American coal companies’ stock prices have crashed in recent years, in response to the triple-whammy punch that is the US fracking boom, the environmentalist movement, and the slowdown in the Chinese industrial economy. As recently as January of 2016, the Dow Jones US Coal Index had lost around 92 percent of its market value since mid-2014, more than 97 percent of its value since 2011, and more than 98 percent of its value since its all-time peak in 2008.

Now, it may be that coal really is finished as a major industry in the US, but there is no reason to be certain about this. The market’s plunge is arguably more a sign of investor panic than of rational valuation: coal still accounts for around a third of US electricity generation and close to 40 percent of electricity generation worldwide. The economic outlook for the coal industry does not seem to have collapsed to the extent the Dow Jones US Coal index might suggest.

1. Climate Change

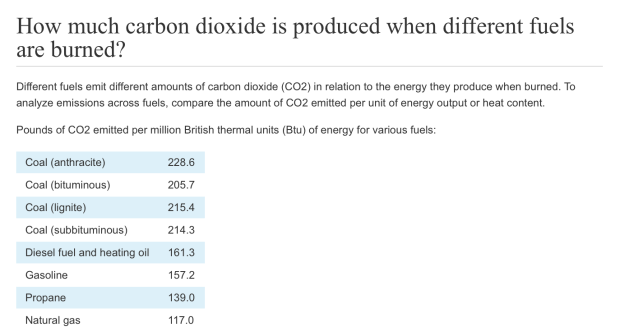

Burning coal is generally considered to be around twice as carb0n-intensive as burning natural gas. Carbon dioxide, however, is hardly the only culprit where climate change is concerned. Methane emissions are also a crucial component to climate change, for example, and industries like natural gas and meat production can be more methane-intensive than coal.

Thus far the natural gas industry, food industry, and many in the US government have neatly sidestepped the methane issue, refocusing American public attention toward carbon dioxide. They have done this by using the “we need to protect the planet for the sake of our grandchildren and future generations” approach. Methane emissions, after all, only contribute directly to global warming for a few years or decades at a time, whereas carbon dioxide can remain in the atmosphere for many centuries.

The truth, though, is probably that this is deliberately misleading. Future generations may be perfectly capable of handling whatever climate change comes their way, or of removing carbon dioxide from the atmosphere. The really dicey climate change period is more likely to occur within the coming years or decades, when the world is not yet technologically advanced enough to protect vulnerable human (and animal) populations. Within such a time frame, emissions of gasses like methane can be even more impactful than carbon dioxide.

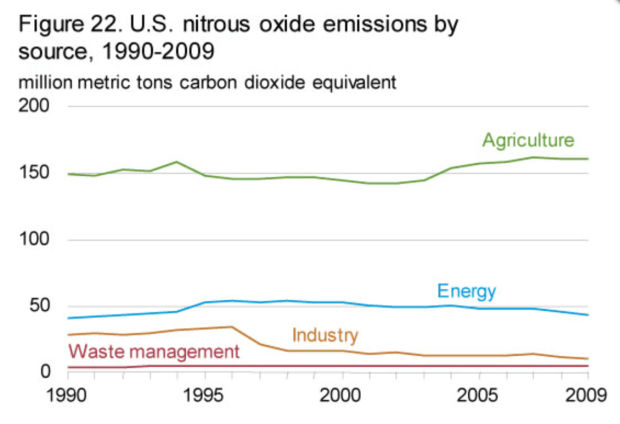

Today US methane emissions, measured in kilotons of CO2 (carbon dioxide) equivalent, are around ten percent as high as carbon dioxide emissions. Since the impact of each kt equivalent of methane upon global warming can be up to 80-90 times higher than carbon over the course of a twenty-year period, however, the overall effect of methane emissions can perhaps be worse for climate change than carbon emissions can.

Indeed, while the direct impact of methane fades over time, the indirect impact of methane emissions could remain for decades if they help to trigger a global warming feedback loop; for example, if it helps to cause sun-reflecting polar ice to melt, which could warm the planet and so cause even more polar ice to melt.

