The Birthplaces of China’s Leadership

Internal Chinese Geopolitics, part 1

The Geopolitics of Chinese M&A

North Korea and the Olympics Curse

With the new year starting, it is now forty years since 1979. Forty of course is a biblical number, which is fitting because 1979 was a year in which religious belief became decisively political. Some of these events are still well remembered – Iran’s Islamic Revolution, the Soviet invasion of Afghanistan on Christmas Eve, the Camp David Accords between Jimmy Carter, Anwar Sadat, and Menachem Begin. Other key events however are often forgotten, so that 1979 does not usually get the acknowledgment it deserves as being a year of unmatched religious and political action.

The year began with the full resumption of diplomatic relations between the US and China, on New Year’s Day, ending three decades of formal estrangement between the two countries. This was followed by Deng Xiaoping visiting the White House at the end of the month, the first time a Communist leader of China had ever made such a trip.

This new relationship had an immediate political impact when, on January 7th, the Khmer Rouge regime in Cambodia fell to the invading Communist Vietnamese. Five weeks after that, China invaded Vietnam, launching a short but brutal war against Vietnamese forces that had been fighting the US only six years earlier.

While the political importance of China and America re-establishing their alliance is obvious, its religious significance tends to be overlooked. It has, however, helped lead to one of the largest increases in any religion in recent history: the adoption of Christianity by many tens of millions of Chinese since the 1970s. In 1979 China’s Three-Self Patriotic Movement church was legalized by the Chinese government. It and many other much smaller churches have been so successful in the decades since that today China and America have probably the two largest Protestant populations in the world. China’s overall Christian population is difficult to estimate, but 100 million is a common guess.

Of course, it was in the Middle East where the biggest religious and political upheaval in 1979 took place. In Iran, the Ayatollah came to power on February 11th, the Shah having fled to Egypt three weeks earlier. In a foreshadowing of events that would come at the end of the year, on February 14ththe US ambassador was kidnapped and killed in Kabul, while on the same day Iranian militants temporarily took control of the US embassy in Tehran, kidnapping a Marine there.

But what goes down also goes up. On March 26, the Egypt-Israel Peace Treaty was signed. This was an event of great significance, considering that the two countries had fought four wars against one another in the preceding three decades, yet have not fought a single war against one another in the four decades since. Israel returned the Sinai Desert to Egypt as part of the deal, while Egypt became the first Arab state to recognize Israel.

The month ended on a less peaceful note in a different arena of religious and political conflict: Britain. On March 30 Airey Neave, the Tory party’s Shadow Secretary of State for Northern Ireland, was assassinated outside of the British Parliament by a car bomb planted by Irish militants. The assassination took place just two days after a no confidence vote had brought down a Labour government; Margaret Thatcher was elected Britain’s first female PM a month later.

This assassination would be followed by an even larger attack later in the year. On August 27[1], the Provisional Irish Republican Army killed eighteen British soldiers with two roadside bombs in Northern Ireland, while on the same day killing Lord Mountbatten (an uncle of Prince Phillip, who had formerly been head of the Royal Navy, head of the Armed Forces, and Viceroy of India), his grandson, and two others by planting a bomb on his boat[2].

A month later, Ireland would host its own biggest religious event in decades, when the Pope visited the island. The Pope was welcomed by a crowd estimated to include 2.7 million people, nearly the entire population of the Republic of Ireland[3].

This however was not the Pope’s most important trip abroad in 1979, nor the one to attract the largest crowds. John Paul II, who had only become Pope at the end of 1978, was the first non-Italian Pope in 450 years. He was, even more importantly, Polish, at a time when Poland was the largest country in the Soviet-led Warsaw Pact. The Pope’s visit to Poland in June of 1979, often referred to as the nine days that changed the world, was the first trip by a Pope to a Communist country. It played a substantial role in the rise of the Polish Solidarity movement, and so in turn arguably helped end the Cold War.

The Pope’s influence also attracted enemies. When, at the end of 1979, the Pope was visiting Turkey, a man named Mehmet Ali Agca, who was then beginning a life sentence in prison for killing the editor of a Turkish newspaper earlier that year, escaped from jail and fled to Bulgaria. Two years later, Agca would shoot the Pope in St. Peter’s Square. Given Bulgaria’s position in the Warsaw Pact, many people speculate that the Soviet Union was behind this attack in some way[4].

Acga would later claim that a reason for the shooting was that the Pope had orchestrated the siege of the Grand Mosque of Mecca, a siege which was taking place when Acga made his jail break in November of 1979. This siege, which lasted for two weeks at the holiest site in Islam, involved tens of thousands of hostages[5], several hundred gunmen, and one false messiah. It took place on the first day of the new millennium of the Islamic calendar (1400 A.H.), during the annual Hajj pilgrimage. Saudi forces finally ended the siege after a number of failed attempts and hundreds of deaths, by secretly enlisting the help of France, which sent three of its Special Forces soldiers to Mecca. They quickly converted to Islam in order to enter the holy city, then used gas to sedate the gunmen, who by then had taken refuge in the catacombs beneath the Mosque.

The siege arguably had a major impact on Saudi culture and foreign policy, and a direct legacy in future events such as the emergence of Al Qaeda. It is a sad, fascinating story worth reading about, one that is often forgotten due to a Saudi media blackout and the 444-day Iranian hostage crisis, which had begun several weeks earlier and was consuming much of America’s attention.

At the time, the siege had a number of immediate consequences, owing partly to confusion as to who had orchestrated it. As we have already seen, Acga claimed the Pope was involved. Many others believed the US was behind the siege. This resulted in the destruction of US embassies by mobs in Libya and Pakistan on December 3. Others believed Shia revolutionaries in Iran were behind it. This led to an uprising in the Eastern Province of Saudi Arabia, where the country’s Shia minority population lives and most Saudi oil is located. People there had been attempting to celebrate Ashura on November 25, a major Shia holiday prohibited in Saudi Arabia.

Shia-Sunni political relationships were also deteriorating elsewhere in the Middle East in 1979, part of a process that helped lead to the most deadly war in the recent history of the region, the Iran-Iraq War, the following year. At the start of the year Iraq and Syria had been discussing the possibility of unifying their armed forces and merging into a single state[6], to counter Egypt’s new relationship with the US and Israel. The Shia Islamic revolution in Iran however created the possibility of a closer relationship between Iran and Syria. Syria’s government, led by Hafez al- Assad and the country’s minority Allawite (a branch of Shia Islam, sort of) elite, was at the time fighting Sunni groups such as the Syrian Muslim Brotherhood. Syria also had interests in the Lebanese Civil War (1975-1990)[7], a religious sectarian war in which Shia forces – a few years later emerging as the Party of God, Hezzbolah – were being energized by the Iranian revolution as well as by Israel’s invasion and subsequent withdrawal from Shia-inhabited South Lebanon in 1978.

In Iraq the reverse situation existed. The Iranian revolution frightened Iraq’s Sunni elite, in part because a majority of Iraq’s population were disenfranchised Shia. This may have led Saddam Hussein, then vice president of Iraq, to overthrow his elder cousin Ahmed Hassan al-Bakr, the president, on July 16, 1979. A week later Saddam carried out a public purge of Iraqi politicians, claiming they had been plotting with Syria to overthrow the government of Iraq. The following April, he ordered the execution of Iraq’s Grand Ayatollah Muhammad Baqir al Sadr (whose son-in-law, the cleric Muqtada al Sadr, is today arguably the most influential politician in Iraq), along with al Sadr’s sister Amina, before beginning an eight-year war against the ayatollahs in Iran in the fall.

The year ended with the Soviet invasion of Afghanistan on Christmas Eve[8]. This was followed two days later by the Soviets killing their former ally, Communist Afghan President Hafizulla Amin[9]. US president Jimmy Carter then signed the order for the CIA to provide lethal aid to the Afghan mujahedeen. Most of this aid was facilitated by the Pakistani regime of Zia ul Haq, who came to power in a coup at the end of 1978 and would, more than any other figure, be responsible for transforming the Pakistani state from secular to theocratic. The decade-long resistance of the mujahedeen against the Soviets and their allies would result in the deaths of perhaps a million people.

Thus it can be seen that 1979 was also a turning point in the extremely violent Cold War. From a time of “national malaise” in the US (to reference the famous speech by Carter that year[10]), which was dealing with an energy crisis, a hostage crisis, and recent memories of Vietnam[11], 1979 would set in motion forces that would lead to a US victory in the Cold War ten years later. But then, it would also lead the US to its wars in Iraq and Afghanistan, at the start of another new millennium.

Ultimately, 1979 was significant not only because of its mix of religion and politics, a mix which obviously was not new at the time and has not gone away since. It was also important because the events of that year helped to shape the views of a generation of people who, today having reached their fifties, sixties, or seventies, can now shape events themselves[12]. Perhaps this has contributed to the fact that American relationships with Iran and Russia remain hostile just like they were in 1979, while American relationships with countries like China, Saudi Arabia, and Egypt remain cooperative just like they were in 1979. True, there are signs that some of these relationships may be beginning to change. But for today at least, 1979 remains a guide worth remembering.

