This article was written for an essay contest, so the style is a little bit different from others on this site. It was first written three years ago, when most people had not yet become bearish on the Chinese economy and politicians in the US were still talking a lot about America’s “pivot to Asia”. The essay discusses the possibility that the Atlantic regions – North America, South America, Europe, and much of Africa – will remain at the heart of the international system in the years and decades to come, for better or for worse.

Hope you like it!

The Return of the Atlantic

For nearly 500 years, the Atlantic Ocean was the unrivalled centre of the international system, connecting Europe to its expansive economic and imperial networks in Africa, Asia and the Americas. Transatlantic trade continued to exceed transpacific trade as recently as the late 1980s, while at the same time the transatlantic alliance against the Soviet Union remained the world’s most important geopolitical partnership. Indeed it seems incredible to recall now, but China, India, Indonesia, Korea, and Australia combined had a smaller economic output than West Germany in 1990.

Today, in contrast, the European Union and United States both import more goods from China alone than they do from one another, and the Cold War has been over for a quarter of a century. The Pacific has in many ways become the new centre of the world: it is home to the three largest economies of America, China, and Japan, is the highway for East Asian imports of commodities and exports of manufactured goods, and acts as a base for nearly 75 percent of US soldiers stationed outside of North America or Afghanistan. Not surprisingly, a majority of economists, politicians, and journalists believe that the continued economic growth of populous Asian countries like China, India, and Indonesia means that the centrality of the Pacific has only just begun.

In this essay we will argue that, even as it remains popular to herald the arrival of a “Pacific Century” (to quote a famous Hillary Clinton op-ed in Foreign Policy magazine), it will actually be the Atlantic that will become once again the centre of the international system, serving as the corridor of an expanding economic network that will incorporate Europe, the Americas, much of Africa, and to a lesser extent even parts of southern Asia. Transatlantic commerce is likely to once again exceed the value of transpacific commerce and, partly by doing so, it will help to serve as an organizing force in global geopolitics. We hope it will serve as a force for good in the world as well.

To be sure, while we view this Atlantic phenomenon as likely to be brought about by economic, cultural, and linguistic circumstances that are already actively or latently in place, we will also argue that, from a policy perspective, the political effectiveness and ethical utility of such a reinvigorated transatlantic relationship will depend on the extent to which efforts are made to reduce carbon emissions in developed economies, as well as on the extent to which efforts are made to provide honest and constructive assistance to struggling countries within the developing world.

The Pacific Moment

The rise of transpacific trade during the latter half of the 20th century occurred as a result of a unique set of circumstances. These were, specifically, the reconstruction of the Japanese economy following its destruction in the Second World War, the emergence of South Korea and Taiwan following their adoption by the United States as strategically-located allies in 1950, and the rapid growth of coastal Chinese states following their devastation during the Sino-Japanese War, Chinese Civil War, and isolationist era under Mao, which occurred in an overlapping succession from 1927 until 1979. These four countries have caused transpacific commerce to soar in recent decades, with help from Southeast Asian success stories like Singapore, Thailand, and Malaysia.

While this rising transpacific trade has certainly deserved the widespread public attention it has received, it has nevertheless served to overshadow a number of other key characteristics of the global economy, which instead highlight the enduring significance of the Atlantic Ocean. These include the fact that roughly 65 percent of both the world’s nominal economic output and private consumer spending are located in the Atlantic basin rather than in the Pacific basin; that more than 70 percent of the populations of North America, South America, and Sub-Saharan Africa live within the Atlantic basin rather than the Pacific basin; that the Pacific generally takes 2-4 times longer to cross widthwise by ship than the Atlantic does; that the quantity of transatlantic investment is estimated to be 5-10 times greater than transpacific investment; and that Indian and Pakistani trade and labour crosses the Atlantic, Mediterranean, or Arabian Sea far more often they do the Pacific.

The reemergence of transatlantic interactivity as a defining feature of the international system will simply reflect these enduring realities. In addition, it will be driven by a set of economic evolutions that are beginning to revive transatlantic trade relative to transpacific trade, as well as by the continued spread of modern communications and the emergence of African and Latin American economies, which are helping to increase the political and economic significance of the cultural, social, and linguistic affiliations that bind together the four continents of the Atlantic world.

Transatlantic Connections

Atlantic regions share a number of important connections with one another. The first is cultural: unlike in Asia, the overwhelming majority of people in the Americas are of European or African heritage. Most have ancestors that arrived within just the past century or two. This could have increasingly powerful political and economic consequences in the future, particularly as the economies of Africa develop and as African populations in the Americas become wealthier and more empowered (most notably the 40 million US African-Americans, 28 million Afro- Caribbeans, 15 million Afro-Brazilians, and 80 million Brazilians who identify as being of mixed ancestry), such that it will no longer just be white Americans and Europeans engaged in the most significant transatlantic partnerships.

