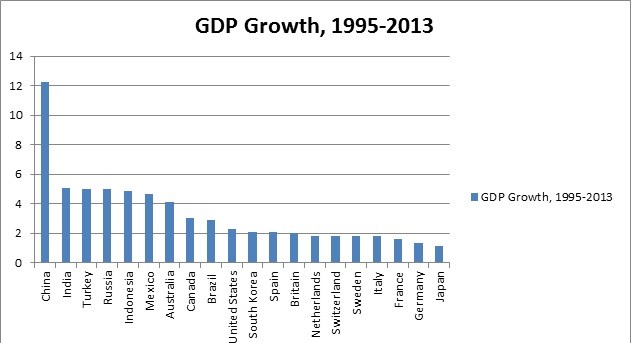

The graph below shows the world’s 20 largest economies, and how many times larger they are today than they were in 1995. As you can see, Japan grew the slowest of the countries on the list. Though it is still the world’s third largest economy, close to double the size of fourth-place Germany and more than half as large as second-place China, its economy is barely larger than it was in 1995. During that same span, China’s economy is believed to have grown more than twelve-fold.

How did this happen?

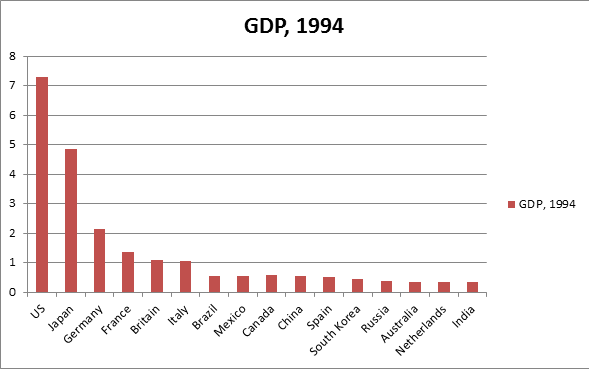

Japan was all over America’s radar in the early 1990’s. As you can see from the graph below, Japan’s gdp is thought to have been 66% as large as the US’s in 1994. By comparison, even China’s gdp today is only thought to be 52% of the US’s. At the same time, there were no other obvious candidates to attract American attention back in the 1990s; Germany was inwardly focused on reabsorbing East Germany, while China’s economy was only the 10th largest in the world and Russia was in its post-Cold War disarray.

Many Americans at the time worried that Japanese businesses were out-competing their own, and as a result called on their government to reduce some of the benefits that the United States had provided Japan during the Cold War. This attention was probably not the best thing for Japan; indeed, it may not be a complete coincidence that the Japanese stock and real estate markets collapsed during 1990, the year after the Berlin Wall came down.

The most famous “Japanophobic” film: Rising Sun (1993), starring Wesley Snipes and Sean Connery

Japan’s gdp per capita in 1995 was 1.4 times higher than the United States, the next richest major economy. It was 4 times that of neighbouring South Korea. Having such a nominally wealthy population may have made it difficult for Japan to compete with other developed countries, much less with developing ones.

Most of Japan’s baby boom generation reached the age of 50 in the late 1990’s, and began saving more for their eventual retirement. This meant that there was less private consumption to stimulate Japanese gdp. By comparison, the boomers in the US and Europe in 1995 were only in their mid-30’s, and in China they were in their mid-20’s. Japan’s second largest generation, meanwhile, was entering their mid-to-late 20’s during the 1990’s, meaning that Japan’s labour force was not growing at the same speed as it had through the 1980’s when this generation was graduating from high school and college.