Thus, methane emissions arguably deserve more public attention and regulation. And if they are regulated, it may weaken the natural gas industry relative to the coal industry, as the gas industry in the US accounts for almost triple the methane emissions that coal does. Just this month, the US federal government has launched its first ever package of methane emission regulations for the oil and gas sector.

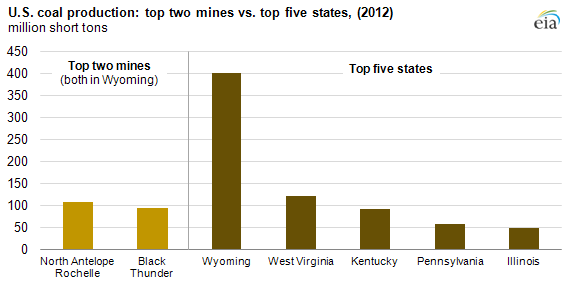

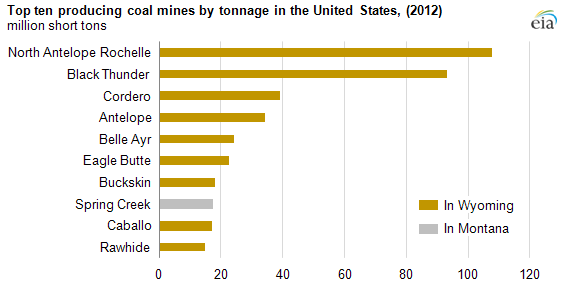

Methane, which is the main component of natural gas, can also be captured and then stored or used to produce energy. Capturing methane from the natural gas industry, however, is extremely difficult to do, because the gas sector is diffuse, consisting of hundreds of thousands of wells spread across dozens of states as well as in offshore fields in the Gulf of Mexico. Capturing and making use of methane that is released from coal mines could perhaps be easier to do, since coal production is more concentrated than gas or oil. There are only about 1000 or so coal mines in the country, and they are located mostly in Wyoming or the Midwest.

Another thing to note is that while burning natural gas is only a bit more than half as carbon-intensive as coal, much of the natural gas production in the United States comes as a byproduct of drillers trying to produce oil. This means that US gas is actually more carbon-intensive than it seems, since it would not be produced as much if the US was not also producing so much oil, and oil (or gasoline) is more than three-quarters as carbon-intensive as coal is.

This also raises the question: will the price of oil in the US remain low? If it does, it is likely to result not only in a reduction in oil production, but also in natural gas production (again, because natural gas is frequently a byproduct of oil), which in turn could cause coal to become more competitive relative to natural gas.

Oil in the US is used mainly for transportation, so it is possible that the revolutions now taking place in the transportation sector – for example, Uber (and companies like Uber), UberPool, Zipcar, electric vehicles, hybrids, e-commuting and e-commerce, using smartphone apps to make express busses finally become feasible, being able to watch a movie or do work on your smartphone or tablet while you are taking public transit or being carpooled, and the development of self-driving vehicles – could lead to such a reduction in oil use.

In the case of electric or hybrid vehicles, this could also lead to a major increase in electricity usage, potentially helping the coal industry at the expense of the oil and gas industry. And while electric cars may not soon be appearing in every driveway, it may not be too long before a widespread network of electric or hybrid Uber-esque vehicles and Zipcar-esque vehicles come into place.

If, moreover, self-driving vehicles do become a reality as well at some point, it could make vehicle-sharing services like Uber and Zipcar even more competitive, and could allow electric Uber vehicles and Zipcars to drive themselves to (and wait in line at) the nearest battery-charging station. This is an important factor, given that fully charging an electric vehicle often takes several hours.