Notes:

[1]This attack took place just as a public debate over whether or not it was appropriate to satirize religion was taking place in Britain, as only ten days earlier the Monty Python movie The Life of Brian had first been released. The movie was banned in the Republic of Ireland until 1987.

[2]Another prominent figure assassinated in 1979 was Park Chung-hee, who had been the president of South Korea since 1963, first coming to power in a military coup in 1961. He was shot by his close friend, the head of Korea’s CIA. Park’s daughter was recently president from 2013-2017, but was then impeached.

[3]Two weeks before the Pope’s visit, Ireland passed the Health Act, which legalized the selling of contraception for the purposes of family planning. China then said I’ll raise you one better, launching, in effect, mandatory contraception: 1979 was the year the one-child policy was born.

[4]Actually, Agca himself later claimed the KGB was involved. But he has a track record of making untrue, self-aggrandizing statements, so this does not prove anything.

[5]Most of whom were released at the beginning of the siege. There were an estimated 50,000 pilgrims in the Mosque to begin with, but only a relatively small percentage of them were kept hostage during the siege’s two-week duration.

[6]Like Syria and Egypt had done from 1958 to 1961.

[7]Another arena of political conflict, Cold War rivalry, and religious activity was Central America, where wars in El Salvador, Guatemala, and Nicaragua were taking place around this time. A key event in El Salvador’s civil war (1980-1992) was the assassination of Archbishop Oscar Romero, which took place while he was at mass in March of 1980, a day after he had publicly asked Salvadoran soldiers not to carry out orders to kill civilians.

[8]Though not in Orthodox countries like Russia, where Christmas is on January 7.

[9]He was not the only Amin to be ousted from power in 1979. Uganda’s Idi Amin (no relation) was removed too, by an invading Tanzanian army.

[10]Though Carter never actually used the word malaise in the “malaise speech”.

[11]At the 1979 Academy Awards, The Deer Hunter won Best Picture while Jon Voight and Jane Fonda won Best Actor and Best Actress for Coming Home. Both were films about Vietnam. Apocalypse Now, meanwhile, went on to win the top prize at the Cannes Film Festival in 1979 (but was then snubbed in favour of Kramer vs Kramer at the Oscars in 1980).

[12]In 1979, Donald Trump started building Trump Tower. Bill Clinton was elected governor of Arkansas at the age of 31. An 18-year-old Barack Obama moved to the US mainland to attend a liberal arts college in Los Angeles. Xi Jinping finished his degree in chemical engineering, as a “Worker-Peasant-Soldier student” in Beijing. Angela Merkel too was becoming a chemist in a Communist state, having finished her physics degree at the end of 1978 in Berlin. Shinzo Abe finished his degree at the University of Southern California. Narendra Modi graduated from the University of Delhi in 1978 and began working for the Hindu nationalist paramilitary organization, the RSS, in 1979. Theresa May graduated from Oxford in 1977; Jeremy Corbyn entered politics as local councillor in 1979. Bibi Netanyahu and Mitt Romney were coworkers and friends at the Boston Consulting Group.

Additional notes:

In democratic countries, political analysts often try to sniff out any regional divisions that exist within a given country by looking at the voting patterns of that country’s electorate. In Italy’s recent election, for instance, it has been thought to be significant that Italians living in northern Italy tended to vote centre/right (including for the Northern League), whereas in southern Italy people tended to vote for the Five Star Movement.

In countries like the People’s Republic of China, however, where no such elections are held, different factors may be looked at instead, in order to gauge the level of regionalism that might exist.

One interesting thing to note here is that almost none of modern China’s top politicians were born in peripherally located areas in the country’s southeast, southwest, northwest, or northeast. The only province in southeast or southwest China to have produced a somewhat notable number of Politburo members is Fujian, a relatively small province where Xi Jinping served 17 years of his career, which is important to China in part because it shares unique social and linguistic connections with the nearby island of Taiwan.

The chart above shows, by birth-province, the number of members in the politburo, politburo standing committee, party secretariat, central military commission, provincial party secretary, or previous politburo standing committee members going back to 1990, adjusted to take into account the varying population sizes of each province. Apart from Fujian and Qinghai (which ranks high on this list only because it has such a tiny population, by China’s standards), all of the provinces at the top of this list are in the north or central coastal regions.

China’s most populous province, Guangdong, has had no leaders on this list. As of 2017, Guangdong may have also broken a thirty year tradition by having its provincial governor not be a native of the province. It is now one of the few provinces not to have a native-born governor.

In this picture above, we see the birthplaces of China’s current top leadership, the members of the Standing Committee. Here we also see the one big exception, Qinghai-born Zhao Leji. Zhao’s career is noteworthy. Zhao served as party chief of Qinghai, breaking the unwritten rule that a person should never be party chief in their birth-province. Zhao was later party chief in Shaanxi, where his parents were from; this too broke an unwritten rule, that a person should not be party chief in their “native” province. Now, Zhao has not only reached the Standing Committee, but has taken over Wang Qishan’s anti-corruption job, a critical position. Some have argued that Zhao has been able to rise in this way mainly because Xi Jinping’s family is also from Shaanxi.

Here’s a map of the birth-provinces of the current 25-member Politburo Central Committee (which includes within it the 7 members of the higher-ranked Standing Committee):

And here, finally, is a map of the birth-provinces of the current provincial party chiefs:

The year 2017 has short, medium, and long-term significance in China.

Its short-term significance comes from the Communist Party’s quinquennial leadership transition, which is being held a week from today.

Its medium-term significance comes from being the twentieth anniversary of the most recent notable geopolitical transition in China; namely, of Hong Kong leaving the British to join (in effect) China’s largest province Guangdong, and of Chongqing leaving China’s formerly-largest province Sichuan, in 1997*.

Its long-term significance comes from being the 100th anniversary of the Russian Revolution; of which, with the Soviet Union now long gone, the Chinese Communist Party is the only major remnant. The Party’s centennial is itself arriving in 2021, the first deadline in Xi Jinping’s “Chinese Dream”.

It is interesting to think on how these factors may overlap. The Russian Revolution of course brings to mind the Soviet collapse. That collapse occured 69 years after the Soviet Union’s formation; next year will be 69 years since the People’s Republic of China’s formation. These memories may be reenforcing the desire of China’s leadership to avoid the mistakes they perceive Gorbachev to have made. In a small way, this might be contributing to the Party’s granting more power to Xi Jinping. The promotions Xi makes this week are being watched closely, worldwide, as a yardstick of his clout.

Geopolitics within China

The twentieth anniversary of the political changes to the Hong Kong-Guangdong and Sichuan-Chongqing regions are, arguably, deeply relevant to this issue.

First, the two men Xi is expected to highlight as long-term successors of himself and of Premier Li Keqiang currently lead those regions. Chen Min’er is the party chief of Chongqing, Hu Chunhua is the party chief of Guangdong. Both will have an incentive to keep their regions pliant, in order to realize this rise to the top.

Second, the strongest moves in Xi’s anti-corruption campaign have been taken against top leaders in the Sichuan-Chongqing region: against Sun Zhengcai, party chief of Chongqing, a few months ago, and against Zhou Yongkang, a former chief of Sichuan, in 2015. Sun will be the first Politburo member kicked out under Xi. He will be just the third incumbent Politburo member to fall in the past 20 years, and yet the second party chief of Chongqing (the other being Bo Xilai, in 2012) to do so.

Third, Guangdong and Sichuan are by far the largest of China’s “peripheral” provinces (see graph); provinces outside of the part of China that, roughly speaking, lies between or near Beijing and Shanghai. Few recent Chinese leaders have been born in peripheral provinces; the new Standing Committee that Xi is expected to pick will not have anyone born in a peripheral province. Neither was anyone on the current Standing Committee* born in a peripheral province. Indeed, nobody born in Guangdong or Sichuan holds any of the 43 positions within the Communist Party’s Politburo, Secretariat, or Central Military Commission.

Read the full article here: Geopolitics within China

On The Future of the Canadian Auto Sector

There is a profound difference between Canadians, Americans, and Chinese, both in their demographics and in their dreams.

In the US, the largest population group is 20-35 year olds. Many of these Americans will, in the years ahead, be looking to pursue the American Dream: to buy a home and start a family. Indeed, just like the Baby Boomers before them, many of these Millennial Americans have been moving to suburbs and buying SUVs.

In Canada, in contrast, the largest group is 50-60 year olds. In the years ahead, many of these Canadians will be looking to cut back their work hours, or retire, or transition from manual labour to less physically strenuous jobs. Many will also pursue the Canadian Dream: having a cottage to host one’s grandchildren at.

In China, the largest group is 40-55 year olds. Most of this group works in physically demanding industrial or agricultural jobs. Most of them, particularly in China’s rural areas and inland provinces, still earn between 2-10 dollars a day. The Chinese Dream is to let these aging manual labourers transition to less strenuous work, while also bringing the country’s impoverished rural areas and inland provinces out of poverty.

Ontario’s Position

These demographic trends are not alien to the auto sector in Ontario. A city like Windsor is, in a certain sense, situated in a delicate borderland, between the vast American consumer market on the one hand, and the smaller domestic market of Canada but larger global market on the other hand. This is a risky, though often rewarding, position to be in. When successful, it has allowed Ontario to attract investment from global firms seeking a way to access to the American market without investing too much in the US directly. In the wake of the recent Valiant deal, such investment is increasingly expected to come from China.

