It is probably just a coincidence, but there is a strong correlation between being a member state of the Eurozone and being dependent on energy imports. The Eurozone imports upwards of two-thirds of the energy it consumes (compared to just 10-15 percent for the US and China, and 30-40 percent for Britain and India); only two of the Eurozone’s 19 members import less than 47 percent of the energy they use. These two Eurozone outliers are the Netherlands and Estonia, which import just 17 and 10 percent of their energy consumption, respectively.

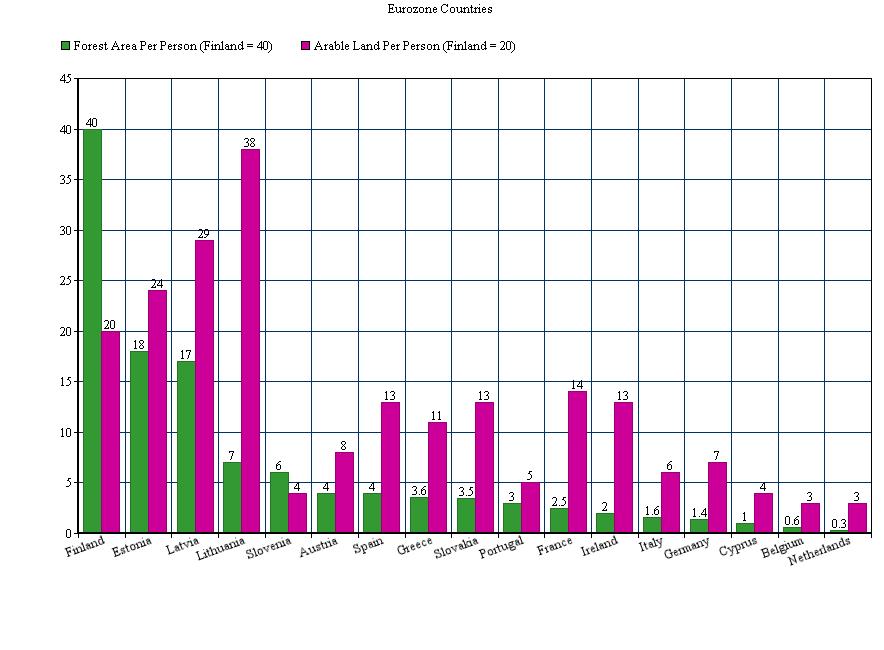

Estonia is a greater exception still. Unlike in the Netherlands, where, as recently as August, net oil imports accounted for an estimated 4.3 percent of Dutch GDP, in Estonia oil imports only accounted for 2.3 percent of GDP, the lowest share in the Eurozone apart from Ireland or Austria. Estonia is also a transit state for Russian exports of oil and coal, owns large reserves of oil shale (not to be confused with shale oil) and biomass energy (see graph below), and had been expected, prior to the recent collapse in oil prices, to have the European Union’s fastest-rising diesel fuel production during the next few years. Estonia also has by far the most oil stored up of any European country, relative to the pace at which it consumes oil. In other words, Estonia is unlikely to benefit from cheap oil, or from lower energy prices in general, to the same extent as other Eurozone countries.