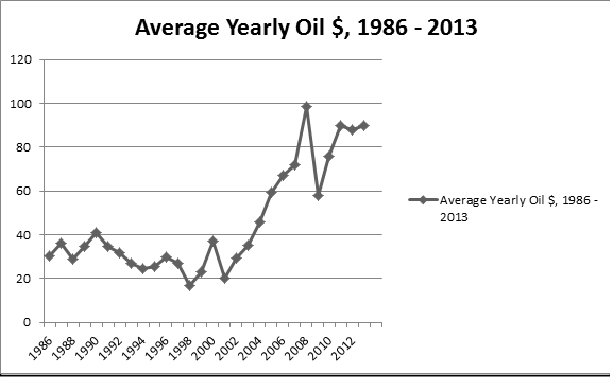

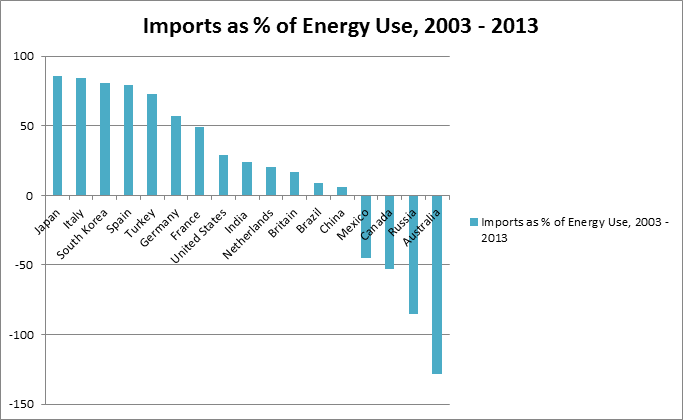

Between 1997 and 2007 the price of energy shot way up, reaching all-time monthly highs even when adjusted for inflation. Despite dipping somewhat during the recession in 2008, prices have stayed very high by historical standards during the past five years. Japan, though it uses its energy more efficiently than most countries, is also one of the most dependent upon imports for its energy consumption. As a result, the high prices of the past decade have helped limit its economy’s ability to grow.

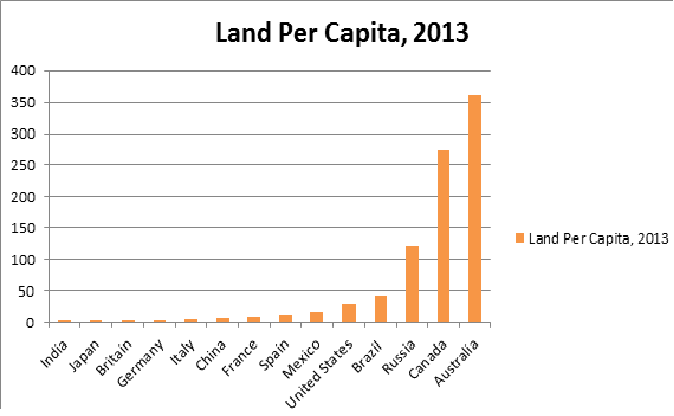

Japan is not only dependent on importing energy, but also most other natural resources. It is the world’s largest importer of tin, and the second largest importer of iron ore, copper, aluminum, nickel, silver, and coffee. Using land as a (admittedly limited) proxy for natural resource wealth, the graph below shows how Japan compares poorly with other major economies on a per capita basis.

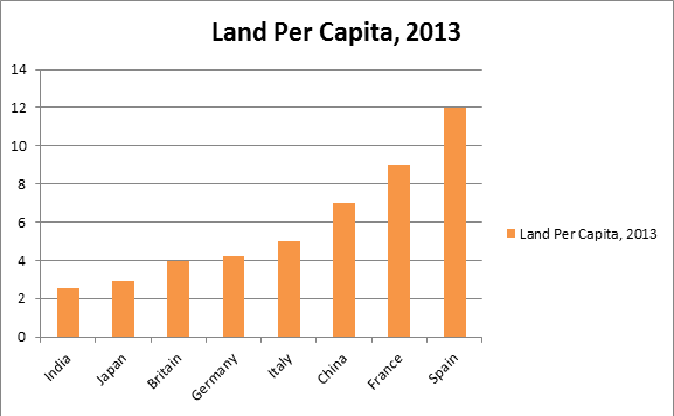

And zooming in on this graph:

Japan’s small amount of land and resources relative to the size of its population probably played a role in its poor economic performance in the past two decades, as this period saw global mineral and food prices rise rapidly.

Finally, Japan is one of the most equal countries in the world in terms of income distribution, and has one of the lowest unemployment rates. Arguably, Japan’s gdp grew less than it could have because the country was more focused on pursuing social welfare goals like employment and income equality.

What’s next for Japan?

Obviously, Japan is no longer attracting too much American attention: that honour now goes to China. Japan’s development costs may also no longer so much higher than those of other developed countries. Japan now has a per capita gdp that is around 87% as high as Germany’s and France’s, 74% as high as that of the United States’ and Canada’s, and just 59% as high as Australia’s.

However, Japan’s population is still the oldest in the world, and it is older than ever. Japan’s baby boomers are now 65 – 70 years old on average; given that the average effective age of retirement in Japan is 69, they may soon retire en masse. Meanwhile, the second largest generation in Japan today is 40 – 45 years old on average, meaning that their levels of consumption may decline as they enter their 50’s and 60’s over the next fifteen years. It is perhaps worth mentioning here that not only did Japan’s financial crash in the early 1990’s occurred when its baby boomers were approaching age 50, but that the US and Europe’s crises of 2007-2008 occurred as American and European baby boomers were approaching age 50.