Obviously, however, global firms cannot rely for certain on continued favourable access to the American market, regardless of whether or not these firms have investments just across the US-Canada border within Ontario. It is up to Ontario to determine to what extent it wants to orient its production around markets in the United States, and to what it extent it wants to focus on Canadian or global consumers instead.

A Possible Divergence

This is where trends such as demographics become relevant. As a result of such trends, it may be the case that consumer demand in the United States will diverge sharply from that of countries like Canada and China in the years ahead. While Americans continue to buy cars and SUVs, in Canada and in global markets it may be instead that auto sector demand will become increasingly dominated by busses and by trucks:

1. The Supply of Drivers

The global Baby Boomer bulge, of 50 and 60 year olds in the West and of 40 and 50 year olds in China, is likely to create the largest labour shift in human history: manual labourers transitioning to less strenuous work. In spite of what some politicians may claim, these labourers will not often be retrained to become software engineers. Nor will they all move into retail jobs at companies like Walmart, as out-of-work labourers have often done during the past generation. Too many of these retail jobs are being automated out of existence. Rather, the single biggest job these labourers are likely to switch to is driving a motor vehicle.

Not only is driving a bus, truck, or taxi something that can be done by a person who has, say, a bad back, it is also becoming far less strenuous than ever before, as a result of technological additions to modern vehicles. Driving large busses and trucks has been somewhat difficult in the past, particularly in tasks such as parking, turning, or driving on country roads during challenging weather conditions or in the dark of night. Modern vehicles, on the other hand, equipped with cameras, sensors, and high-tech safety features, are in the process of making the job of driving relatively comfortable and safe even for 60 or 70 year olds.

If the Baby Boomers create a glut of drivers globally, the costs of using trucks, busses, mini-busses, etc., will fall.

2. The Night Moves

Of course, there has also been plenty of discussion in the media about the possibility of self-driving vehicles. If such vehicle actually do become commonplace anytime soon, they will have the largest impact on places and at times in which there is today a scarcity of human drivers. Namely, they will the largest impact on late-night driving (when human drivers are mostly asleep) and on areas such as, for example, Canada’s far northern regions, where — particularly during long, cold winter nights, or in snow storms, or on dangerous ice roads that require almost constant maintenence — there are few human drivers around.

Autonomous capabilities would have a much greater impact on trucks than on cars, then; and in particular, on short trucks, where labour costs per unit of cargo are much higher than for heavy trucks or transporters. They would also have a greater impact on places with challenging geographies, such as Canada. And they would be especially useful for slow-moving overnight vehicles, like plows, de-icers, and pavers.

Trucks, finally, may experience the benefits of autonomous driving earlier or more than other vehicles will as a result of government regulation. While governments may be hesitant to allow autonomous cars in general at first, they are far more likely to allow a truck driver to turn on an autonomous cruise control system late at night, when relatively few cars are on the road, so that he or she can get some sleep.

3. More Time, Less Money

These two trends we have discussed thus far — demographics and automation — may also lead to a phenomenon in which Canadians’ free time will increase at a much faster pace than will their income levels. This could occur because of an aging Canadian worker entering into full or partial retirement, or it could occur because of a Canadian worker losing his or her job to a software system or machine. Either way, Canadians are likely to have more time to fill up their schedules with leisure activities — say, spending more time in cottage country — but will also have to economize on costs in order to afford them.

One way to economize on leisure spending would be to forgo car ownership (or at least, to share a car with a spouse instead of owning two cars per couple) and using transit more. Busses, for example, are slower than cars — as they often make stops to pick up and drop off passengers along their routes — but also cheaper than cars, particularly once you factor in the cost of car ownership. If the cost of bus drivers declines (which, as we have discussed above, we think it will), busses would become cheaper still. As Canadians’ free time increases faster than Canadians’ incomes, busses might therefore see greater use.

4. The Transit Revolution

Apart from their sometimes being slow compared to cars, another major reason many people do not use transit regularly is because of the “last-mile” problem: how to get from a transit station to one’s destination, without a car. Also problematic is the “first-mile” problem: how to get to the transit station if the station’s parking lot is full, or if you do not own a car. Yet these “first-mile/last-mile” problems are likely to be solved—or at least, made far less problematic—in the near future, as a result of technological changes.

One technology to overcome the first-mile/last-mile challenge is that of services like UberPool, wherein passengers and drivers easily co-ordinate door-to-door carpools through their smartphones. This same system could be used by busses or mini-busses too, which would make the rides cheaper but also longer—see the More Time, Less Money section above. Systems like UberPool work best in markets that are “liquid”; i.e. big-city markets, where there lots of passengers and drivers around. The US, being highly suburban, may be less suited to this than Canada (where more people live in large cities) or most global markets.

Another way to overcome the “last-mile” challenge is via car-sharing services, such as Car2Go or Zipcar. These allow people to take a car from the transit station to reach their destination. Use of car-sharing services in Canada is growing. It may eventually make it easier for some people to forego car ownership entirely.

As services like car-sharing and ride-sharing advance, then, transit’s “first-mile/last-mile” problems may be overcome.

5. The Canadian Shield

If transit really does become more common relative to car usage, it will in many places be dominated by rail transit. Similarly, railways will continue to transport more freight than trucks. Trains are, after all, more efficient than trucks and busses. They will remain more efficient even if the cost of hiring a bus or truck driver falls.

Where trucks and busses will be utilized most, then, is in locations where it is difficult for railways to function. We have already mentioned one location where railways are difficult: Canada’s far north, where permafrost impedes rail construction and maintenance, and ice roads are sometimes the only economical option.

Another region where railway construction is expensive is the Canadian Shield, the result of the Shield’s enormous size, exposed rock shelves and over-abundance of lake (the latter being proble matic given that trains cannot easily make sharp turns to bypass them, as trucks can). If Canadians, armed with more free time than ever before, seek the Canadian Dream in the lakeside cottages of the Shield, they will have to rely on trucks to transport bulk necessities like food (as the Shield is not suitable for agriculture) and fuel.

Railways networks are also under-built in mountainous areas, as trains cannot handle either sharp turns or steep inclines well. Three of Canada’s four major cities — Vancouver, Montreal, and Calgary — are located a very short distance from mountains, in contrast to US population centres which tend to be located in spatious coastal plains or the even larger Midwestern/Central Plains. It might be expected that, as a result of having more free time to spare, Canadians will spend more time pursuing leisure activities in mountains.

Meanwhile, countries like China are now actively trying to develop their impoverished inland regions, many of which are mountainous and have relatively little access to either railways or to coastal shipping—and will therefore have to rely on trucks and busses for their transportation. Many other developing economies, in South Asia, Latin America, and Africa, are also mountainous and landlocked. The largest city in NAFTA, Mexico City, is the highest-elevation in the world among cities with at least four million residents. Still, it is China which is the king of highlands. China’s Tibetan Plateau and Himalayan region occupies roughly one-fifth of China’s landmass, and is similar to the Arctic in its permafrost risks, sparse population (it has less than one half of one percent of China’s population), low rail access, and resource wealh.

Conclusion — Canada and the World

Canada typically has one foot in the American market and one foot in the Canadian and global markets. Canadians companies often wonder what trade regulations or barriers the Americans will insist upon, either for Canadian firms or for foreign-owned firms invested in industrial facilities within Canada. But if, also, markets diverge — if Americans continue to use conventional four-seater cars and SUVs and trains, while Canadians and global market players like China increasingly look to buy busses and trucks — then Canada’s auto sector could also have to answer a more basic Canadian question: just how American are we?

As usual, there are no easy answers here, only risks and rewards.

According to an article in The Economist, the value China’s outbound M&A activity rose sharply in 2016, up approximately fivefold since the summer of 2015 and eightfold above its average rate between 2010- 2015.

The article mentions that this increase could represent a troubling trend for China, of capital fleeing the country in response to its slowing economic growth rate and gradually depreciating currency in recent years.

It then largely dismisses this theory, however, saying, “rather than sparking a stampede [of money] to the exits, it is more accurate to say that these changes [in China’s economic performance] have alerted Chinese firms to the fact that they are still woefully under-invested abroad. China’s share of cross-border M&A has averaged roughly 6% over the past five years, despite the fact that it accounts for nearly 15% of global GDP”.

In other words, the article assumes that, if a country’s share of global M&A does not exceed its share of global GDP, its M&A is less likely to be capital flight. This assumption is not justified, however. It overlooks other key factors that may determine a country’s propensity for engaging in outbound M&A. Such factors include:

1. A country’s physical proximity to other large economies

In order to have cross-border M&A, you need borders to cross. Economies with large neighbours, for example Canada or the Netherlands, tend to have a relatively high propensity for engaging in international M&A.Canada’s cross-border M&A, for example, has tended to be 25-50% as large as the US’s in recent years, in spite of the fact that Canada’s GDP is less than 10% as large as that of the US. China, unlike Canada, does not border any large economies. This impacts not just its M&A, but also trade: in China trade counts for 37% of GDP, whereas in Canada it is 64% and in the Netherlands it is 151%.