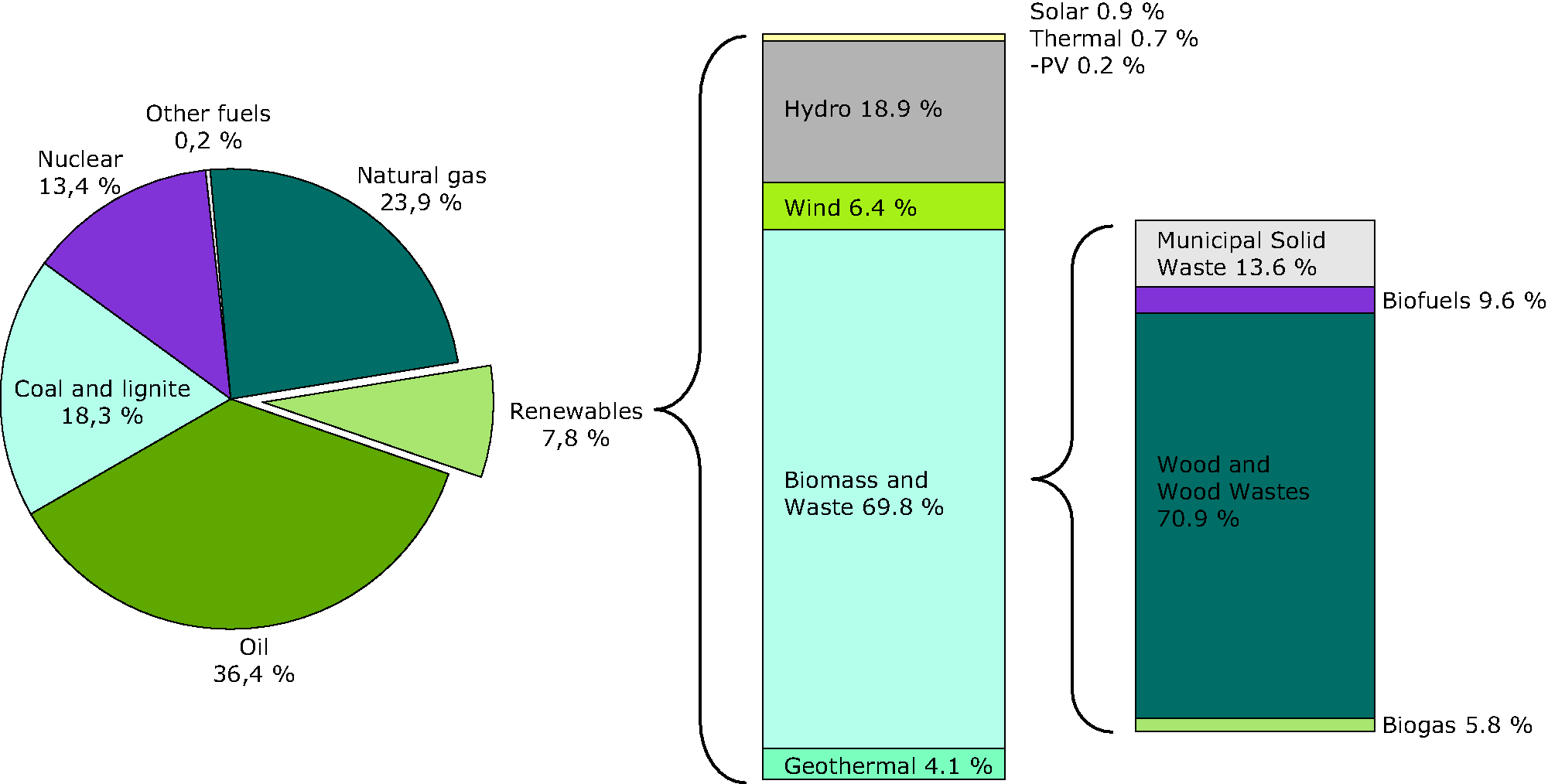

Europe’s energy use mix, with emphasis on biomass sources, particularly wood:

Europe’s energy use mix, with emphasis on biomass sources, particularly wood:

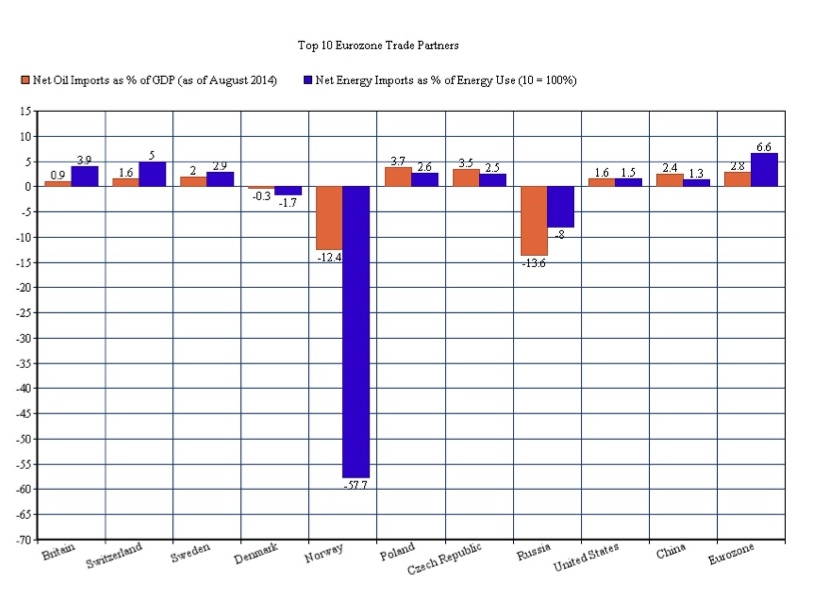

For the Eurozone as a whole, oil imports were equal to an estimated 2.8 percent of GDP, which is much higher than in the nations the Eurozone trades with the most (see graph below). Falling oil prices should cause the value of the Euro to rise against the currencies of most of its top trade partners, therefore; at least, assuming that a declining Eurozone economy did not cause the oil price drop in the first place. Indeed, the Euro has already risen in value relative to the currencies of Russia, Norway, Sweden, Poland, and the Czech Republic since the oil price plunge began (though admittedly, it has also fallen in value relative to the currencies of the US, Britain, Switzerland, Denmark, and China).

(Eurozone stats are at the far right of the graph)

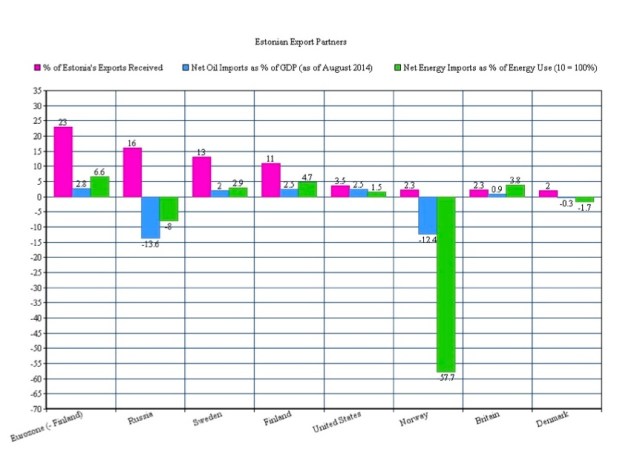

This does not necessarily bode well for Estonia, however, which, in spite of not benefiting much from cheaper energy, may nevertheless have to cope with the effects a strengthening Euro could have on its export competitiveness. Unfortunately for Estonia, its exports are equal to almost 90% of its GDP, and they go mainly to non-Eurozone economies like Russia and Scandinavia, which are hardly dependent on imports of oil, energy, or commodies in general (see graph below).