—

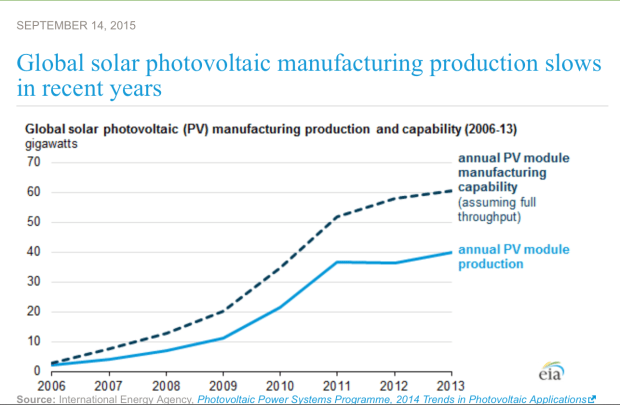

Of course, many people think that coal is likely to lose out not only to natural gas, but also to alternatives like solar energy, which emit relatively little carbon dioxide, methane, or any other type of greenhouse gas. However, it is still not clear when or if industries like solar will be able to compete on a large scale with coal in developed economies like the United States.

Much has been made about the falling cost of solar panels They are often said to have become more competitive as a result of technological improvements, and are expected to continue doing so going forward. In fact there is an alternative plausible explanation about what has driven the falling cost of solar panels: government support in East Asia (especially China), Europe, and to a lesser extent North America. The solar industry may have benefited from attempts by governments in these regions to stimulate their slowing industrial sectors and reduce pollution at the same time.

If this explanation is true, then it is possible that the cost of solar panels going forward will not continue to fall as much as people now expect them to. Indeed, if China’s economy has the “hard landing” some fear it will, panel prices could even rise a lot as solar panel manufacturing output collapses.

Ultimately, though, climate change threats will continue to hamper the coal industry, unless at least one of two things happen. The first is large-scale carbon capture and storage. Though carbon capture and storage has been over-hyped in recent years , it cannot be ruled out entirely either. We will discuss this further below.

The second is climate change fatalism. If it becomes accepted that we already well past the point of being able to reverse global warming, then the priority could shift away from reducing carbon emissions and instead become achieving rapid economic advances in order to pay for the huge, global effort that adapting to climate change will entail. Ironically, coal could be employed as the cheap, plentiful resource used to spur such rapid economic growth. If this sounds a bit crazy, bear in mind that it is the approach that India and China are already implicitly (and at times explicitly) embracing at the moment. India in particular is still planning on building many new coal plants in an attempt to achieve economic growth.

Bangladesh, perhaps the most climate endangered among the world’s hugely populous nations, has resisted climate change fatalism. However if it runs out of hope that the world’s major economies will take the necessary measures to mitigate climate change, then it could end up getting on board with this philosophy too, since it desperately needs economic growth to lift its population out of the immediate poverty it faces.

Countries like Bangladesh have, in addition, been publicly toying with the unorthodox idea of purposely releasing gasses like sulphur dioxide into the atmosphere in order to deflect sunlight and thus reduce global temperatures. Indeed, certain industries already produce this effect over a limited timespan, due to the sulphur dioxide they emit. Such industries include coal-fired power plants and container shipping.

According to this article from the Guardian, the container shipping industry alone, over a five-year lifespan, may contribute a cooling effect significant enough to offset the warming caused by every car, bus, and airplane in the world combined. Still, this cooling effect diminishes over longer timespans as sulphur dioxide leaves the atmosphere, and, in any event, sulphur dioxide emissions also cause significant local pollution, such as acid rain.

2. Local Pollution

A lot of the most concerted pushback against coal has seemed like it is driven by fears of climate change, when really it is driven to a substantial extent by frustration with more local forms of pollution that the coal industry creates. In order for local anti-pollution activists to gain public support, they often, quite understandably, use climate change as a cover.

The threat of climate change alone, without local anti-pollution activism, has a more difficult time of creating meaningful pushback, because climate change is far less of an immediate and concentrated danger than localized pollution is. Pushback against local pollution, for example, historically played a significant role in causing American industry to outsource to places like China that were more willing to tolerate it. This is also, by the way, one reason why methane emissions have gotten off the hook compared to some other types of greenhouse gasses, including carbon dioxide: methane causes far less local pollution, even though its contribution to global climate change can be severe.

If coal can overcome its local pollution problem, then, it may be able to revive itself to some extent even in spite of the role it plays in global climate change.

There is a way that the coal industry may reduce its local pollution problem: disassemble and reassemble coal-fired power plants and relocate them to more sparsely populated areas, and largely mechanize the operation of coal-fired power plants and coal mining sites.

