It is easy to be small and ignored. But to be large and ignored, it helps to hide within the shadow of an even larger entity. In the realms of economics and geopolitics, there are three very large countries which, though not actually ignored, do not always receive the respect their size demands, as they inhabit the shadows thrown by the world’s colossi, the USA and China. These countries are Canada, Mexico, and Japan.

Japan has by far the third largest economy in the world, by far the second largest developed economy in the world, by far the second largest population among developed economies, and the tenth largest population globally.

Canada is the second largest country in the world, the fourth largest possessor of renewable freshwater, the fourth largest producer of renewable energy, the fourth largest exporter of oil, and the tenth largest economy.

And Mexico has the world’s eleventh largest population, thirteenth largest territory, and fifteenth largest economy. (Only five other nations are top-15 in all three categories: the US and the BRICs). Mexico has 2.5 times the population of the next largest Spanish nation (Colombia), plus a diaspora of 35-45 million in the US. It is also the twelfth largest oil producer in the world. The Greater Mexico Region (including Mexico, Texas, California, Venezuela, and US waters in the Gulf) produces more oil than Saudi Arabia or Russia. This region also has an economy larger than any country in the world, apart from the US or China.

The League of the Overshadowed

At the moment, however, trade between Canada, Mexico, and Japan is quite small. Neither Canada nor Mexico are even among Japan’s top fifteen trade partners. And while Mexico and Canada do trade with one another more often — Mexico recently overtook Britain to become Canada’s third biggest trade partner — trade with Mexico still counts for less than three percent of Canada’s total. Their trade with one another is overshadowed by that of the US. Indeed, California alone trades far more with Canada, Mexico, and Japan than those countries do with one another. There is no League of the Overshadowed… yet.

It may be worth noting, though, that US politics have to a certain extent put trade with Canada, Mexico, and Japan into question. President Trump’s first executive order was to withdraw from the Trans-Pacific Trade Partnership, in which Japan would have accounted for over 60 percent of the twelve member-states’ GDP apart from the US. Trump has also signalled his intention to renegotiate NAFTA, tighten the US-Mexico border, raise tariffs on Canadian farm and forestry products, and keep American fossil fuels cheap.

If these policies are followed through on, they could have the effect of driving US trade partners somewhat closer together. Obviously, Canada and Mexico have an interest in showing that they can trade with one another regardless of what Washington intends to say or do about NAFTA. Both also have an interest in exporting more fossil fuels to Asia, where prices remain more expensive than in the shale-rich US. On June 1, in fact, Canadian senator Paul Massicotte wrote an op-ed calling for Canada and Japan to sign a free trade agreement with one another as quickly as possible, given the failure of TPP and risks for NAFTA. Especially as both Canada and Japan have large majority governments right now, such a deal may happen.

An economic relationship between Canada, Mexico, and Japan could turn out to be far more significant, however, than being just a knee-jerk response to Trump’s America-First politics. As we will see, Canada, Mexico, and Japan are in fact complimentary nations, both economically and geographically. Already they have a propensity to trade with one another that is larger than their absolute trade levels suggest (see graph below). So long as Japan’s economic growth remains stagnant, Mexico remains poor, and Canada remains underpopulated, this propensity does not matter much. But if these conditions do not remain, we should expect trade between these three significant, overshadowed countries to grow by a very large amount.

Complimentary Nations

Economists often talk about land, labour, and capital, considering them fundamental inputs of productivity. In the case of Canada, Mexico, and Japan, these inputs are epitomized: Canada has land but not labour, Mexico labour but not capital, and Japan capital but not land. Together, then, they could make a formidable team.

In Canadian politics and business, it has become common in recent years to say that by exporting natural resources to China, Canada can finally reduce the near-monopoly that the US has on buying Canadian exports. This view, however, is based on a false extrapolation of a trend that is now nearing its end: industrial growth in coastal Chinese cities. As China now seeks to rebalance its economy, by investing instead in its service sectors (which are less resource-intensive) and interior cities (which have a lower propensity to engage in trans-Pacific trade), its demand for Canadian resources is unlikely to continue to surge. Most of the resources it does buy will probably continue to come from within its own borders — China only imports 15 percent of the energy it consumes — or from its “One Belt, One Road” partners in Asia.

