 2.5 times the share that the United States does.

Partly as a result of this British Columbian transpacific relationship, Canadian exports to China are equal to roughly 2.5 percent of Canada’s GDP, whereas US exports to China are equal to only 1.3 of the US’s GDP. In addition, there are social and financial ties between Canada and China that are economically significant, albeit difficult to measure precisely, reflecting the fact that roughly 11 percent of British Columbia’s population and 5 percent of Canada’s total population are of Chinese origin — compared to just 1.2 percent for the US’s population, 0.3 percent for the European Union’s population, and 4 percent for Australia’s population.

All of this is to say that Canada will feel the effects of an economic slowdown in China, and not only because of the effect such a slowdown would have (and has already been having) on commodity prices. Canada could be particularly affected by a crisis in southeastern China, if one were to occur, since because of the historical connection between Canada and Britain, most of the Chinese immigrants in Canada have come from Hong Kong and adjacent parts of southeastern China (and spoke southeastern Chinese languages like Cantonese, even though Cantonese is only spoken by approximately 60 million people within China, compared to nearly a billion Mandarin speakers).

Notably, eastern Chinese provinces have had the slowest growth in China every single year since the global financial crisis. Meanwhile, Hong Kong’s economy has slowed immensely in recent years and had an especially difficult 2014, and mainland southeastern China was the slowest-growing major Chinese region in 2014. This could potentially wind up being bad news for the Canadian economy this year.

Challenge #4: The United States

According to most Canadian economic analysts, Canada’s saving grace in 2015 is likely to be the US economy, which has been rebounding to a certain extent from its relatively poor performances in 2007, 2008, 2009, 2011, and 2013, and which had particularly strong growth in the third quarter of 2014. While this assessment is probably true, it is nevertheless important to point out that the American economic recovery has not been occurring in the areas of the US that have the greatest impact on the Canadian economy.

Most of Canada’s exports to the US go to states in the Northeast or Midwest, on the borders of the Atlantic or, especially, the Great Lakes. Michigan, New York, Ohio and Illinois together receive around one-third of all Canadian manufacturing exports to the US, for example. Yet most states in this region have not performed very well during the years since the financial crisis.

With the exception of states like North Dakota, which have economies based around the production of commodities like oil and agriculture and compete directly in these industries with neighbouring Canadian provinces in the Prairies, most of the best-performing US states have not been near the Canadian border. Instead, they have been in southern or western states, most notably Texas. Ohio, Michigan, and Illinois, meanwhile, were among the slower-growing economies during that same period. These trends have largely continued during 2013 and 2014 (though, on a more positive note for Canada, the economy of Michigan has been doing decently in the past two years, and Michigan is the single largest importer of manufactured goods produced in Canada).

In addition, upstate New York, the only part of the US which borders both Ontario and Quebec, has performed far worse than the New York City metropolitan area through these years. In Michigan, similarly, growth has been stronger in the western part of the state, which does not border Canada, than in the northern or eastern parts of the state, which do. And in Ohio, growth has been stronger in southern cities like Columbus or Cincinnati, which are relatively far away from Canada and the Great Lakes, than it has been in northern, Lake Eerie cities like Cleveland or Toledo.

Falling Energy Prices and US State Economies

In spite of auto-related manufacturing in states like Michigan and Ohio, the US’s Northeastern and Great Lakes states will not necessarily be among the main beneficiaries of the fall in energy prices. New York, for example, consumes the least amount of energy per capita of any state apart from Rhode Island. Northeastern states like Vermont, New Hampshire, and Massachusetts, which have close ties with Canada, are extremely energy-efficient. The Pacific northwestern states, Oregon and Washington state, which are economically integrated with British Columbia, are also energy-efficient. And the Great Lakes are for the most part only partially energy-intensive economies (apart from Indiana, which is quite energy-intensive). Michigan consumes the 16th least amount of energy per capita, while Pennsylvania is 20th, Illinois is 25th, and Ohio is 28th.

Moreover, the area in and around the Great Lake states is one of the major energy-producing regions of North America, and therefore may not benefit as much from cheaper energy as some other parts of the US will. Pennsylvania produces significantly more energy than any state aside from Texas or Wyoming, and much more natural gas than any state other than Texas. The West Virginia-Pennsylavania-Kentucky-Illinois-Indiana-Ohio region accounts for around three-quarters of all the coal production in the US outside of Wyoming; coal production which is being squeezed by falling natural gas prices as a result of fracking.Ohio, Illinois, and to a lesser extent Michigan also produce a decent amount of oil themselves, and Michigan has the largest natural gas storage capacity of any state in the country.