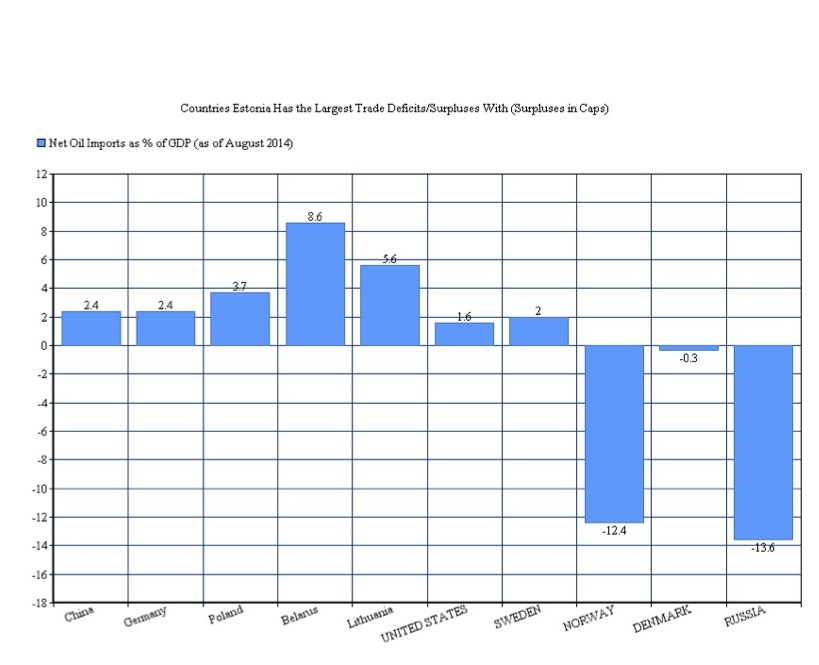

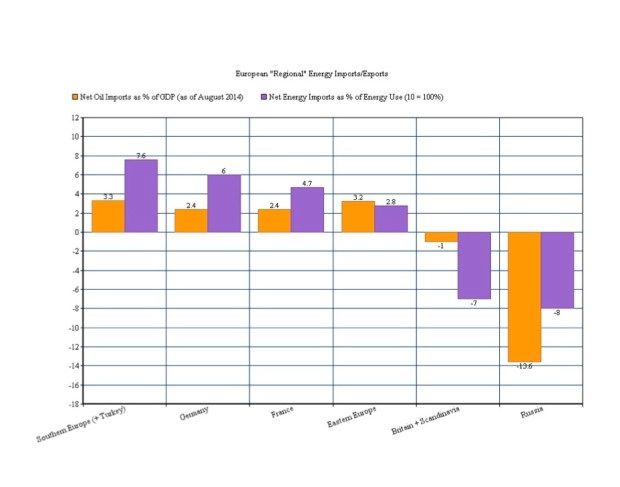

Indeed, this characteristic holds true not only for Estonia’s largest export partners in absolute terms, but also of the countries with which Estonia enjoys the largest trade surpluses (see first graph below). Even worse, the biggest European beneficiaries of cheap oil and energy are nearly all situated next to the Mediterranean, the part of Europe Estonia exports to the least (see second graph below).