In Japan, on the other hand, the reverse is true. Japan has few resources of its own, and no Silk Roads to tap. Japan imports 90-plus percent of the energy it consumes, mainly from the Middle East. Its access to the Middle East, however, is imperilled, both from competition with other Asian countries (notably, China and India) as well as from Middle Eastern conflicts. Consider, for example, that Japan accounts for 30-40 percent of LNG imports globally, yet its primary supplier, Qatar, is now in an open feud with Saudi Arabia. Between competition and conflict, Japan could have to rely more on trans-Pacific trade to get resources. It would not be the first time: in the 1930s, eighty percent of the oil Japan consumed was imported from the US.

Even more important may be the impact of labour-saving machinery — robotics — upon Japanese trade. Because Japan has the oldest population in the world by far, it is planning to become a leader in robotics. Even, for example, as soon as the Tokyo Olympics in 2020, Japan is planning to showcase its robotic prowess. Yet robots are highly energy-intensive, and industrial robots resource-intensive. If Japan really does become the leader in robotics, it is likely to start importing lots of energy and other commodities from resource-rich countries like Canada. It may also be likely to start exporting its robotic technologies to countries like Canada, given Canada’s abundance of resources but lack of a large, cheap, human labour force.

Upstairs, Downstairs

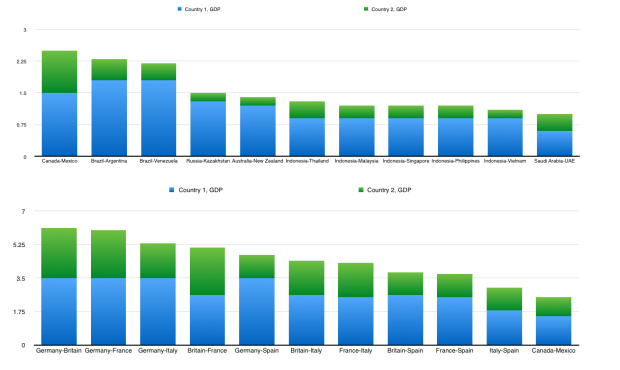

Today, if you exclude the US or Europe, Canada and Mexico have the largest combined economies of any pair of countries which are part of the same trade bloc (see graph 1 below). Yet if you include Europe, Canada and Mexico still rank quite a bit lower than a number of pairings of Europe’s largest economies (graph 2).

In other ways, however, Canada and Mexico rank ahead of these European pairings. In population they do so (graph 3). In land they do so too (indeed, Mexico alone is larger than any four countries in the EU combined). And in terms of their indirect, second-degree trade (their combined trade with a third country), Canada and Mexico as a pair lead the world (graph 4), a result of their both trading hugely with the US.

While Canada’s propensity to trade with Mexico is greater than with any significant country apart from the US, it is still only around half as high as its propensity to trade with the US. The reason for this is simple: Canada and Mexico do not share a border with one another. They are not even very close in proximity to one another. More than 3000 kilometres separate Mexico City from any of the largest cities in Canada.

This separation is also reflected in Canada’s lack of a significant Spanish-speaking diaspora, particularly relative to that of the US. In spite of the fact that 21 percent of Canada’s population is foreign-born, compared to just 14 percent in the US, only 0.3 percent of Canada’s population is Mexican, compared to an estimated 11 percent of the population in the US. Even the state with the smallest share of its population being Mexican or Mexican-American—Maine—has a higher share, 0.4 percent, than Canada does.

But this may be likely to change, for two reasons. First, there is a political faction in the US which is wary of further Hispanic immigration, seeing it as a threat to the singular position held by the English language in America. Second, whereas the population of the US is relatively young, the population of Canada is Boomer-dominated, inching towards old age. This is especially true of the population of Canada’s French-speaking provinces, Quebec and (partially) New Brunswick. These provinces also, because of the far smaller language gap between French and Spanish than between Spanish and English, have a much higher propensity to attract Latin Americans than do other parts of Canada (see graph). Between demographics of this kind and US immigration politics, the next major wave of Latin American emigrants could be to Canada.