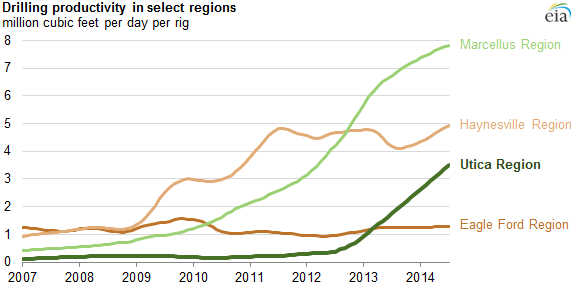

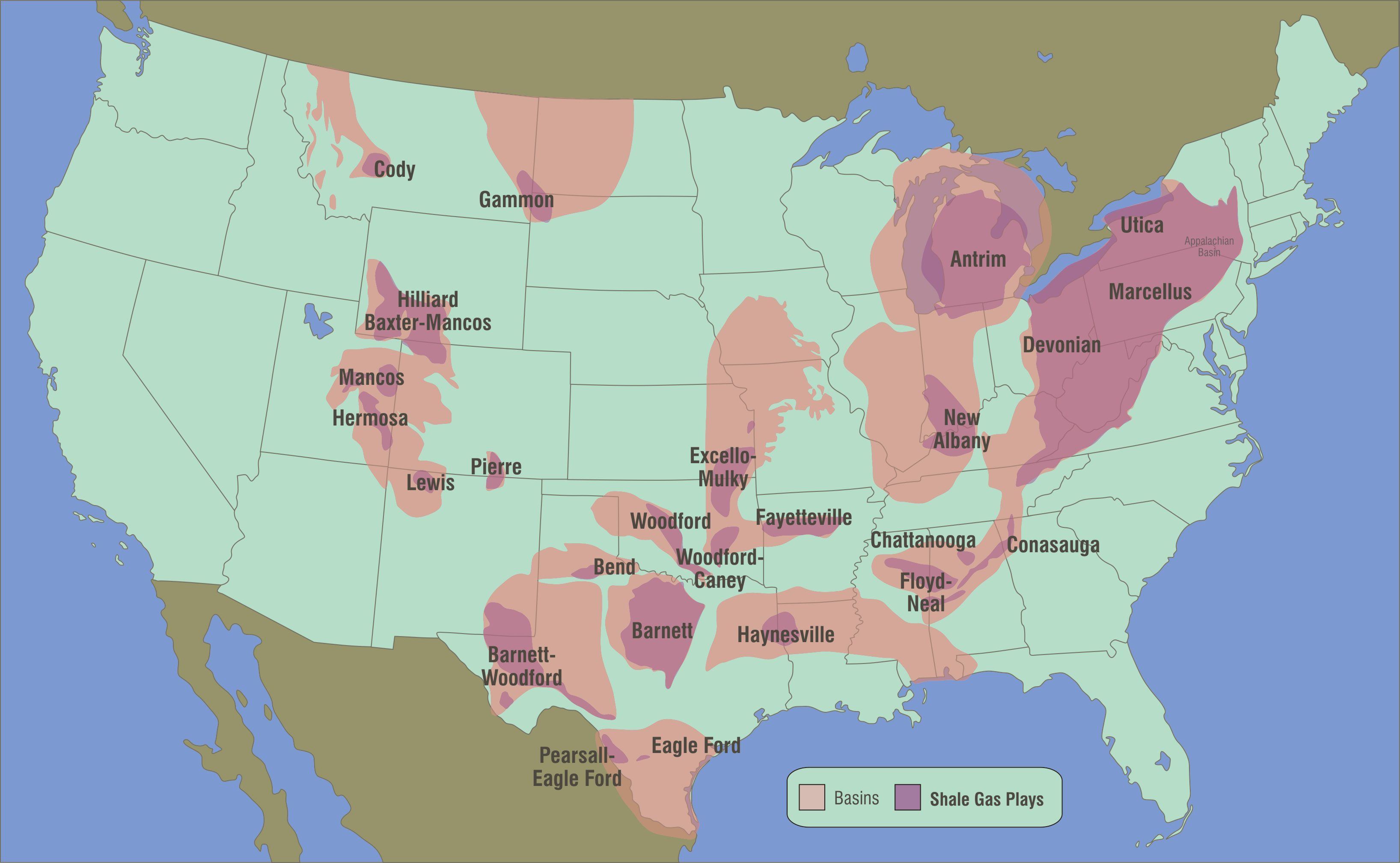

Meanwhile, the shale gas basins in this region, namely the Marcellus basin and the (more geologically challenging and expensive to develop) Utica basin, have had by far the fastest productivity growth in recent years of any major basins in the United States (see graph below). In the case of the Utica, which contains significant amounts of both oil and natural gas, the basin encompasses not only Pennsylvania, as the Marcellus does, but also other areas near Canada, like eastern Ohio and upstate New York.

In spite of their historical reputation for loving and making cars, none of the Midwestern states even remain among the top ten states in terms of per capita vehicle ownership. Even Michigan now only ranks around 15th in terms of per capita vehicle ownership. The Great Lakes/Midwest is also one of the leading ethanol-producing, iron-ore producing, and food-exporting regions in the entire world, which could hurt as food, fuel, and mineral prices have been falling. Finally, cheaper oil could make it cheaper for people living in northern cities like Buffalo to fly south or west, spending more time and money in sunnier states, or in the Rocky Mountains.