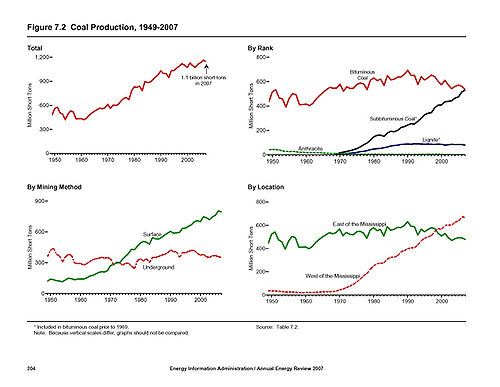

The mechanization of the coal industry is already well on its way (see graph below) and will probably continue in the coming years as a result of the “robot revolution”. Moving coal-fired plants to less populated areas would of course be enormously expensive; it would require not just moving the plants themselves, but also the building of new electricity lines.

Finding cheap routes to build electricity networks through is no easy task, nor is maintaining such electricity networks once they are already built. Plus, the longer the route, the more electricity is lost in transmission – and the routes would have to be quite long in order to locate the power plants in sparsely populated areas. Still, it could happen, if coal can remain cost competitive with other energy sources. More on this in the next section.

Local pollution is also a major reason why urban and suburban areas may start to use a lot of hybrid, electric, or Uberpool-esque vehicles, since conventional gasoline-powered vehicles create a lot of air pollution (and noise pollution) in areas in which lots of people live. Hybrids, if they can become cost-competitive with conventional cars, are ideal in this regard, as they typically cause air pollution only on rural or ex-urban roads where fewer people live.

If electric vehicles become common, it could boost demand for electricity (helping coal, potentially) and decrease demand for oil (helping coal by causing less natural gas production, potentially).

Finally, local pollution is most harmful in places where there are lots of physically vulnerable people; i.e. in densely populated countries where there are many young kids or senior citizens. The United States does not fit this description, as it is sparsely populated and most of its population is in the prime of their lives. The developing world, on the other hand, is often very young and densely populated, while Western Europe, Japan, and increasingly even China are old and densely populated. Pushback against local pollution in China in particular could cause some industrial activity – and its attendant demand for electricity – to relocate to North America.

3. Robots

Robots could benefit the coal industry in multiple ways. First and most obviously, they are likely to cause American electricity demand to soar, because robots are often extremely energy-intensive to use and because they could lead manufacturing that in previous decades has been outsourced to countries like China and Mexico to be brought back to the United States.

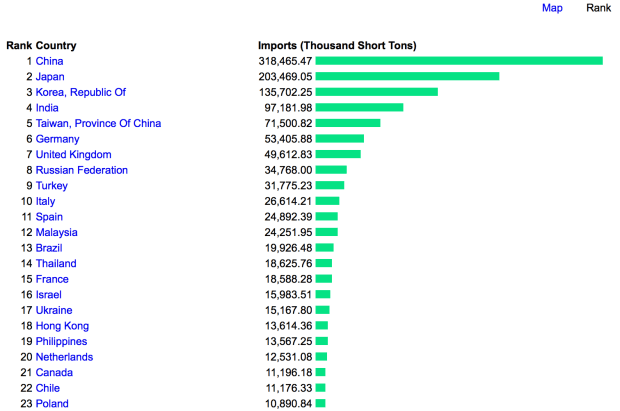

The same is true in other developed economies, like Japan, South Korea, Taiwan, and Hong Kong, which are already totally reliant upon coal and other fossil fuel imports to power their economies. In 2014, Japan and especially South Korea were the biggest purchasers of US coal, with the exception of the Netherlands (a European trade hub), Britain, and Brazil. East Asia is also the primary destination for more than three-quarters of Canadian exports of coal, which are split about equally between China, Japan, and South Korea.

Indeed it seems like ancient history now, but prior to United States sanctions on Japan in the 1930s, Japan was getting around 60-80 percent of its oil imports from the United States. It is not totally out of the question that a somewhat similar pattern could re-emerge, with the US exporting fossil fuels to East Asia once again, as the US may want each of these countries to remain strong enough to “contain” China.