The second transatlantic connection is a social one, the result of technology increasingly allowing first-, second-, and even third-generation immigrants in the developed world to maintain relationships with family members, friends, and acquaintances back in their countries of origin. Crucially, immigrants in North America and Europe come overwhelmingly from Latin America, Sub-Saharan Africa, or the Mediterranean basin. More than half of the foreign-born population in the United States arrived from Latin America alone, and there are about four times as many first-generation immigrants in the European Union from Africa or the Americas as there are from East Asia.

There are, in fact, already 2-3 million Latino-Americans living in Spain, and more than 50 million living in the United States. Africa’s emigration rate to both Europe and North America, meanwhile, has risen at a faster pace than that of any other region since 1980, and is likely to continue to do so as a result of the fact that the average birth rate in Sub-Saharan Africa is nearly twice as high, and the per capita income nearly twice as low, as that of any other part of the world.

Finally, and in our opinion most importantly, there are the transatlantic linguistic connections. Over 80 percent of the world’s nearly 1.5 billion native speakers of Spanish, English, French, Portuguese, or Arabic live within the Atlantic or Mediterranean basins; each of these languages is fairly prominent within at least three separate continents. English, moreover, is far more widespread in mainland Europe than it is in any other continent apart from North America (or Australia). Switzerland, Germany, Austria, Scandinavia, the Netherlands, and Belgium are particularly proficient; according to some estimates, 60-90 percent of their populations are able to speak English In France, Italy, and Poland, meanwhile, the share of English speakers is estimated at 30-40 percent, which is still far ahead of countries like China, Japan, Indonesia, and even India.

In Africa, European languages are also spoken more widely than in most other areas of the world. This is partially the result of to the continent’s colonial histories, many of which ended as recently as the 1960’s or 1970’s. It is, however, also the result of Sub-Saharan countries tending to be linguistically diverse, such that their use of European languages as lingua franca remains common practice. Indeed, despite having the world’s lowest density of accessible schools, televisions, computers, and satellite dishes, English is already spoken by a greater number of people in Africa than in more populous India, both as a native language and as a secondary one.

French, meanwhile, is used by an estimated 90 million Africans, Portuguese by an estimated 20 million Africans, and Arabic as far south as the Sahel.24 In South Africa approximately 20 million people understand Afrikaans, a language that is for the most part mutually intelligible with Dutch. Over 85 percent of Africa’s English-speaking population and nearly all of Africa’s French-, Portuguese-, Arabic-, and Afrikaans-speaking populations live within the Atlantic or Mediterranean basins.

Also important is that over 40 percent of Africa’s population is under the age of fifteen. This makes it the world’s youngest region by a considerable margin: by comparison, only 15 percent of China’s population and 29 percent of India’s population are younger than fifteen. Children possess the ability to learn languages many times more easily than adults can, particularly if they have access to schooling, books, media, and modern communications.

Africa’s current generation of children might become the first to grow up with widespread access to such tools, which might therefore help African economies to develop and integrate with the other continents of the Atlantic world. This is also one reason why it would be wise from a policy standpoint for Europe and North America to immediately support economic development in Africa, since doing so would help African populations gain access to more education and information now while they are still young.

Shifting Trade Patterns

In 2013, Chinese coastal cities had an average nominal per capita income of roughly $20,000, nearly as high as those of South Korea and Taiwan. The median age in China is 37, about the same as in the US; in South Korea and Taiwan the median age is 40. These are no longer really “emerging markets”, in other words. Rather than experience another lengthy period of rapid economic growth that would continue to drive up transpacific trade, they will instead be undergoing various structural evolutions, as all maturing economies tend to do over time.

In the coastal areas of China, this evolution is likely to be from an economy oriented around exports of lower-end manufactured goods to an economy that exports value-added goods and services and is more reliant on the private consumption of its own population. Such shifts are natural for a middle-income economy like China to experience, but they may also reduce the quantity of China’s transpacific imports of industrial commodities and transpacific exports of manufactured goods.