It may also be worth mentioning that, even as American growth is generally a good thing for the Canadian economy, the fact that the US is growing at a decent pace at a time when countries like Russia, Japan, Germany, Brazil, and possibly even China and Mexico are all flirting with recession means that US national power might increase at a pace that could become uncomfortable for some of the economies that have to deal with the Americans most often, potentially including Canada.

Indeed, given that US election season is approaching, American politics could perhaps become relatively erratic during 2015. The Republican-controlled Congress, the Democratic-controlled White House, or various US state governments could, for instance, place indirect restrictions on imports from various provinces or industries within Canada in order to provide a short-term protectionist boost to American employment growth. They might also run political attacks against the Albertan oil sands during the year leading up to the election: the Democrats in order to energize their environmentalist base; the Republicans (and in some cases the Democrats) in order to divert environmentalist ire away from American coal production, offshore oil production, or fracking.

Challenge #5: Canadian Politics

There is a federal election in Canada in 2015. In most countries, investors usually have a clear idea of what they want to see from an election. They want the victory of a competent, “market-friendly” candidate, with a majority government and no significant regional divisions displayed in the country’s voting patterns. This is, in fact, what they got out of the most recent Canadian federal election, in 2011: the right-of-centre Conservative Party won a decent-sized majority government (which was Canada’s first majority government since prior to 2004), winning in Ontario, British Colombia, and the Prairies, while at the same time Quebec abandoned its independence-minded Bloc Quebecois en masse in favour of the NDP, which also became the largest opposition party by a large margin in Ontario, British Colombia, and the country as a whole.

From the perspective of investors, it is unlikely that the 2015 election will be much more favourable than the current situation that exists in Canada. Even if the Conservatives were to win an even larger majority than they have now, which seems unlikely, this would still only be a continuation of the status quo, and would therefore be unlikely to generate any excitement among Canadians or foreign investors. Plus, given that the Conservative leader Stephen Harper has been Prime Minister for just short of ten years now, this status quo may start to become tiring even for investors and Conservatives. It would certainly not induce any sort of “hope and change” optimism that could potentially help stimulate markets in the short-term. In fact, Harper’s opponents will likely be spending the election campaign trying to convince Canadians that their economy has been brought to the brink of recession.

In contrast, it is not very difficult to imagine that the elections could make Canada less appealing to investors. Here’s one scenario that would be much worse from an investor’s view: the Liberal Party, led by 43-year old Justin Trudeau (the son of a former Canadian Prime Minister) wins a minority government in parliament, while, on a provincial level, the country is regionally divided in its voting patterns, with Ontario going primarily for the Liberals, Quebec voting primarily for the NDP, the Prairie provinces voting primarily for the Conservatives, and British Columbia roughly splitting its vote between the Liberals and the Conservatives.

In such a scenario, Canada would have changed from having a “market-friendly” majority government led by an experienced Prime Minister, and having no regionalist tendencies reflected in its voting patterns, to having a left-leaning minority coalition government led by an inexperienced Prime Minister and having significant regionalist divisions between eastern Canada and western Canada, as well as between Quebec and the rest of the country, reflected in its voting patterns.

If the NDP defeat the Conservatives instead of the Liberals, meanwhile, which is also possible (the NDP are currently the second largest Canadian party in parliament by far), it would bring to power a party that has never been in power before in its history, which until relatively recently was viewed by many conservatives as being “far left”, and which has a leader who is only in charge because of the tragic death of the former leader of the NDP following the party’s unprecedented success in the Canadian election of 2011. (Though notably, he is more experienced than the Liberal party leader).

Even worse, a staunchly provincialist party like the Bloc Quebecois, which is currently polling at around 10-20 percent in Quebec, could theoretically end up becoming the kingmaker in a split between the Conservatives and a Liberal-NDP coalition. Investors could turn on Canada to a certain degree if they begin to think that an increasingly fragmented result such as this is likely to occur. Thus, while the defeat of Stephen Harper’s Conservative Party or the loss of its majority position in parliament would not necessarily be bad for Canada over the longer term, it arguably represents a short-term challenge for the Canadian economy – and in particular, for Canadian financial markets – during the election year ahead.

Reblogged this on bertpowers.

Reblogged this on Don't Worry, Be Happy.

Thanks for following sciencesprings. I appreciate it very much.

Reblogged this on Vaibhav Gupta and commented:

Interesting Read

Well researched and very thought-provoking!

thank you!

Reblogged this on Guyanese Online.

You’re analytical style is outstanding. Would you consider doing an article on the economic pros and cons of an Iran deal, as well as the array of possible outcomes? My concern is the advanced missiles that Iran will be buying from Russia with its signing bonus, and what would stop it from breaking the deal in 3 years once these missiles are installed and its oil facilities have been modernized.

Hey, thank you very much. I’ve written a few articles about the Iran deal that you can read about on this site.

“Your” analytical