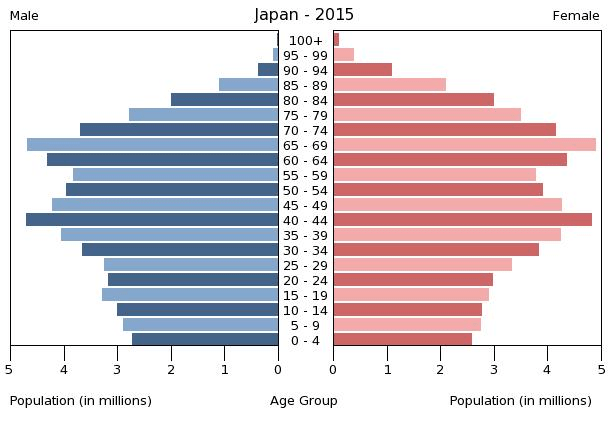

South Korea and Taiwan are particularly dependent upon energy imports (see graph above). And the United States is very approving of its alliances with these two countries because they help to “counterbalance” (to use another geopolitical euphemism) both China and Japan, which by most accounts remain by far the world’s second and third largest economies.

For Japan, robots could particularly cause electricity demand to surge, given that Japan may need to use a lot of them to replace its rapidly aging, high income labour force. Japan’s other alternative thus far has been to outsource labour to countries like China and Thailand, however it is not clear how much Japan is willing to continue becoming dependent on these countries, and meanwhile millions of Japan’s domestic workers are approaching retirement age.

A second way robots could help the coal industry is by causing electricity demand to rise overnight. One of the drawbacks of coal power has been that coal-fired power plants, unlike hydroelectric dams or, to a lesser extent, compared to natural gas plants, cannot easily ramp up and down their electricity production. This has meant that, like nuclear plants, they tend to over-produce electricity overnight, when the cost of producing the power is often higher than the price it sells for. However, since robots don’t sleep, they may drive up the demand for electricity at night. In addition to coal and nuclear, this may also help wind power, since it is often windier overnight than during the day. But it could hurt solar power.

Robots could perhaps also help allow coal-fired power plants to be moved to or built in sparsely populated areas where their local pollution will not be as bothersome, since robot-run factories may not need to employ many humans. This could also prevent new, long electricity lines from having to be built and maintained in some cases, as the power plant could be located right next to the robot-run industrial areas.

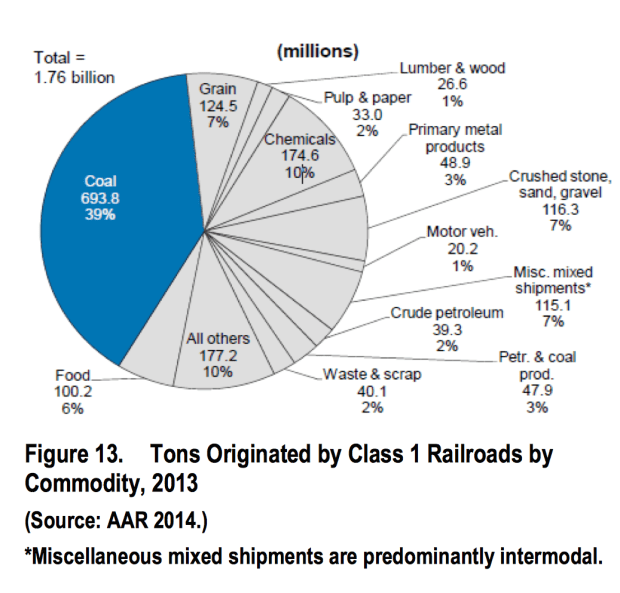

Robot-run factories and coal-fired power plants could also be constructed next to or near the coal mines themselves. This could be a big help to the industry, as coal has very high transportation costs because of how bulky coal is compared to other resources, for example oil, and because coal cannot be moved by pipeline. (Moreover, the transportation of coal often creates significant pollution next to the railways, roads, or barges it is being carried on).

