The Korean War, fought from 1950-1953, was a result of two earlier wars in the 1940s: the US-Japanese War, which ended with the destruction and occupation of Japan in 1945, and the Chinese Civil War, which ended in a Communist victory (and Nationalist retreat to Taiwan) in 1950. With the Communists and Americans as the only powers in East Asia following these wars, the Korean peninsula was split in two, each side taking a piece for itself.

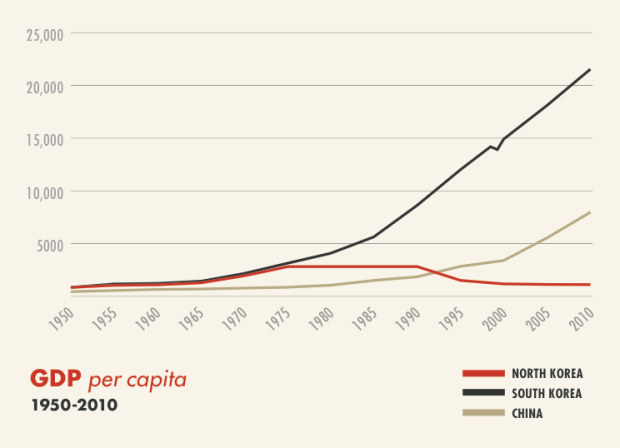

When the US triumphed over the Soviet Union around 1990, many expected the North Koreans to fix their broken ties with South Korea. That this did not occur was partly the result of inertia, partly the result of Kim Il Sung’s living until 1994, and partly the result of the 1997 East Asian financial crisis, which kept the South Koreans too poor to want to incur the cost of investing in North Korean infrastructure or labour.

It was also partly the result of a miscalculation on behalf of North Korea in 1987, twenty-four months before the Berlin Wall came down. Seeking to ruin the South’s first-ever Olympics in 1988, the North blew up a commercial airplane. It was by far the deadliest attack on the South since the armistice began in 1953. South Korea’s anger and mistrust of North Korea as a result of this deed persisted during the ’90s.

When the 21st century arrived the situation changed again. The US, after having fought the bulk of its four major 20th century wars in East Asia—in the Philippines, WW2, Korea, and Vietnam—shifted its focus elsewhere in 2001. This shift was mainly a result of US wars in Afghanistan, Iraq, and Libya. To a lesser extent, it has also been a result of recent Russian interventions in Georgia, Ukraine, and Syria .

In East Asia, meanwhile, China’s GDP surged, while Japan’s continued to stagnate like it had in the ‘90s. Between Chinese growth, Japanese stagnation, and US distraction, East Asia became again a two-power region: the United States and China now dominate the region. But this may now be ending. In the years ahead, East Asia is likelier to become either a one-power region, like it was in 1990s, or a three-power region (the US, China, and Japan). The two-power status quo could remain in place, but is hardly certain to do so.

In a one-power or three-power region, the powers involved may have less to gain from the continuation of poor relations between North and South Korea. There will be much less reason to split Korea in two, as it has been for 67 years now, when East Asia as a whole is not split between two major powers, as it is today.

The move towards a one-power East Asia, or towards a three-power East Asia, is plausible for three reasons:

First, the US has been drawing down from the Middle East. It had 150,000 soldiers fighting in Iraq and Afganistan in 2011, but now has fewer than 15,000. Unless it decides to wholly reverse this process — Trump has announced the addition of 4,000 soldiers to Afghanistan, but that is a far cry from the Obama-era surge—the US will have the ability to focus on other regions, like East Asia, more than it could during the 2000’s.

Second, China’s GDP growth has slowed, from 10-15 percent growth during the 2000s to 3-7 percent (depending on whether you believe its official growth rate, 6.7%) last year. In order to keep up with 2.5 percent US growth, China must grow around 4 percent. China’s challenge in doing this is that its labour is now much costlier and older than it used to be, while its resource wealth, most notably its coal, has led to pollution.

China may struggle to keep up with US power. As it is, the US economy is an estimated 1.6 times larger than China’s. [The US-Canada-Britain-Australia alliance, meanwhile – which, unlike China itself, more or less speaks a single language – has a GDP 2.2 times larger than China’s]. The US GDP alone is larger than that of East Asia as a whole.