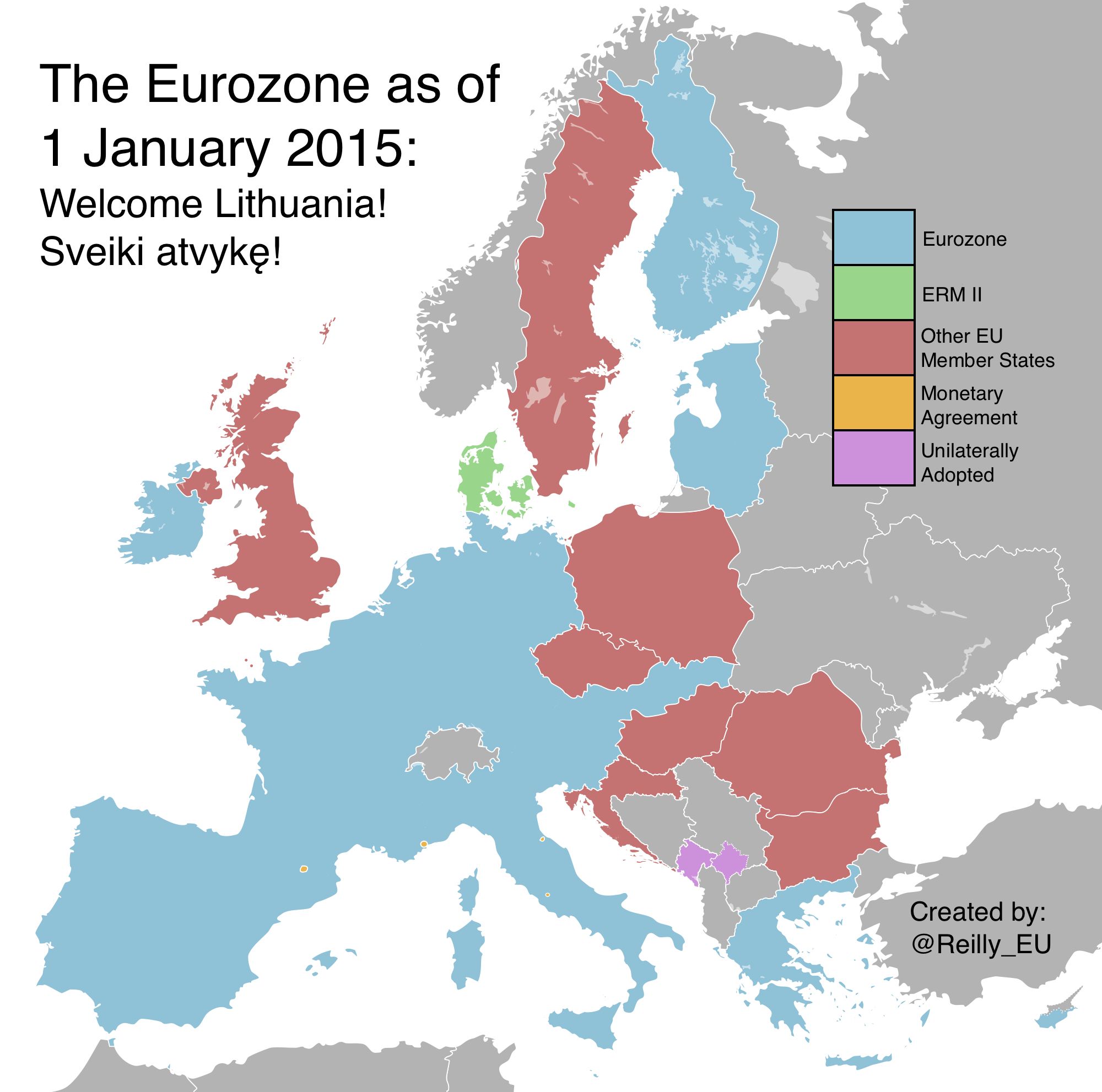

So, was Estonia’s 2011 decision to join a currency union which contains only one of its four largest export partners, and within which it is has an intensely outlying energy-import dynamic, a financially sensible move? Or was it rather the case that Estonia adopted the Euro primarily in order to proclaim its Europeanness (and non-Russianness), and so might now have to face some of the adverse economic consequences of the decision, at least where its exports are concerned, given that oil prices have dropped by well over 50 percent since October?

In addition, what effects might falling oil prices have on Estonian politics? Estonian elections are approaching this March, and a large majority of Estonian energy production is located in the part of Estonia in which nearly 75 percent of the inhabitants are ethnic Russians (who also comprise an estimated 25 percent of the overall Estonian population). Russia remains Estonia’s largest trade partner, and Russia’s ruble has already declined by one-third in value against the Euro since October. The Estonians are also tied to the Finns, their second largest trade partner, with whom they speak an extremely similar language (which is also extremely dissimilar to all other languages in Europe) — and Finland too has a national election coming up, in April.

Meanwhile, Russia’s two major NATO geopolitical rivals, namely the US and Turkey, as well as Russia’s largest NATO economic competitor, Canada, which is also home to the West’s biggest Ukrainian diaspora, are having elections this year as well (the US primaries are not until 2016, but the election will effectively begin in mid-2015). These elections could certainly cause NATO relations with Russia to deteriorate, even beyond the low point they are already sitting at. Indeed, a relatively robust American economic recovery could force the US Republican Party to make foreign policy the central focus of their political campaign – and perhaps specifically, to obsess over the chummy “Reset” with Vladimir Putin that Hillary Clinton initiated during her tenure as Secretary of State – which could thrust the Baltics, the sole ex-Soviet republics that are now firmly a part of NATO and the West, into the global spotlight. It could be an interesting time ahead for tiny Estonia, to say the least.

2 Comments