2. A country’s cultural and linguistic affinity with other large economies

Most economies in the world speak European languages; Northeast Asia remains something of a linguistic outlier. This may make Northeast Asian countries less likely than other regions to engage in global M&A. Japan, for instance, currently accounts for 6.5 percent of global GDP, yet has accounted for less than 1 percent of global inbound M&A in recent years, and less than 4 percent of cross-border M&A in general. Arguably, China too might be expected to have a low propensity to engage in M&A.

3. Capital availability versus investment opportunity

One of the reasons that Japan’s outbound M&A far exceeded its inbound M&A is that capital in Japan has been cheap (its interest rate is below zero), yet investment opportunities in Japan have been limited (its economic growth rate is 1 percent). Thus, the Japanese borrow money cheaply at home, and often invest it abroad. In China, however, interest rates frequently top 4 percent, while economic growth is estimated to be 6-7 percent. We might, then, expect China to be less M&A-intensive, and generate more of its own investment opportunities domestically rather than seek out ones in foreign markets. Unless, of course, as many economists suspect, China’s true growth rate is much below 6-7 percent.

4. A country’s political relationship with other large economies

Outside of mainland China itself, approximately 45 percent of East Asia’s GDP is generated in Japan, China’s historic regional rival. Outside of mainland China, approximately 29 percent of global GDP is generated in the US, China’s potential global rival. Because China’s relationship with Japan and the US is sometimes a tense one, its investment relationship with Japan and the US may be less than it could otherwise be. For instance, when a territorial spat between China and Japan, over the Senkaku/Diaoyutai islands, heated up (rhetorically) around 2012, cross-border M&A between China and Japan fell sharply. Indeed, in spite of relatively close cultural connections, Japan was not even one of China’s top ten targets of outbound M&A spending in the past decade. China has tended to invest in Europe; Japan in its political ally the US. 43 percent of Japan’s outbound M&A in the past decade went to the US.

5. A country’s relationship to foreign financial hubs

Relatively independent financial hubs, like Hong Kong, Singapore, or Luxembourg, tend to be significant net providers of M&A capital. Their outbound cross-border M&A spending tends to far exceed their inbound M&A, and their global share of cross-border M&A tends to far exceed their global share of GDP. From 2011-2014, for example, Hong Kong’s outbound M&A was about 25-40% as large as mainland China’s, even though Hong Kong’s GDP is only around 2% as large as mainland China’s. (Rightly or wrongly, M&A statistics tend to treat Hong Kong as if it was an independent entity). The fact that the world’s top two financial city-states (Hong Kong and Singapore) are Chinese may suggest that mainland China’s propensity for outbound M&A should be relatively low—just as, for example, US outbound M&A would plummet if (hypothetically) Manhattan were to secede from the US.

The value of China’s outbound M&A as a share of global cross-border M&A should, perhaps, be lower than China’s share of global GDP, then. Yet in 2016 Chinese buyers accounted for an estimated 15 percent of the value of all cross-border M&A, slightly higher than the 14.5 percent of global GDP China had. The Syngenta deal alone, announced in early 2016, was roughly large enough to eclipse all outbound Chinese M&A in any year prior to 2014. China has kept up its M&A pace thus far in 2017, not counting Syngenta.

The explanation that you often hear for why China’s M&A boom is not capital flight — namely, that Chinese firms are seeking foreign expertise and technology, as China transitions to a more knowledge-intensive economy — may have some merit, but still it ignores the fact that money has also been pouring out of China into other assets in the developed world in recent years. To take the most notorious example, Chinese capital been pushing up real estate values in Pacific cities (Vancouver, Seattle, Sydney, etc.) and hub cities (NY, London, Toronto, etc.). The M&A boom, then, may be part of the greater trend of Chinese capital seeking safe haven. China’s 2016 M&A investment in the global safe haven, the US, was roughly triple what it had been in 2015, 2014, or 2013. It was larger than in every year from 1990-2012 combined.

If much of China’s M&A boom really is a result of capital flight, it is also likely to be unsustainable. In part two of this article we will analyze China’s geopolitical structure, to see when (or whether) this boom will end.

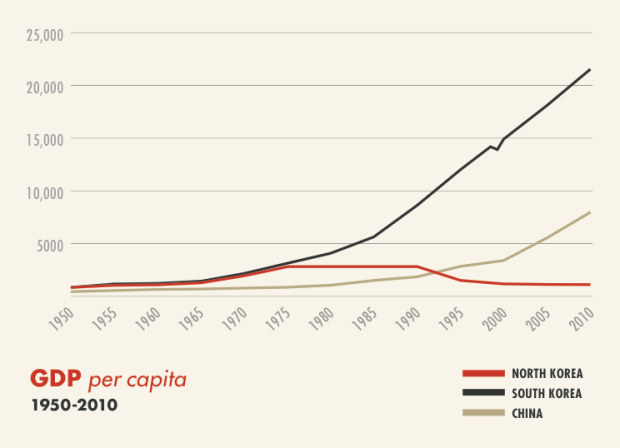

The Korean War, fought from 1950-1953, was a result of two earlier wars in the 1940s: the US-Japanese War, which ended with the destruction and occupation of Japan in 1945, and the Chinese Civil War, which ended in a Communist victory (and Nationalist retreat to Taiwan) in 1950. With the Communists and Americans as the only powers in East Asia following these wars, the Korean peninsula was split in two, each side taking a piece for itself.

When the US triumphed over the Soviet Union around 1990, many expected the North Koreans to fix their broken ties with South Korea. That this did not occur was partly the result of inertia, partly the result of Kim Il Sung’s living until 1994, and partly the result of the 1997 East Asian financial crisis, which kept the South Koreans too poor to want to incur the cost of investing in North Korean infrastructure or labour.

It was also partly the result of a miscalculation on behalf of North Korea in 1987, twenty-four months before the Berlin Wall came down. Seeking to ruin the South’s first-ever Olympics in 1988, the North blew up a commercial airplane. It was by far the deadliest attack on the South since the armistice began in 1953. South Korea’s anger and mistrust of North Korea as a result of this deed persisted during the ’90s.

When the 21st century arrived the situation changed again. The US, after having fought the bulk of its four major 20th century wars in East Asia—in the Philippines, WW2, Korea, and Vietnam—shifted its focus elsewhere in 2001. This shift was mainly a result of US wars in Afghanistan, Iraq, and Libya. To a lesser extent, it has also been a result of recent Russian interventions in Georgia, Ukraine, and Syria .

In East Asia, meanwhile, China’s GDP surged, while Japan’s continued to stagnate like it had in the ‘90s. Between Chinese growth, Japanese stagnation, and US distraction, East Asia became again a two-power region: the United States and China now dominate the region. But this may now be ending. In the years ahead, East Asia is likelier to become either a one-power region, like it was in 1990s, or a three-power region (the US, China, and Japan). The two-power status quo could remain in place, but is hardly certain to do so.

In a one-power or three-power region, the powers involved may have less to gain from the continuation of poor relations between North and South Korea. There will be much less reason to split Korea in two, as it has been for 67 years now, when East Asia as a whole is not split between two major powers, as it is today.

The move towards a one-power East Asia, or towards a three-power East Asia, is plausible for three reasons:

First, the US has been drawing down from the Middle East. It had 150,000 soldiers fighting in Iraq and Afganistan in 2011, but now has fewer than 15,000. Unless it decides to wholly reverse this process — Trump has announced the addition of 4,000 soldiers to Afghanistan, but that is a far cry from the Obama-era surge—the US will have the ability to focus on other regions, like East Asia, more than it could during the 2000’s.

Second, China’s GDP growth has slowed, from 10-15 percent growth during the 2000s to 3-7 percent (depending on whether you believe its official growth rate, 6.7%) last year. In order to keep up with 2.5 percent US growth, China must grow around 4 percent. China’s challenge in doing this is that its labour is now much costlier and older than it used to be, while its resource wealth, most notably its coal, has led to pollution.

China may struggle to keep up with US power. As it is, the US economy is an estimated 1.6 times larger than China’s. [The US-Canada-Britain-Australia alliance, meanwhile – which, unlike China itself, more or less speaks a single language – has a GDP 2.2 times larger than China’s]. The US GDP alone is larger than that of East Asia as a whole.

Third, the economy of Japan, which today is an estimated 37 percent as large as China’s and 18 percent larger than Germany’s, is likely to benefit from the crash in oil and other natural resource prices that began in mid-2015. Unlike China, Japan has few resources of its own, and so depends on imports to fuel its economy.

While Japan’s aging population continues to be a challenge — Japan’s largest age cohorts are 40-45 year olds and 65-70 year olds — it may be able to address the challenge via automation, immigration, and a labour force dominated by technically skilled 50-80 year olds. Japan is already planning to advance its robotic prowess in the near term, as it wants to showcase them at the 2020 Tokyo Olympics.