Third, the economy of Japan, which today is an estimated 37 percent as large as China’s and 18 percent larger than Germany’s, is likely to benefit from the crash in oil and other natural resource prices that began in mid-2015. Unlike China, Japan has few resources of its own, and so depends on imports to fuel its economy.

While Japan’s aging population continues to be a challenge — Japan’s largest age cohorts are 40-45 year olds and 65-70 year olds — it may be able to address the challenge via automation, immigration, and a labour force dominated by technically skilled 50-80 year olds. Japan is already planning to advance its robotic prowess in the near term, as it wants to showcase them at the 2020 Tokyo Olympics.

Japan’s robot drive is likely to have consequences not just for the Japanese economy, but also for the Japanese military. Japan has already begun to rebuild its military of late, first in response to China’s rise and then in response to Donald Trump’s rhetoric that US allies should “stop freeloading, and pull their own weight”. Already today the Japan ranks 8th in military spending, despite devoting just one percent of its GDP to it. Should Japan double this, to reach the 2 percent of GDP that France and Britain spend, it would then become the third largest military spender in the world, and move far ahead of the next largest, Russia. (Were Japan to spend 5 percent of GDP on its military like Russia does, it would move far ahead of China).

Even if Japan does not re-emerge, East Asia might not remain a two-power region. Rather, China could fall behind the US sufficiently that, in effect, it will be a one-power region again, like it was in the 1990s. US power is rising not only due to its withdrawal from the Middle East, but also because its rivals, most notably Russia, are being hurt by the fall in resource prices. As in the ’90s — when oil prices were at all-time lows — cheap oil works in the US’s favour. And if US power in the region does rise, the North Koreans might be less willing to resist its demands.

There is an additional reason for improving relations between the North and South: it may benefit the South’s economy. Unlike in the 1990s, South Korea is now a relatively wealthy country. Yet because of its rapid growth, it has become dependent on imports of natural resources and exports of manufactured goods. South Korea has been importing resources mainly from the Middle East, and exporting mainly to China.

The Middle East, however, remains unstable. Qatar, for example, the world’s largest LNG exporter, sells more to South Korea than to any other country. But Qatar is now in open conflict with Saudi Arabia. Uncertainty of this kind threatens South Korea’s GDP growth. In addition, as China tries to shift from coal to gas, and as Japan tries to shift from human labour to fuel-powered robots, South Korea may have to deal with rising competition from its own enormous neighbours when importing fossil fuels from the Middle East.

Similarly, South Korean exports have been limited by the slowing Chinese economy. China accounts for a quarter of all South Korean exports, more than the US and Japan combined. South Korea has also been hurt by its own success: its labour is no longer so cheap like it was in previous decades, when it was still a poor country. For these reason, South Korea has already grown more slowly in the past two years that at any time since 1997 (excepting the global financial crisis in 2009).

These economic troubles are occuring at a bad time for the South. South Korea will host the the first-ever Winter Olympics in continental Asia this year. It wants the world’s perceptions of itself—namely, that it is a remarkable country, with remarkable companies like Samsung and remarkable economic prospects in general—to endure. It also does not want the North to cause trouble this time, as occured in 1987.

Trading with North Korea could help address both these concerns. North Korea has an extremely cheap, Korean-speaking labour force; a labour force that includes cousins, and in some cases even siblings, of the South’s. It represents a potential Korean-speaking market for South Korean exports, both of media and manufactured goods. It even, if ties improve enough, offers opportunities in tourism. And it offers access to natural resources. The North Koreans are rich in coal; the South Koreans are top coal importers. More importantly, the North offers a land route by which South Korea can access resource-rich Manchuria and Siberia.

It is possible, of course, that the Korean issue will be addressed by war rather than by trade. In the past year alone, the US has prepared for such a war. It is also possible that the North will not be addressed at all; that the tyrannical staus quo will endure. But for the reasons outlined above, I believe reconciliation is the most likely, and the status quo the least likely.

Dennis Rodman, who played on the the 1990s Chicago Bulls (Kim Jong Un’s favorite basketball team) has lately met with Un. Do not be suprised if Rodman’s Celebrity Apprentice co-star, Donald Trump, follows suit.