Lignite, in fact, which is used commonly in Europe, has such a low bulk-to-value ratio that in most cases it transported only extremely short distances, and often by conveyer belt. A lot of sub-bituminous coal, which is very common in the US, is not much more dense in its energy content.

Given this bulkiness, coal could also benefit from robots that aid in the transportation sector: namely from self-driving trucks. Coal is often mined in mountainous areas, where building railways is difficult and expensive (railways cannot handle inclines or sharp bends easily, compared to roads). Building railroads to reach mines, or trucking the coal to the nearest railroad, can be an enormous expense. In the US and Canada coal mining also occurs in wintry and relatively remote locations, for example in northern Alberta or in the mountains of Montana and Wyoming, which can cause transport costs to be higher still.

With self-driving trucks, however, you do not need to pay a driver wages or insure a driver against the event of injury in a mountain-road accident, which saves money, and self-driving trucks can work all night, which improves efficiency. In fact, even large trucks are often too large to use on mountain roads and tunnels (or if there are mountain roads capable of handling them, they are often very expensive to build and maintain), but with self-driving trucks it is possible to use small trucks instead because you don’t have to worry about paying drivers’ wages or insurance. It would otherwise take a lot more drivers to transport coal via small trucks compared to large trucks, since small trucks can carry much less coal per trip.

Self-driving trucks could be a huge boon for the coal industry, then. Indeed, because many mining roads are privately owned by mining companies, they may be able to begin using self-driving trucks before normal roads do, since the biggest barrier to adopting self-driving trucks elsewhere may be public regulations.

Finally, robots and computer systems could help in the maintenance of long power lines, which could benefit the coal industry a great deal (and also benefit other industries, like wind power). Current methods of doing this are expensive, unwieldy, and often dangerous. This video may seem outdated, but many of the methods it shows are frequently still used today.

And of course, there may also be plenty of opportunities for robots to increase efficiency in the actual mining of coal itself.

4. Developing Economies

Many developing nations have embraced coal because it is cheap, but this process could slow or even reverse in the future. If it does, it could allow the US to pick up some of the coal slack that developing countries give up, since there is only so much carbon that the world can handle, and since in some cases it could lead manufacturing to relocate to the US. It could also cause the developing world to import more LNG or renewable energy sources from the US, pushing up the cost of those energies in the US when compared to coal.

First, as climate change fears rise, developing countries could begin to have to scale back on coal, whether because their own populations become worried (the developing world in general is more vulnerable to climate change than the developed world is) or because the developed world decides to slap carbon tariffs on their exports.

Second, local pollution in much of the developing world has become so intense that it may cause – and in some cases, is already causing – increasing pushback against coal.

Third, as was mentioned earlier in the article, robots could allow developed countries to “reverse outsource” their manufacturing industries, which would sharply reduce demand for energy in the developing world.

Fourth, if urbanization slows in the developing world – which it could, because of such “reverse outsourcing” taking away urban jobs, because of the spread of cell phone and Internet access into rural areas, because of urban air pollution becoming intense and undesirable, and because urban temperatures in developing countries are frequently extremely high compared to rural areas (particularly rural highlands) – then the developing world will demand energy sources that can be accessed in rural areas where there are little or no electricity grids: solar panels, diesel generators, small wind turbines, etcetera. But not coal, which is generally burned in big power plants to power cities and factories.

Instability in the developing world might also benefit the US coal industry, allowing the US to increase its coal exports. If, for example, China falls into regional chaos like it did for decades prior to the Communist takeover of the country in the late 1940s, then it could put at risk some or many of the energy supply routes that link China’s energy-rich interior provinces (like Shanxi, Heilongjiang, and the “autonomous regions” of Xinjiang and Inner Mongolia) to China’s major urban areas on the coast (like Shanghai, Guangzhou, Hong Kong, Beijing-Tianjin, Taipei in Taiwan, and many others).