Japan’s robot drive is likely to have consequences not just for the Japanese economy, but also for the Japanese military. Japan has already begun to rebuild its military of late, first in response to China’s rise and then in response to Donald Trump’s rhetoric that US allies should “stop freeloading, and pull their own weight”. Already today the Japan ranks 8th in military spending, despite devoting just one percent of its GDP to it. Should Japan double this, to reach the 2 percent of GDP that France and Britain spend, it would then become the third largest military spender in the world, and move far ahead of the next largest, Russia. (Were Japan to spend 5 percent of GDP on its military like Russia does, it would move far ahead of China).

Even if Japan does not re-emerge, East Asia might not remain a two-power region. Rather, China could fall behind the US sufficiently that, in effect, it will be a one-power region again, like it was in the 1990s. US power is rising not only due to its withdrawal from the Middle East, but also because its rivals, most notably Russia, are being hurt by the fall in resource prices. As in the ’90s — when oil prices were at all-time lows — cheap oil works in the US’s favour. And if US power in the region does rise, the North Koreans might be less willing to resist its demands.

There is an additional reason for improving relations between the North and South: it may benefit the South’s economy. Unlike in the 1990s, South Korea is now a relatively wealthy country. Yet because of its rapid growth, it has become dependent on imports of natural resources and exports of manufactured goods. South Korea has been importing resources mainly from the Middle East, and exporting mainly to China.

The Middle East, however, remains unstable. Qatar, for example, the world’s largest LNG exporter, sells more to South Korea than to any other country. But Qatar is now in open conflict with Saudi Arabia. Uncertainty of this kind threatens South Korea’s GDP growth. In addition, as China tries to shift from coal to gas, and as Japan tries to shift from human labour to fuel-powered robots, South Korea may have to deal with rising competition from its own enormous neighbours when importing fossil fuels from the Middle East.

Similarly, South Korean exports have been limited by the slowing Chinese economy. China accounts for a quarter of all South Korean exports, more than the US and Japan combined. South Korea has also been hurt by its own success: its labour is no longer so cheap like it was in previous decades, when it was still a poor country. For these reason, South Korea has already grown more slowly in the past two years that at any time since 1997 (excepting the global financial crisis in 2009).

These economic troubles are occuring at a bad time for the South. South Korea will host the the first-ever Winter Olympics in continental Asia this year. It wants the world’s perceptions of itself—namely, that it is a remarkable country, with remarkable companies like Samsung and remarkable economic prospects in general—to endure. It also does not want the North to cause trouble this time, as occured in 1987.

Trading with North Korea could help address both these concerns. North Korea has an extremely cheap, Korean-speaking labour force; a labour force that includes cousins, and in some cases even siblings, of the South’s. It represents a potential Korean-speaking market for South Korean exports, both of media and manufactured goods. It even, if ties improve enough, offers opportunities in tourism. And it offers access to natural resources. The North Koreans are rich in coal; the South Koreans are top coal importers. More importantly, the North offers a land route by which South Korea can access resource-rich Manchuria and Siberia.

It is possible, of course, that the Korean issue will be addressed by war rather than by trade. In the past year alone, the US has prepared for such a war. It is also possible that the North will not be addressed at all; that the tyrannical staus quo will endure. But for the reasons outlined above, I believe reconciliation is the most likely, and the status quo the least likely.

Dennis Rodman, who played on the the 1990s Chicago Bulls (Kim Jong Un’s favorite basketball team) has lately met with Un. Do not be suprised if Rodman’s Celebrity Apprentice co-star, Donald Trump, follows suit.

There is a recent pattern in American politics, in which Democratic politicians who succeeded in presidential elections were not born in northern states (e.g. Obama, Clinton, Carter, Johnson, Truman, and, if you must, Al Gore), while Republicans who won presidential elections — so, not counting Ford, who inherited Nixon’s presidency post-impeachment — have had very close ties to either Texas (the Bush’s, Eisenhower), California (Reagan, Nixon), or Florida (Bush, Trump).

To some degree, this pattern presumably reflects the old divide between the country’s Northeast and Southeast. The Democrats, who have their base of support in the Northeast, have had trouble in elections when they do not reach out to the South by selecting one of its native sons as their candidate. The Republicans, who have support in the Southeast, have had trouble winning when they do not secure the support of at least one of the country’s three largest states—California, Texas, or Florida.

Looking at the home regions of China’s leading politicans, it is fairly easy to discern a similar north-south divide. A large share of Chinese leaders were born in northern China. These include Beijing-born Xi Jinping (who’s father, Xi Zhongxun, was from Shaanxi) and Shandong-born Wang Qishan (a former mayor of Beijing, now Xi’s anti-corruption chief). At present, out of China’s seven Standing Comittee top leaders, only seventh-ranked Zhang Gaoli was born in southern China. Five of the seven were born in the north and one, Premier Li Keqiang, was born in in central China. Many politicians of the past, such as Zhao Zhiyang or Hua Gaofeng, have also hailed from the north.

Indeed, as far as I can tell, Zhang Gaoli may in fact be the first person in thirty years to be born outside of northern or central China and have made it to the Standing Committee. He is also the only person currently serving in the Party’s 25-member Politburo born outside north or central China.

Central China — which, somewhat confusingly, is sometimes considered to be part of Southern China, though it is located far north of the ‘deep south’ regions like Guangdong or Yunnan — has also produced its fair share of notable figures, such as Hu Jintao, Jiang Zemin, Li Keqiang, Zhou Yongkang, and Wu Bangguo, all of whom were born in Jiangsu or Anhui. There seems, in fact, to be a very recent trend in which, when the General Secretary is from northern China, then the Premier is from central China, and vice versa. So, for example, there is now the pairing of Xi and Li (born in Beijing and Anhui, respectively), and before them the pair Hu and Wen (Jiangsu and Tianjin).

Some may interpret this as an implicit power-sharing arrangement between central China and northern China. While at present most leaders come from northern China, this was not the case a generation ago. Jiang Zemin (born in southern Jiangsu), Zhu Rongji (northern Hunan), Li Peng (Shanghai), Hu Yaobang (northern Hunan), Li Xiannian (Hubei), and Yang Shangkun (Chongqing) were not from the north. Of the “Eight Elders” of the 1990s and 1980s, six were born in central or south-central China; the other two in Shanxi. Even Xi Jinping, a northerner, spent his political career in central China or south-central China, in Hebei, Fujian, Zhejiang, and Shanghai.

The pattern, if it does actually exist, does not appear to be unique to civilian political leaders. Among today’s 11-man Central Military Commission, seven were born within northern China, while two were born in north-central China and two in south-central China. None are from the deep south.

Meanwhile, out of the 205 active members of the Party Central Committee, fewer than 15 were born in the deep south*. (*Here, please correct me if I am wrong. I do not speak Mandarin, and finding this information was difficult. Bo Zhiyue’s work was useful and worth reading, but has a different emphasis). No person born in the vast southeast province Guangdong, or the vast south/centre- west province Sichuan, holds one of the 43 positions in either the Communist Party’s Politburo, Secretariat, or Central Military Commission, at or around the highest levels of China’s political hierarchy.

The Sichuan basin has also witnessed a spate of high-profile political take-downs in recent years, notably of Chongqing’ party leader Bo Xilai and, later, of Sichuan province’s former chief Zhou Yongkang. Now Chongqing’s party chief is Sun Zhengcai, who is the youngest member of the current 18th Politburo and formerly served as party chief of Jilin. Guangdong’s party chief, Hu Chunhua, is the second youngest member of the Politburo and formerly served as party chief of Inner Mongolia, after having spent most of his career working in Tibet.

This may be significant, in both cases. Southern China, as well as other areas that might perhaps also be considered to be ‘peripheral’ (including Inner Mongolia, Tibet, and even Jilin), appear often to have been used as something of a stepping-stone to power by young, up-and-coming leaders like Hu and Sun. The idea is—presumably—that they will do whatever it takes to secure the Party’s interests in those regions, given they have such bright future careers to lose if they fail to do so. Past instances may include Hu Jintao serving in Guizhou and Tibet, Zhao Zhiyang in Guangdong, or maybe even Xi in Fujian. In the case of Hu and Sun in Guangdong and the Sichuan basin, they might be there simply because of those regions’ large sizes and significance—but perhaps they are also there to preempt dissent.

…And yet. Much of China’s economic output is generated in areas from around Shanghai south to Guangdong; particularly if you include Taiwan as being part of the country. Guangdong alone accounts for an estimated 10% of mainland China’s GDP and more than 25% of its exports. This creates, perhaps, an unbalanced dynamic: China’s political periphery is also its top commercial engine.

Americans might be tempted to call this state of affairs “taxation without representation”. While I will not stoop to doing so, I would however be very interested in hearing feedback about these patterns from any of the billion or so people who are more knowledgable on Chinese affairs than I am.

Today, at $45-50 a barrel, the price of crude oil has risen significantly from the $30 lows it reached around the start of 2016. Still, it remains quite far below the $80-110 range in which it resided during most of the past decade, prior to its crash in mid-2014. Gas and coal prices, meanwhile, have in most areas of the world fallen even more than those of oil has. China, because it is the world’s largest net importer of oil and of fossil fuels in general, has often been viewed as a country that is likely to benefit from these cheaper prices.