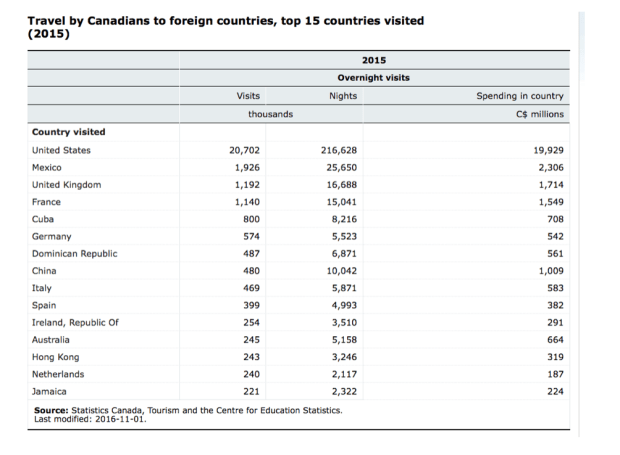

The aging population of Canada’s Baby Boomers, and especially of Quebec’s Baby Boomers, also indicates another area in which Canada-Mexico economic ties—both direct and indirect—are likely to grow: tourism. Already today, Mexico is the largest destination for Canadian travellers apart from the US, while the areas of the US that Canadians spend the most time in — Florida, the Southwest, and New York — are ones in which Mexican-Americans (or in Florida’s case, Hispanic-Americans in general) inhabit in large numbers. As Canadian Baby Boomers reach old age or retire, they are likely to spend more time in places like Mexico, in order to avoid much of the discomfort (even danger) of dark, icy Canadian winters. This will be most true of Quebec, given its older population, colder winters, and greater ability to learn Spanish.

As the chart above implies, the US reconciliation with Cuba may also lead Canadians to spend more time in Mexico. During the past generation, the US rivalry with Cuba has given Canadians a near lock on the Cuban market. Canadians account for an estimated forty percent of all visitors to Cuba, and Cuba accounts for a disproportionately large destination (given Cuba’s relatively small size) for Canadian tourists. As the US allows its own population to go to Cuba, however, Canadian snowbirds will lose the advantage of having such a cheap, warm country all to itself. Many will re-route to other Latin American beaches.

An even more important pull factor for Canadian snowbirds will be “e-commuting”. The ability for young Canadians to spend time in a cheap, warm country in the winter is likely to increase dramatically as a result of the modern Internet. This is also likely to impact the Baby Boomers. If, for example, it becomes easier for a Boomer’s children and grandchildren to come visit them in Florida or Mexico for, say, a whole month over Christmas, rather than for just a week, then Boomers will be likelier to go in the first place.

And the relationship may not even remain one-way only: Mexicans may begin to visit Canada more often too. Today Mexicans do not go to Canada much, because they lack the disposable income to do so. If and as Mexicans become wealthier, however, they may look to Canada as a place to go in the summer; a place where the summer weather is not too hot, the major metropolises are not too crowded, and a cottage by a northern lake may be rented at an affordable rate. Climate change could, sadly, also play a role in this equation. Mexico — and the Southwestern US, in which tens of millions of Mexican-Americans live — is dangerously arid, whereas Canada is in possession of an abundance of renewable, surface-level freshwater.

Conclusion—The New Drivers of Trade

Today, the main driver of trade is proximity. Countries which share borders with one another tend to trade a lot — though, of course, there are many exceptions to this — whereas far-away countries tend not to. However as (or, admittedly, if) globalization continues, proximity may no longer matter as much. Complimentarity may matter a lot more. We have seen here various ways in which Canada, Mexico, and Japan may be complimentary to one another. Canada has land but not labour, Mexico labour but not capital, Japan capital but not land. Canada has cold, dark winters but warm, water-rich summers, Mexico warm bright winters but hot, arid summers. All three countries have coasts on the North Pacific Ocean; none are part of the Asian (or Eurasian, or Afro-Eurasian) continent. And all three countries are very large, yet are overshadowed by neighbours that are far larger than they are. They may end up, if only informally, a formidable League.