Conventional analysis of Korea seems to be incorrect in its view of the probability of North-South reunification. The conventional view is that reunification grows more unlikely as the disparity in wealth between the North and South (now far greater than that between West and East Germany in the 1980s) continues to increase, and as young South Koreans, who tend to be more opposed to reunifying with the North, come of age.

While we have no way of knowing what the odds of reunification are, we should recognize that the logic behind these conventional views is not sound. Most South Koreans are Baby Boomers or senior citizens, so the issue of young Koreans tending to oppose the idea of reunification may not be nearly as relevant as one might think, even if we do accept the premise that public opinion will help determine the relationship between the two Koreas. An estimated 58 percent of South Koreans in general favour reunification.

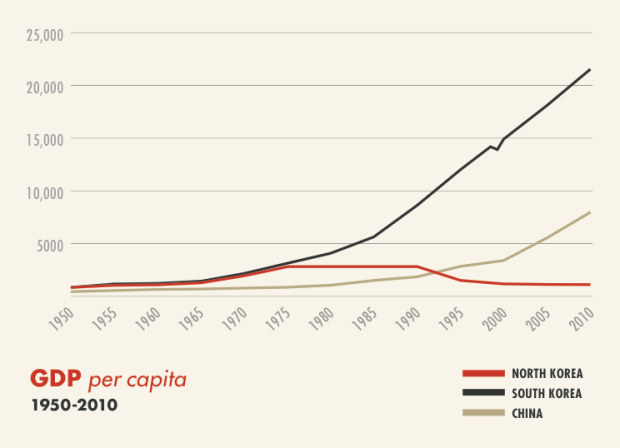

As for the enormous economic disparity between the North and the South, it might actually make reconciliation between the two Koreas more probable, not less probable. This is because it makes opportunities available from economic arbitrage higher for both sides.

Unlike in previous decades, North Korea and South Korea today have complimentary economic resources and needs. South Korea’s primary resource is capital, which the North needs if it is to finally escape extreme poverty. The South’s primary need is to bolster its increasingly expensive and rapidly aging population (see Figure 1, below), as well as safeguard the imports of fuel and exports of manufactured goods upon which South Korea depends more heavily than does any other major economy (see Figure 2).

The North’s resources are its cheap labour, coal reserves, and land bridge linking South Korea to China and to Russia.

The North’s resources are its cheap labour, coal reserves, and land bridge linking South Korea to China and to Russia.

Working together, either through a reopening of trade and investment channels or through eventual reunification, the South could provide capital while the North provides labour, energy, and direct access to the labour and energy of Northeast China and Pacific Russia. Given the vulnerability of South Korea’s existing trade routes to Europe and the Middle East, which pass the Straits of Hormuz, Malacca, Taiwan, Bab-el Mandeb, and Suez, none of which South Korea has any control over, it is not difficult to see why trading with the North might appeal to the South.

In this context, the current Olympics reconciliation between the two Koreas should not have taken so many people by surprise. (The Olympics reconciliation also should not have been such a surprise because it was preceded by South Korean officials announcing, in March 2017, their intention for South Korea to present a joint bid to co-host the football World Cup in 2030 with North Korea, China, and Japan). This is not to say that theOlympics indicate that a real push towards reconciliation will now occur, let alone a push for reunification. Still, these outcomes should not be ruled out, just as the thaw in the relationship that has taken place at the Olympics should not have been ruled out.

Let us take a brief look, finally, at the current politics/economics of the four outside powers that surround and influence the Koreas: China, Japan, the United States, and Russia.

China and Japan both have leaders who have recently gained in prominence: Xi since the Party Congress this past October, Abe since the Japanese election this past October. China and Japan are both scrambling for access to energy: China to replace coal in order to reduce pollution, Japan to replace nuclear power in order to avoid another Fukushima incident. Both countries are also scrambling for labour: Japan because of its elderly population, China because of wage inflation, the impact of the one-child policy, and the aging of Chinese Baby Boomers. South Korea, which is also increasingly in need of energy and labour, will find it difficult to compete with these two giants. The only place where South Korea may have an edge over China and Japan is its fellow Korean state, North Korea.

This competition among the Northeast Asian economies might increase even more if the United States follows through on President Trump’s pledges to reduce the US trade deficit, get tough on China, and prevent allied nations like South Korea, Japan, and Germany from “free-riding” on the global sea-lanes protection that has been provided by the United States navy. Meanwhile, with the number of US soldiers in Afghanistan having been reduced from around 100,000 in 2011 to only around 11,000 today, the US may now have the ability to threaten the North Koreans more than at any time since September 11, 2001.

Russia, in contrast, is now focused on its engagements in both Syria and Ukraine, which may limit its ability to aid its historic ally North Korea. Russia’s economy is limited too, as a result of the low oil, gas, and coal prices that began in 2015. Russia depends on exporting energy to Europe, but if those exports are imperilled, whether because of worsening relations between Russia and Europe or because of the US’s new transatlantic exports of oil and liquified natural gas, Russia may have to diversify its trade patterns by exporting to East Asia. The Russians are, however, afraid of both China and Japan, and so prefer to trade with the Koreas instead. It is therefore increasingly in Russia’s interest to see reconciliation between the Koreas, so that Russian exports can reach the South via the North and so that the Koreas’ economies and demand for Russian resources can grow.

In closing, we should perhaps begin to consider the Korean situation in the same way that an experienced investor views financial markets: aware of the significance of arbitrage, and aware of the maxim that past results are not a proper indication of future returns. In other words, we should not assume that the North’s isolation and totalitarianism will necessarily continue, and we should not think that the Koreas’ diverging paths means they are less likely to re-converge going forward. Of course we should not be naive about the character of the North’s regime, and we should not be overconfident in assuming it will change. But neither should we discount the possibility of reunification, whether achieved through diplomacy, assassination, or war. Not even in 2018.