This view may be incorrect. Not only do China’s energy imports not equal a large share of its GDP, but the growth of China’s energy imports going forward may be slower than many predict. Moreover, there is an enormous discrepancy in the amount of fossil fuels produced by various regions and provinces within China. As such, the crash in energy prices may excacerbate, or at least influence, some of China’s preexisting geo-political divisions.

Energy Imports

China may be the world’s largest energy importer, but it is has also become its second largest energy producer, and as such only relies on energy imports for an estimated 15% of its total energy consumption, in contrast to 94% in Japan, 83% in South Korea, 33% in India, 40% in Thailand, and 43% in the Philippines. In 2014 imports of oil were equal in value to just around 2.4 % of China’s GDP, according to the Wall Street Journal, compared to 3.6% in Japan, 6.9% in Korea, 5.3% in India, 5.4% in Thailand, 4% in the Philippines, and 3.3% in Indonesia.

South Korea and Japan also imported more than two and four times more liquified natural gas, respectively – the prices of which tend to track oil prices more closely than conventional natural gas prices do – than China did. China’s LNG imports barely even surpassed India’s or Taiwan’s. China’s imports of natural gas in general, meanwhile, were less than half as large as Japan’s and only around 20% percent greater than South Korea’s.

China, furthermore, tends to import energy from the most commercially uncompetitive, politically fragile, or American-hated oil-exporting states, such as Iran, Russia, Iraq, Angola, and other African states like Congo and South Sudan. In contrast, Japan and South Korea get their crude from places that will, perhaps, be better at weathering today’s low prices, namely from Kuwait, Qatar, the UAE, and Saudi Arabia. (Granted, China gets an enormous amount of oil from Saudi Arabia too; however, Saudi oil does not count for nearly as large as share of China’s oil imports as it does for Japanese or South Korean oil imports). Similarly, China gets much of its natural gas from Turkmenistan, Uzbekistan, and Myanmar, whereas Japan imports gas from Australia and Qatar and South Korea imports gas from Qatar and Indonesia. China’s top source for imports of high-grade anthracite coal, and its third largest source for coal in general, is North Korea.

China has, in addition, invested capital all over the world in areas hurt by falling energy and other commodity prices, both in developed countries like Australia and developing economic regions like Africa. With energy prices cheap, it may get low returns on these expenditures.

Energy, History, and Politics

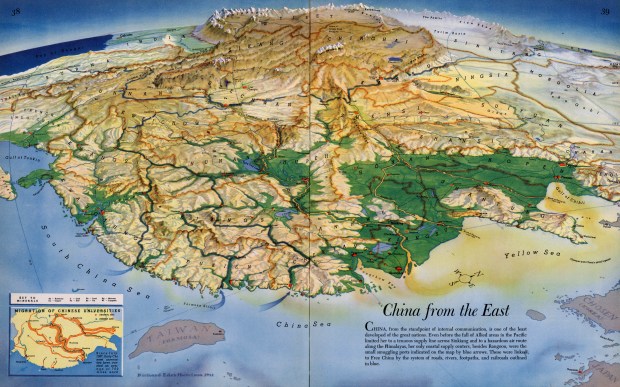

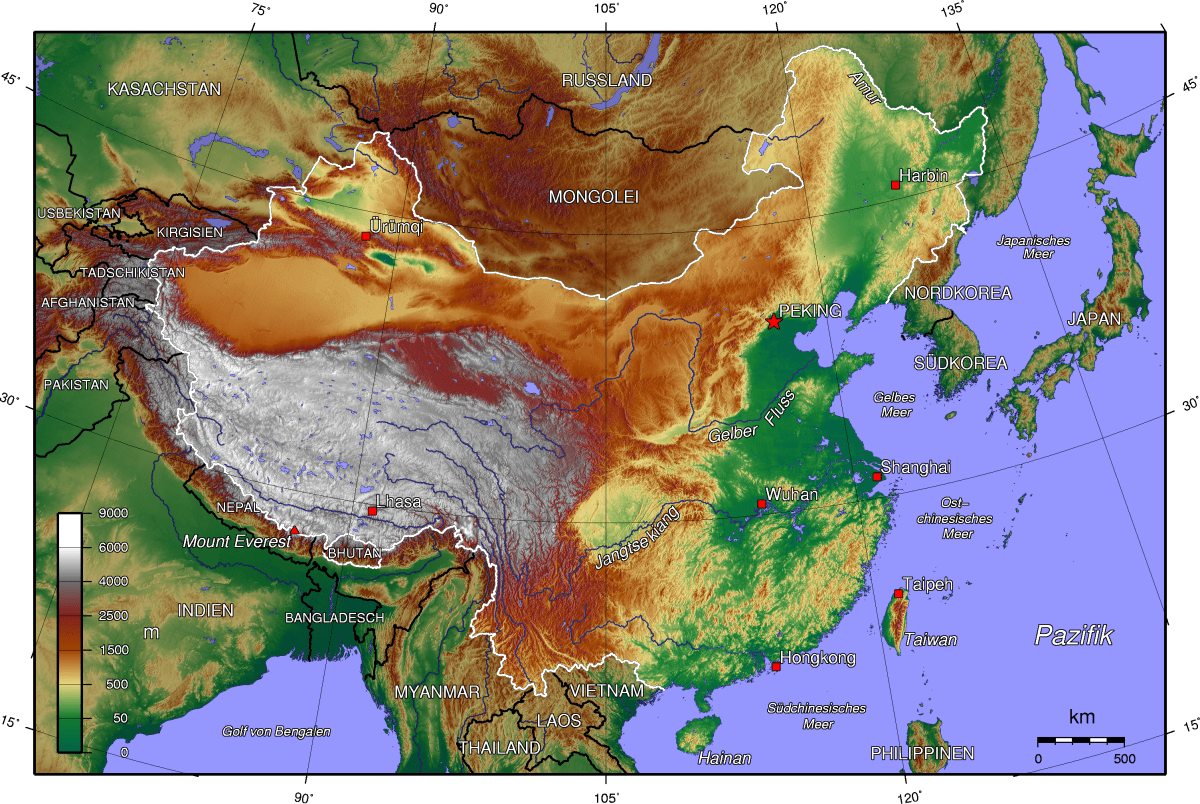

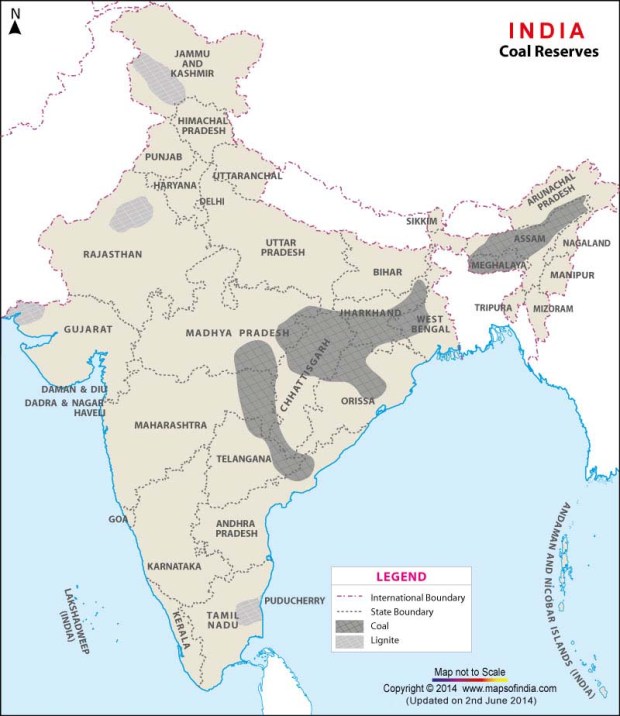

Another mistake the financial media makes is looking at China as if it were a country, rather than what it really is: both a country and a continent. Continents contain deeply-rooted divisions along regional, linguistic, and ethnic lines. China is no exception. China’s main division, roughly speaking, is between areas south of the Yangtze River, which tend to be mountainous, sub-tropical, and dependent upon importing fossil fuels, and areas north of the Yangtze, which tend to be flat, more temperate, and rich in fossil fuels.

China’s Physical Topography China’s Population Density

Northern China, stretching over 1000 km from Beijing southward to Shanghai on the Yangtze, is the country’s political heartland. It is densely populated and home to most of China’s natively Mandarin-speaking, ethnically Han citizens. When compared to southern China, the north has historically been somewhat insulated from foreigners like the Europeans, Americans, and even Japanese. Beijing’s nearest port is roughly 5000 km away from Singapore and the Strait of Malacca; Hong Kong, in contrast, is only around 2500 km from Singapore and Malacca. Beijing is rougly 2600 km from Tokyo by ship, whereas Shanghai is 1900 km from Tokyo and Taipei (in Taiwan) is 2100 km from Tokyo.

Japan’s Ryukyu island chain and the Kuroshio ocean currents historically allowed for direct transport from Japan to Taiwan and the rest of China’s southeastern coast; the Japanese controlled Taiwan for more than three and a half decades before they first ventured into other areas of China in a serious way during the 1930s. Even today, Japan accounts for a larger share of goods exports to Taiwan than do either China or the US.