Fortunately, Japan does have the highest NIIP in the world. (NIIP = Net International Investment Position; which is basically the amount of money a country’s government, businesses, and people are owed after you take into account the amount of money they owe to other countries). In fact, as recently as 2010, Japan’s NIIP was roughly that of China and Germany, the world’s next two largest creditors, combined. Japan also has the highest life expectancy of any country in the world, at 84.6 years – compared, for example, to 80 for the US. And Japan is also frequently listed as having the highest standard of life among major economies, if such ratings are to be believed.

That being said, Japan’s population is aging so rapidly that it is not clear whether either of these things will be sufficient to allow it to remain economically competitive in the years ahead. In addition, the huge amount of money that Japan is owed by other countries can only be used if those countries are able to pay it back; something that does not always happen so easily, as Germany has learnt in recent years. To be fair, much of the money owed to Japan is invested in the United States, which is unlikely to turn into Greece anytime soon. Still, you can never be too sure.

Japan also continues to be highly dependent on imports for its energy consumption, particularly since the tsunami-induced nuclear meltdown it experienced in 2011. 95 percent of Japanese energy comes from imported fuels, compared to only 15 percent for the US and 10 percent for China. Japanese electricity prices are more than double those of the United States, and higher than all major European countries apart from Germany. This could make it relatively difficult for Japan to use machines to help supplement its aging workforce.

One obvious way to deal with an aging population is through immigration. This is not, however, something that Japan is accustomed to doing. Japan has one of the smallest foreign-born populations in the developed world. Moreover, unlike English, Spanish, Portuguese, and French, there are no large and poor populations in the world who speak Japanese that Japan can recruit. The Japanese diaspora is only about 2.5 million strong, 1.2 million of which live in the US and probably aren’t looking to move to Japan, and 1.5 million of which live in Brazil, which is about as a far away from Japan as you can get. Some countries, like Sweden, Denmark, and the Netherlands, deal with a similar problem by using English to speak to some of their immigrants. However, Japan is also the worst at speaking English among nearly all developed countries in the world. Plus, Japan’s population density is also still extremely high, so the country may have an especially difficult time growing its population further through immigration.

Of course, none of this means that Japan will definitely not open its doors to mass immigration – it has a high standard of living to attract prospective immigrants, and it has historically proven that it can undergo dramatic cultural and economic changes in a very short period of time. That being said, Japan will probably find it many times harder to solve its demographic problems through immigration than, for example, Canada will when it eventually faces the same kind of rapid aging that Japan is on the verge of.

If immigration and automation cannot get the job done in the short time frame Japan faces before its population reaches old age, this might only leave outsourcing as a solution to its demographic problems. There are 1.3 billion Chinese people living within a relatively short distance of Japan that it could potentially outsource to. However, Japan is unlikely to rely on China for too much of its outsourcing needs, for five reasons.

First, Japan is unlikely to decide to become too dependent on China given that it knows China might become powerful enough to dominate it at some point in the future.Second, China still resents Japan for its brutal occupation of much of its territory during the 1930’s and 1940’s. Third, Japan is already extremely dependent on China; 26% of Japanese imports came from China in 2013, compared to only 11% from Japan’s next largest trade partner, the United States. No country wants to be too dependent on any other single country, so Japan will not want its dependence on China to increase much more than it already is.

Fourth, Japan does not want to be too dependent on China because the Chinese economy is potentially unstable, having become accustomed to rapid growth that may now be unsustainable. Finally, Japan will not outsource too much to China because Chinese labour is no longer so cheap to employ. China’s average income is now $6000, and in coastal provinces that Japan can access most easily it averages around $10,000. By comparison, average incomes in nearby Vietnam are only $1700, Cambodia $950, Indonesia $3600, the Philippines $2600, North Korea $1200, India $1500, and Bangladesh and Burma $900.

Thus, Japan will probably look to Southeast Asia or even India for most of its future outsourcing needs. This could help it to overcome its demographic challenges, while also serving as a boon for the poor countries receiving Japanese investment. However, it will also mean that Japan will have to be increasingly active in regional affairs, driving hard bargains when it comes to crafting economic agreements with the countries and businesses it outsources to. In addition, Japan will continue to rely heavily on Southeast Asia, the Middle East, and/or Pacific Russia for its energy and mineral needs for at least the foreseeable future. As a result, Japan could once again become an extremely active player throughout much of Asia, looking to gain access to both cheap labour and natural resources.

How might this affect its relations with other regional powers, particularly China and the United States but also South Korea, Australia, Thailand, Indonesia, India, Taiwan, and Russia? Will Japan be able to maintain healthy relationships with all of these states, or will it be tempted to move closer to some and further away from others? And can Japan’s economy come through its demographic changes intact, perhaps even serving as a model for other Western countries whose own Boomers will reach their seventies during the 2020s and 2030s? We will find out soon enough.