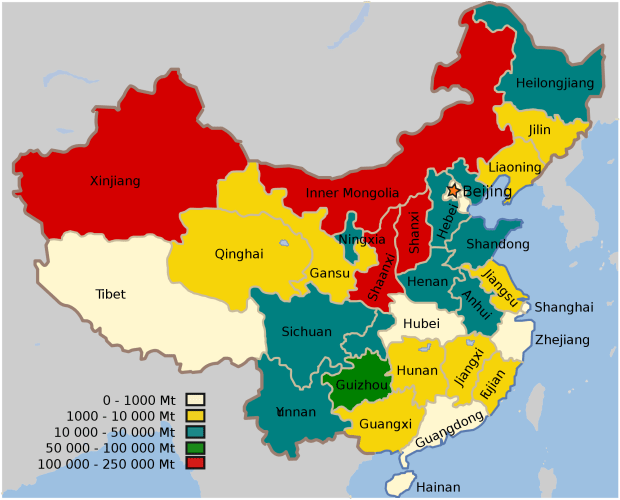

Shanxi and Inner Mongolia combined have accounted for more than 15 percent of global coal production in recent years. If China’s coastal cities cannot secure energy supplies from within China, they may turn to importing coal from countries like Australia and even the US instead. This may not be likely to happen, but it is a “black swan” possibility that is worth taking note of, given China’s historical regionalism and the enormous energy and coal consumption of China’s coastal provinces.

This is also true of other energy sources. China’s natural gas, hydro, and most of its oil production, for example, are also located in interior provinces like Heilongjiang, Xinjiang, Sichuan, and Yunnan. They are in fact often located extremely far in the interior, such as in the Autonomous Region of Xinjiang, which produces a substantial portion China’s oil, natural gas, and coal.

Xinjiang has a deep ethno-religious divide between Turkic Muslim Uyghers and its more recent Han Chinese settlers, and has very difficult terrain that has historically made it prone to separatism, irredentism (with the Turkic Muslim populations of neighbouring, now-independent Central Asia) and “warlordism”. In Xinjiang, mountains cover an area larger than England and regularly reach heights higher than the highest Rockies. Much of Xinjiang is also covered by deserts or semi-deserts, and the region is so far inland that its capital city, Uruqmi, “has earned a place in the Guinness Book of Records as the most remote city from any sea in the world. It is about 2,500 kilometres (1,600 mi) from the nearest coastline”.

China has, similarly, also pinned hydro hopes on Tibet; a risky proposition given its intensely difficult terrain, remoteness, ethno-religious resistance to Chinese settlement and domination, and position as the source of most of India’s, China’s, and Southeast Asia’s live-giving rivers.

China’s energy imports come mostly, however, from Siberia, Central Asia, or from Oceania, Africa, or most often the Middle East (by way of the Strait of Hormuz, the Indian Ocean, the Strait of Malacca, and South China Sea). Should these supply routes be imperilled, Chinese coastal cities could be forced to import energy across the Pacific from the Americas instead.

13 percent of China’s oil imports comes from Angola, even, according to the US Energy Information Agency, more than from any country apart from Saudi Arabia (16 percent). Angola, apart from being a formerly war-torn country that remains full of material poverty and ethnic division, is located very far away from China, on the Atlantic rather than Indian Ocean coast of the African continent. For its oil to reach China, it must first round the southern tip of Africa, passing waterways controlled by Angola’s regional rival South Africa.

—

It may also become more economical to have solar power harnessed in the developing world more than or instead of in the developed world. This is because in the developing world, peak energy may increasingly occur at the same time as peak sunlight: in order to power air conditioning for billions of people when its 30-50+ degrees Celsius outside. In the developed world, in contrast, air conditioners are already widespread, and in many places peak energy use occurs when the sun is not bright, for example to power heating units in the winter, or to power perennially overcast places like Britain or Seattle, or to keep the lights on during super-long winter evenings in Scandinavia, or perhaps eventually to power electric cars overnight.

The developing world may also be increasingly likely to use airplanes more often than the developed world does. This is an important point, as airplanes arguably contribute to climate change more than all the cars on the world’s roads combined (at least, over a five-year timespan), since they emit lots of greenhouse gasses at high altitudes. Developing countries may need to use airplanes more because much of the developing world is located in areas where land-based transport can be difficult: in mountainous or hilly areas, in deserts, in the Tropics, in archipelagos, in rural areas, in conflict-prone areas, and in densely populated cities with terrible traffic jams.