Southern China has often depended on foreign trade, since much of its population lives in areas that are sandwiched narrowly between Pacific harbours on one side and coastal subtropical mountain ranges on the other. In northern and central China, in contrast, most people live in interior areas rather than directly alongside the Pacific coast.

People in the northern interior often did not engage in as much foreign trade as those on the coast, as, in the past, transportation in the interior was often limited by the fact that northern China’s chief river, the Huang-he, is generally unnavigable and prone to flooding northern China’s flat river plains, destroying or damaging roads and bridges in the process. In southern or central China, by comparison, even people living far inland could engage with the coast by way of the commercially navigable Yangtze and Pearl Rivers, which meet the Pacific where cities like Shanghai, Guangzhou, and Hong Kong are located.

Northern China, however, was most directly exposed to the land-based Mongol and Manchu invaders who ruled over the Chinese for most of the past half-millenium or so, prior to the overthrow of the Manchu-led Qing Emperor in 1912. Today, of course, the north continues to retain China’s political capital, Beijing, and a disproportionally large majority of Chinese leaders were born in northern China — including Beijing-born Xi Jinping and Shandong-born Wang Qishan, a former mayor of Beijing). This is in spite of the fact that most of China’s leading political revolutionaries in the twentieth century, including Mao Zedong, Deng Xiaoping, Sun Yat Sen, Chang Kai-Shek, Zhu De, Ye Jianying, Hong Xiuquan, and the writer Lu Xun, hailed from southern or south-central China.

At present, out of China’s seven Standing Comittee top leaders, only seventh-ranked Zhang Gaoli was born in southern China; whereas five of the seven were born in northern China and one, Premier Li Keqiang, was born in central China. Zhang Gaoli may in fact be the first person born outside of northern or central China in thirty years to have made it to the Standing Committee. He is also the only person currently in the 25-member Politburo born outside of northern or central China. Meanwhile, among the 11-man Central Military Commission, seven were born in northern China, while two were born in north-central China and two in south-central China. By my count, out of the 205 active members of the Party Central Committee, fewer than 15 seem to have been born south of central China.

Indeed, the southern half of China, stretching from islands in Taiwan, Hainan, Hong Kong, Xiamen, and Macau in the east to the plateaus of Yunnan, Sichuan, and Tibet in the west, seems to be politically peripheral. It is home to a majority of China’s 120 million or so non-Han citizens (most of whom are not Tibetan or Uyghur, though those two groups recieve almost all of the West’s attention), as well as home to China’s 200-400 million speakers of languages other than Mandarin, and to China’s tens of millions of speakers of dialects of Mandarin that are relatively dissimilar to the Beijing-based standardized version of Mandarin, and to most of China’s 50-100 million recent adopters of Christianity, and, finally, to most of China’s millions of family members of the enormous worldwide Chinese diaspora.

Southern China is closer to Southeast Asia, a region with an enormous, economically active Chinese population (many of whom speak southern Chinese languages like Cantonese), than is northern China. Southern China’s Fujian province, in particular, is both linguistically and economically close to Taiwan, and southern China’s Guangdong province—the largest province in China—to Hong Kong. A large share of China’s GDP comes from the coastal areas of China from around Shanghai south to Guangdong, particularly if you include Taiwan as part of the country. Guangdong alone accounts for an estimated 10% of mainland China’s GDP and over 25% of its exports. This creates, arguably, an unbalanced dynamic: China’s political periphery is also its main economic engine.

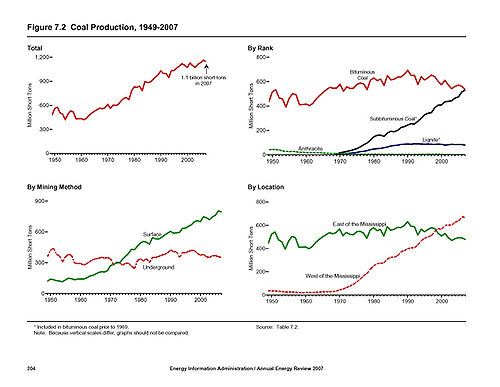

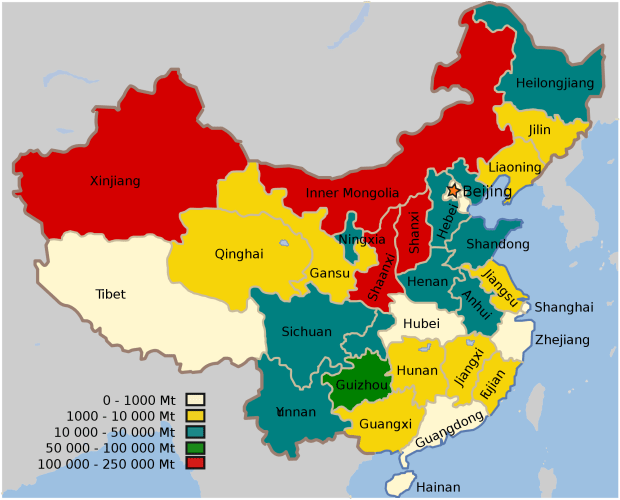

Fossil Fuels

As it happens, northern China produces almost all of China’s fossil fuels. Most Chinese energy is, in fact, produced in and around the province of Shanxi, 300 km or so west of Beijing, where a tremendous share of China’s (and, indeed, the world’s) coal is mined. Shanxi has also seen the biggest political shakeup of any province from Xi Jinping’s anti-corruption campaign thus far. When combined with the northern “Autonomous Regions” of Inner Mongolia and Xinjiang, as well as China’s north-easternmost province Heilongjiang, Shanxi produces a gigantic of China’s fossil fuels in general. Other northern areas, such as Shandong, Liaoning, and Tianjin, are also significant oil producers.

Southern and central China, in contrast, account for most of China’s imports of fossil fuels—especially if you include the economy of Taiwan as being part of southern China. Taiwan, in fact, may be more dependent on oil imports than any other significant economy in the world, according to data from the Wall Street Journal. Falling energy prices may weaken the historical political heartland of China relative to its periphery, in that case. Whether or not this will generate political instability going forward remains to be seen.

Looking Ahead

If (a big if) energy prices remain low for a sustained period, then the question of China’s future dependence on imported energy also becomes relevant, as does the question of the future dependence on imported energy of China’s most important neighbours. In that case, how dependent on energy imports will countries like China, Japan, and India be in a decade or two from now?

While it is impossible to know what the future will be like, it is not difficult to imagine that China will remain less dependent on energy imports than India and/or Japan during the years or decades ahead, as a result of India’s still-emerging economy and Japan’s still-roboticizing economy.

China is not likely to be a major adopter of energy-intensive robots, in per capita terms, because China has a far larger cheap labour force than any country in the world apart from India. Japan, in contrast, will likely help lead the robot revolution, as its labour force is expensive and aging rapidly. This could make Japan even more dependent on importing energy, as machines that are both highly mobile and capable of sophisticated computation require an enormous amount of energy to run — and indeed, one of their main advantages over human labour is that they can and frequently will be tasked to run 24-7, without even taking any time off for holidays or sick days.

China is not certain to increase its energy imports nearly as much as less-developed economies like India, meanwhile, as the Chinese inudstrial sector is facing challenges as a result of its past generation of energy-intensive growth. China faces rising labour costs in many of its cities; a pollution problem; a US that is concerned with Chinese industrial power; and countries throughout the world afraid of China’s world-leading carbon emissions.

In addition, China is located much further away from the Persian Gulf and Caspian Sea oil and gas fields than the Indians and other South Asians are, and so might have difficulty accessing them in a pinch.

China may also, for the first time, have to face industrial competition from resource-rich economies such as Australia, Norway, Canada, Texas, or even the Gulf Arab states,which may be able to use energy-intensive robots of various kinds to build up their manufacturing sectors in spite of their small, expensive domestic labour forces.

All this could make China’s industrial growth rate slip, which in turn might reduce China’s resource imports and thus prevent China from becoming the leading beneficiary of low energy and commodity prices.

Such a shift will be especially likely if the United States or European economies decide to enact tariffs on goods coming from places that generate power by using coal in inefficient ways, a prospect that has become increasingly likely as a result of America’s triple-alliance between environmentalists opposed to coal consumption, shale gas producers competing with coal miners, and energy companies trying to pioneer more expensive but cleaner ways of consuming coal and other fossil fuels. China may then have to focus on growing its service sectors instead of its energy-intensive industrial sectors.

China, Japan, and Siberia

Japan, lastly, might benefit from Russia’s energy-related woes more than China will. This is not only because the Chinese have to a certain extent often looked to Russia as an ally against the West, but also because the areas of Russia that China is close to are mostly irrelevant to China: they are landlocked, Siberian, and for the most part located far from China’s population centres.

Pacific Russia, in contrast, which is located next to the Sea of Japan on the East Asian side of Russia’s Pacific mountain ranges, has a far more liveable climate than does most of the continental Siberian interior. It is home to several small or medium-sized port cities, such as Vladivostok and Petrapavlovsk-Kamchatsky, which are very, very far away from Moscow. This region accounts for much of the oil and nearly all of the Russian gas exports to Asia—especially energy-rich Sakhalin Island, which is just 40 km away from Japan and was half-owned and inhabited by the Japanese prior to the Second World War.