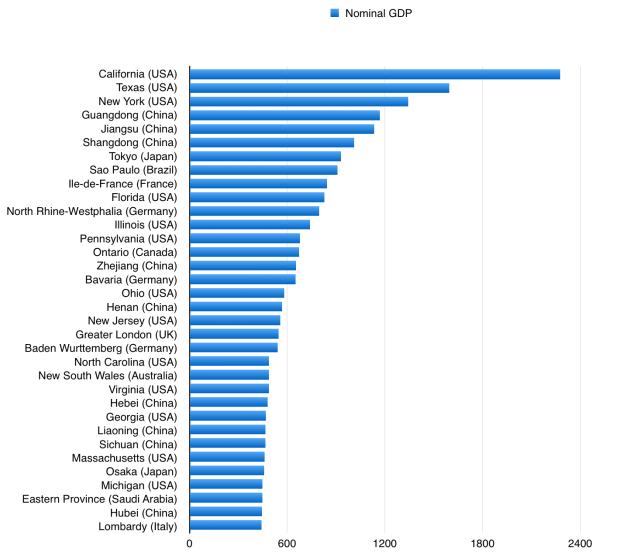

Economic growth in the poorer interior provinces of China, meanwhile, or in the even poorer Indian subcontinent, is not certain to bring about the continued rise of transpacific commerce either. The emerging provinces of the populous Chinese interior are likely to trade mainly with coastal Chinese provinces and other countries in Asia, rather than with economies overseas. Today, for instance, in Sichuan and Henan, the two largest inland Chinese provinces, exports account for around just 4 percent of provincial economic output, almost nothing compared to the 47 percent of economic output that exports account for in coastal China’s two largest provinces, Guangdong and Jiangsu.

In addition, given the crowdedness of China’s coastal cities and ports, the interior provinces of China may also increasingly avoid using the Pacific in favour of the more direct “Silk Road” routes to Europe, or in favour of using Myanmar’s commercially navigable Irrawaddy River to directly access the Indian Ocean.The economic emergence of the Indian subcontinent, meanwhile, could perhaps lead transatlantic commerce to rise faster than transpacific trade, as India and its neighbours may partially succeed China in supplying cheap goods or services to consumers in the Atlantic world.

As they emerge, the Indian subcontinent and the Chinese interior will also be importing rapidly growing quantities of oil and gas from the the Persian Gulf, Central Asia, and Russia. Indeed, India and Pakistan already receive roughly 75 percent of their oil and gas imports and an astonishing 30 percent of their imports of goods in general from the Persian Gulf. China’s interior provinces, meanwhile, get around 75 percent of their gas imports from Turkmenistan and Uzbekistan and 30 percent of their oil imports from Russia and Kazakhstan. These imports are likely to increase, not only because of India’s and China’s continued growth, but also because of their shared desire to consume less coal, on which they rely for an average of about 65 percent of their energy consumption.

This need to import large quantities of energy could lead to competition, rather than cooperation, between regional powers like China, India, and Japan, potentially undermining Asia’s ability to cooperate as a more coherent political unit. (In contrast, the Atlantic world consists mainly of synergistic relationships where energy is concerned: Europe is a net energy importer, South America and Africa are net energy exporters, and North America is not too far from reaching the “energy independence” it has long dreamed about). Moreover, because the European Union itself currently receives around 60 percent of its oil and gas imports from Russia, the Persian Gulf, or Central Asia, the increasing energy consumption of Asia may force Europe to begin importing much more energy from the Americas or western Africa instead, further boosting transatlantic trade.

Conclusion: Policy Framework

While the renewed significance of the Atlantic is likely to occur mainly as a result of the commercial, cultural, social, and linguistic factors discussed above, we believe that specific policy goals are nevertheless required to ensure that such a renewal occurs in a manner that is both ethical and politically effective on a global level. Two policies in particular may be advisable in this regard:

One is the implementation of per capita carbon emissions taxes. Such taxes would likely facilitate transatlantic commerce through the export of European energy-saving and clean energy production technologies to the emissions-intensive markets of North America, whilst simultaneously providing both Europe and America with a more responsible and defensible platform in climate treaty negotiations with industrialized Asian economies that have much lower per capita and historical emissions levels.

The other is increasing political outreach and economic assistance to struggling countries, particularly those within Africa. Africa contains many of the world’s greatest challenges if it is not constructively engaged with, and it also has a youthful and diverse population of more than a billion people, vast reserves of natural resources, and linguistic and social connections with Europe and the Americas. All of these qualities make it a necessary component of any revitalized transatlantic project.

Of course, each of these policies deserves much more focus than we have left to spare in this essay. Yet still we feel confident in saying that, if these two policies are diligently and honestly pursued, then the unexpected return of the Atlantic as the central corridor of the international system would not only become more likely to occur, but will also be much more welcome when it does.