The developed world, on the other hand, may even replace its own airplane usage with land-based transport in some cases, as a result of the technological advances occurring within the land-based transportation sector. Instead of flying from New York City to Florida, Sydney to Melbourne, or even London to Barcelona, people may take the train or bus instead (making use of the wi-fi on the train or the bus along the way, as well as the ability to use services like Uber and Zipcar to get around once they have arrived at their destination) or eventually even take a self-driving vehicle.

5. War

During World War Two, inter-continental weapons did not exist, so US shores were safe from attack (with a few exceptions). During the Cold War inter-continental weapons did exist, but the US was saved from attack by its massive deterrent of nuclear and conventional weapons.

Today, however, precision “smart-bombs” and precision cyber-weapons exist, putting the US at risk (in theory, at least) of a surprise attack on its military and industrial infrastructure. Because a large-scale precision attack would cause very few deaths by WW2 or Cold War standards – a factory could in some cases be destroyed overnight and kill only the night watchman, while cyber-weapons can disable an entire electricity grid without killing anyone – it could mean that an enemy country could be more willing to take the risk of launching such an attack. In other words, the technological advances that are making war less deadly may also end up making war more likely to occur.

The Pentagon is undoubtedly going to spend hundreds of billions or even trillions of dollars to defend against and prepare for such a possibility. It has already done this in recent decades with its ballistic missile defence systems; however these might be inadequate on their own, as North America could simply be too big a place to protect in its entirety.

As the precision-weapons era matures throughout the militaries of the world, the Pentagon may decide to take the additional step of shielding US industry by clustering a few “mega-industrial areas”, capable of producing both military and essential non-military goods, that it can then build more impenetrable defence shields (including “cyber-shields”) around. The idea will be that it is far easier to defend an area the size of a city than it is to defend an area the size of a continent. Other militaries around the world may do a similar thing.

The question is, then, if these military-shielded mega-industrial areas do become a reality, will it be coal that powers them?

It seems quite plausible that it will be. The main alternative, natural gas, is difficult to transport by truck, and natural gas pipeline networks and gas production sites could be vulnerable in the event of war, as could be electricity grids. Coal, however, can be transported by truck, and much of the coal production in the US is already concentrated in just a single state in the heart of the country, Wyoming. Moreover, coal can be stockpiled in enormous quantities, whereas gas is very difficult to store in large quantities.

Oil could conceivably be used instead of coal, but the US has few oil-fired power plants, and oil would be needed in large quantities to power the many military vehicles and fleet of trucks the US would need to fight a war, so it would not necessarily be available to use for electricity production.

Other countries too might use coal if they decide to build military-defended mega-industrial areas. Many significant countries in the world have coal mines or coal reserves, yet do not produce natural gas or oil in as significant quantities. These include Germany, India, England, Turkey, Poland, and China, for example. Moreover, countries can build up huge stockpiles of imported coal, which they cannot do with natural gas.

A mega-industrial region of this kind, backed by the military, could perhaps also allow carbon capture and storage to finally become economically viable. Carbon capture and storage is a key component of mitigating global warming if fossil fuels are not going to be phased out, yet thus far it has been far from economical. But whereas it has not been achievable for a single power plant, if you cluster many power plants together in one area, it could maybe allow for the economy of scale necessary to make carbon capture more affordable.

If, finally, tensions between Russia and “the West” continue to deteriorate, or if the situation in Ukraine continues to destabilize, it might lead to European countries to have to turn to imports of energy from the Americas to make up for the natural gas and coal they would have to stop importing from Russia and Ukraine. This too could help to push up the price of US coal.

Conclusion

I am just playing devil’s advocate here, of course. I don’t actually have any idea what the future of the American or global coal industry will be. Still, judging by the fact that the Dow Jones US coal index has nearly tripled since the start of 2016 (though it still remains around 80 percent lower than it was as recently as mid-2014), I may not be the only one to be doing this.