Russia may, in fact, be somewhat better prepared to fight another border war with China like it did in 1969—which might not be too different than the many other wars Russia has fought within or near its borders both prior to or since then—than it would be to face off against Japan again within the far-eastern, mountainous, archipelagic and peninsular Pacific Russian region, as it did in 1905 and then again during the 1930s and WW2. Of course this does not mean Japan will attack Russia — though it has certainly toyed with the idea of eventually making some bolder moves in the Southern Kuril Islands, which both countries claim as their own. Even the remote, unstated possibility of conflict, however, may help grant Japan leverage in any negotiations with Russia regarding commercial or political issues.

Conclusion

All of this is not to be bearish on China’s future. Energy-intensive industrial growth, after all, woud not necessarily mean an improved quality of life for Chinese citizens. Ideally Chinese standards of living will rise at a considerably faster pace than its energy usage. It does seem, though, that China’s economy may not turn out to be a major beneficiary of the fall in energy prices. The PRC’s neighbours on the other hand, such as Japan and Taiwan, which are less rich in fossil fuels or in labour, may benefit greatly. So too might the poorer countries that depend on energy imports, like India and the Philippines. Just as important, however, yet often overlooked, are China’s domestic geopolitics. Internal Chinese divisions—including along north-south and east-west lines—have been, and might remain, of paramount importance. Energy prices could impact them too.

American coal companies’ stock prices have crashed in recent years, in response to the triple-whammy punch that is the US fracking boom, the environmentalist movement, and the slowdown in the Chinese industrial economy. As recently as January of 2016, the Dow Jones US Coal Index had lost around 92 percent of its market value since mid-2014, more than 97 percent of its value since 2011, and more than 98 percent of its value since its all-time peak in 2008.

Now, it may be that coal really is finished as a major industry in the US, but there is no reason to be certain about this. The market’s plunge is arguably more a sign of investor panic than of rational valuation: coal still accounts for around a third of US electricity generation and close to 40 percent of electricity generation worldwide. The economic outlook for the coal industry does not seem to have collapsed to the extent the Dow Jones US Coal index might suggest.

1. Climate Change

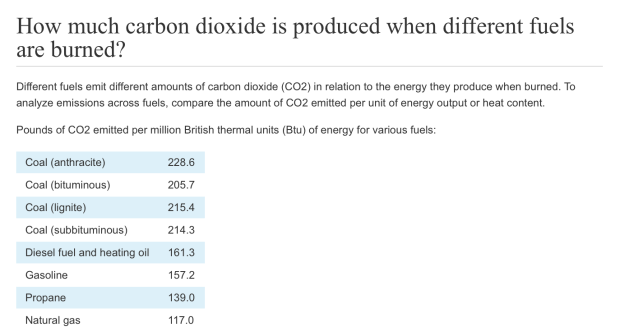

Burning coal is generally considered to be around twice as carb0n-intensive as burning natural gas. Carbon dioxide, however, is hardly the only culprit where climate change is concerned. Methane emissions are also a crucial component to climate change, for example, and industries like natural gas and meat production can be more methane-intensive than coal.

Thus far the natural gas industry, food industry, and many in the US government have neatly sidestepped the methane issue, refocusing American public attention toward carbon dioxide. They have done this by using the “we need to protect the planet for the sake of our grandchildren and future generations” approach. Methane emissions, after all, only contribute directly to global warming for a few years or decades at a time, whereas carbon dioxide can remain in the atmosphere for many centuries.

The truth, though, is probably that this is deliberately misleading. Future generations may be perfectly capable of handling whatever climate change comes their way, or of removing carbon dioxide from the atmosphere. The really dicey climate change period is more likely to occur within the coming years or decades, when the world is not yet technologically advanced enough to protect vulnerable human (and animal) populations. Within such a time frame, emissions of gasses like methane can be even more impactful than carbon dioxide.

Today US methane emissions, measured in kilotons of CO2 (carbon dioxide) equivalent, are around ten percent as high as carbon dioxide emissions. Since the impact of each kt equivalent of methane upon global warming can be up to 80-90 times higher than carbon over the course of a twenty-year period, however, the overall effect of methane emissions can perhaps be worse for climate change than carbon emissions can.

Indeed, while the direct impact of methane fades over time, the indirect impact of methane emissions could remain for decades if they help to trigger a global warming feedback loop; for example, if it helps to cause sun-reflecting polar ice to melt, which could warm the planet and so cause even more polar ice to melt.

Thus, methane emissions arguably deserve more public attention and regulation. And if they are regulated, it may weaken the natural gas industry relative to the coal industry, as the gas industry in the US accounts for almost triple the methane emissions that coal does. Just this month, the US federal government has launched its first ever package of methane emission regulations for the oil and gas sector.

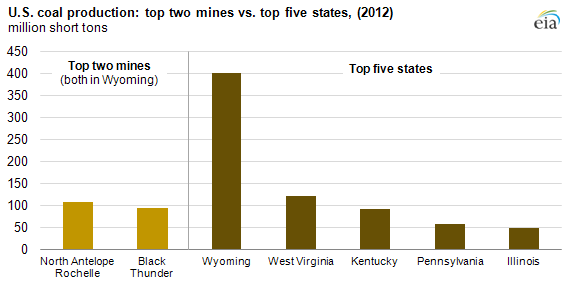

Methane, which is the main component of natural gas, can also be captured and then stored or used to produce energy. Capturing methane from the natural gas industry, however, is extremely difficult to do, because the gas sector is diffuse, consisting of hundreds of thousands of wells spread across dozens of states as well as in offshore fields in the Gulf of Mexico. Capturing and making use of methane that is released from coal mines could perhaps be easier to do, since coal production is more concentrated than gas or oil. There are only about 1000 or so coal mines in the country, and they are located mostly in Wyoming or the Midwest.

Another thing to note is that while burning natural gas is only a bit more than half as carbon-intensive as coal, much of the natural gas production in the United States comes as a byproduct of drillers trying to produce oil. This means that US gas is actually more carbon-intensive than it seems, since it would not be produced as much if the US was not also producing so much oil, and oil (or gasoline) is more than three-quarters as carbon-intensive as coal is.

This also raises the question: will the price of oil in the US remain low? If it does, it is likely to result not only in a reduction in oil production, but also in natural gas production (again, because natural gas is frequently a byproduct of oil), which in turn could cause coal to become more competitive relative to natural gas.

Oil in the US is used mainly for transportation, so it is possible that the revolutions now taking place in the transportation sector – for example, Uber (and companies like Uber), UberPool, Zipcar, electric vehicles, hybrids, e-commuting and e-commerce, using smartphone apps to make express busses finally become feasible, being able to watch a movie or do work on your smartphone or tablet while you are taking public transit or being carpooled, and the development of self-driving vehicles – could lead to such a reduction in oil use.

In the case of electric or hybrid vehicles, this could also lead to a major increase in electricity usage, potentially helping the coal industry at the expense of the oil and gas industry. And while electric cars may not soon be appearing in every driveway, it may not be too long before a widespread network of electric or hybrid Uber-esque vehicles and Zipcar-esque vehicles come into place.

If, moreover, self-driving vehicles do become a reality as well at some point, it could make vehicle-sharing services like Uber and Zipcar even more competitive, and could allow electric Uber vehicles and Zipcars to drive themselves to (and wait in line at) the nearest battery-charging station. This is an important factor, given that fully charging an electric vehicle often takes several hours.

—

Of course, many people think that coal is likely to lose out not only to natural gas, but also to alternatives like solar energy, which emit relatively little carbon dioxide, methane, or any other type of greenhouse gas. However, it is still not clear when or if industries like solar will be able to compete on a large scale with coal in developed economies like the United States.

Much has been made about the falling cost of solar panels They are often said to have become more competitive as a result of technological improvements, and are expected to continue doing so going forward. In fact there is an alternative plausible explanation about what has driven the falling cost of solar panels: government support in East Asia (especially China), Europe, and to a lesser extent North America. The solar industry may have benefited from attempts by governments in these regions to stimulate their slowing industrial sectors and reduce pollution at the same time.

If this explanation is true, then it is possible that the cost of solar panels going forward will not continue to fall as much as people now expect them to. Indeed, if China’s economy has the “hard landing” some fear it will, panel prices could even rise a lot as solar panel manufacturing output collapses.

Ultimately, though, climate change threats will continue to hamper the coal industry, unless at least one of two things happen. The first is large-scale carbon capture and storage. Though carbon capture and storage has been over-hyped in recent years , it cannot be ruled out entirely either. We will discuss this further below.

The second is climate change fatalism. If it becomes accepted that we already well past the point of being able to reverse global warming, then the priority could shift away from reducing carbon emissions and instead become achieving rapid economic advances in order to pay for the huge, global effort that adapting to climate change will entail. Ironically, coal could be employed as the cheap, plentiful resource used to spur such rapid economic growth. If this sounds a bit crazy, bear in mind that it is the approach that India and China are already implicitly (and at times explicitly) embracing at the moment. India in particular is still planning on building many new coal plants in an attempt to achieve economic growth.