How can one measure China’s stability? In the West, it is common to look to Hong Kong and Tibet as litmus tests of the strength of the central Chinese government. While it is true that Hong Kong and Tibet are important places — Hong Kong because it one of China’s major financial and service centres, Tibet because it encompasses around 15 percent of China’s territory and contains the headwaters of China’s, India’s, and Southeast Asia’s most important rivers — the inhabitants of Hong Kong and Tibet do not even account for 1 percent of China’s overall population.

To get a better sense of China’s political stability, then, one must also examine the other areas of China where the dictates of the central government in Beijing are most likely to be resisted. Arguably, these include the following seven areas: the Sichuan basin, Southwestern China, Southeastern China, Northeastern China (formerly known as Manchuria), the Shanghai Municipality, and the “Autonomous Regions” of Xinjiang and Inner Mongolia.

With the exception of Shanghai, not a single person born in any of these areas has become the ruling General Secretary of the Communist Party of China or the Premier of the People’s Republic of China. And yet, taken together, these areas have a population of almost 600 million people – close to half of China’s total population. So, let’s take a brief look at each one of them:

The Sichuan Basin – Population: 111 million

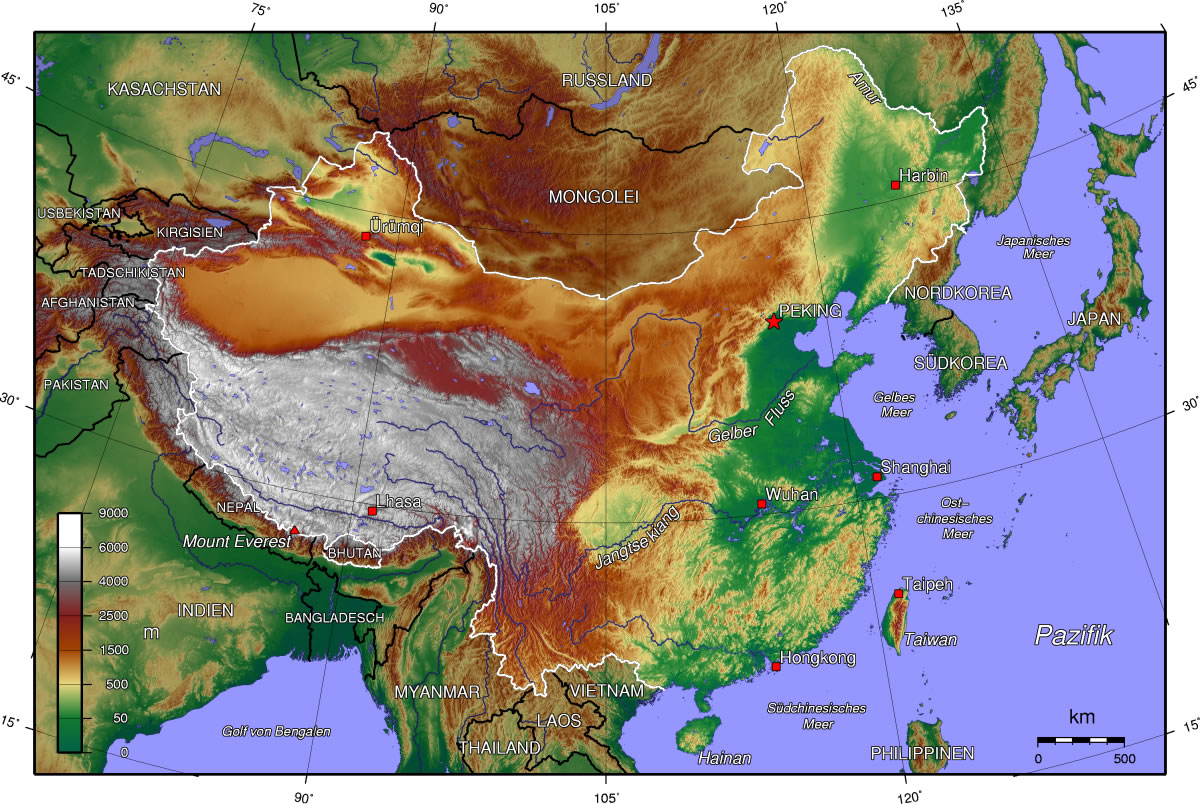

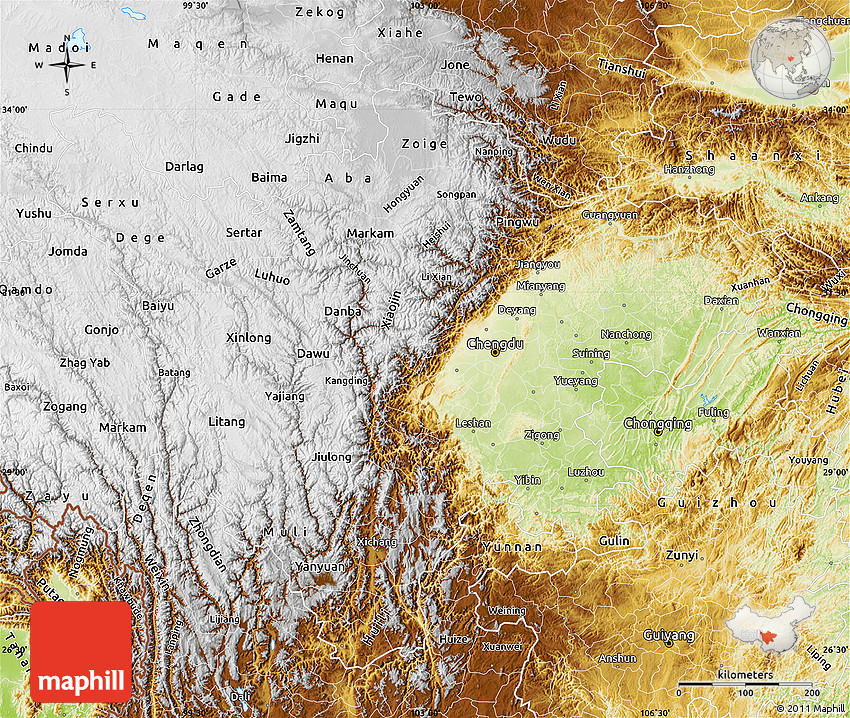

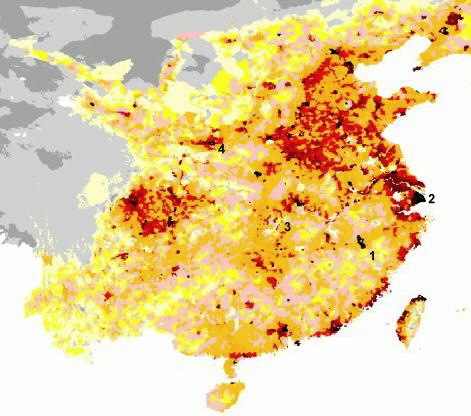

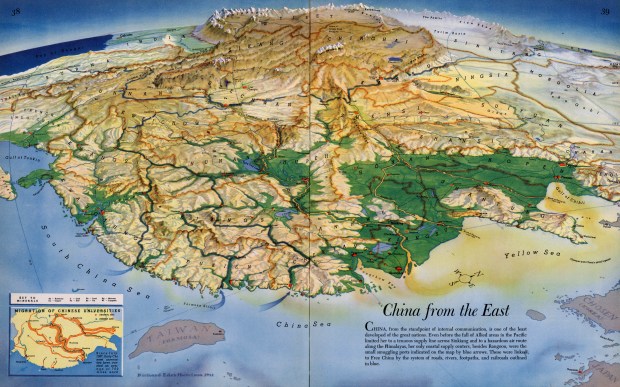

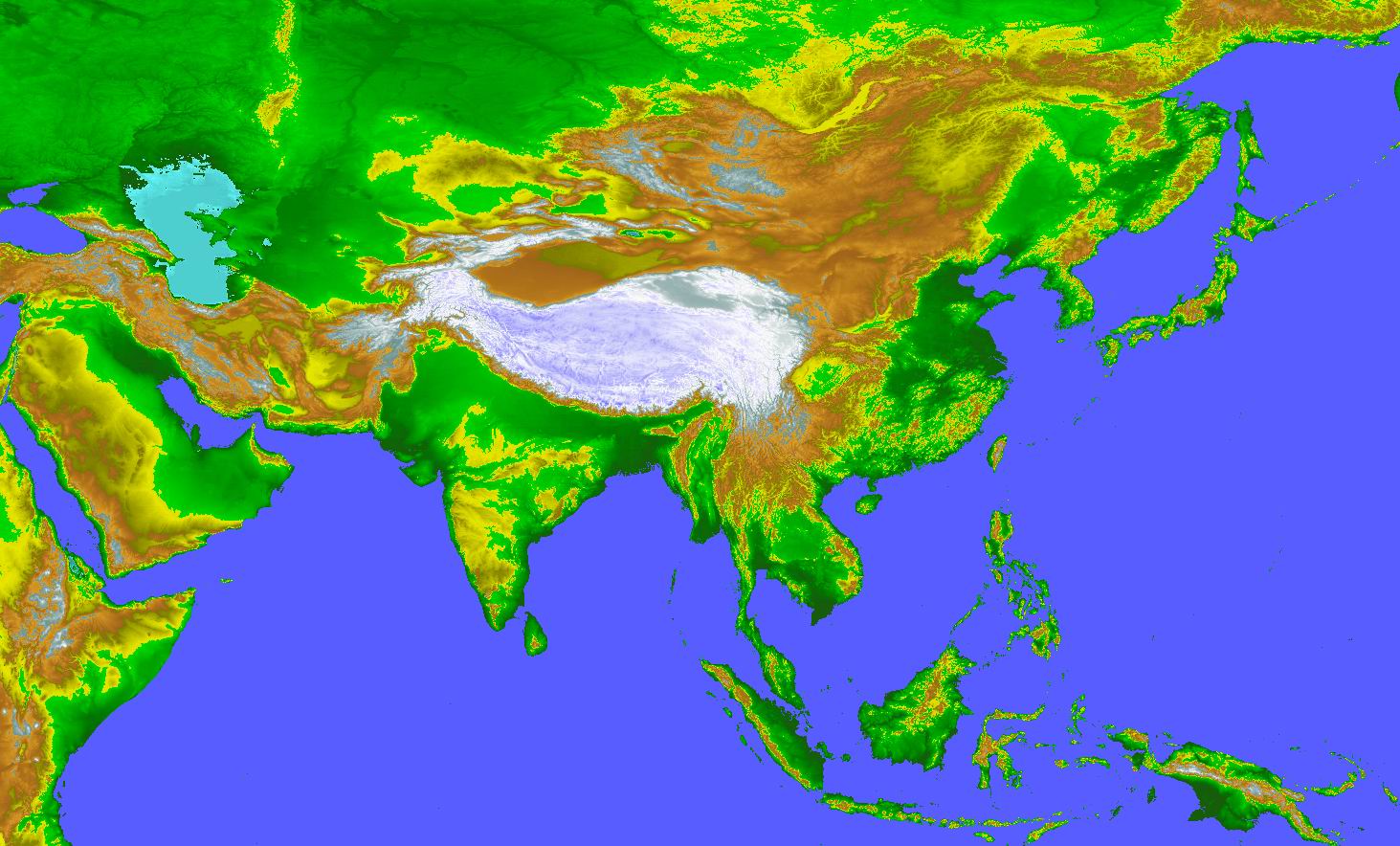

See that red circle in the centre of China’s population density map (pictured below), and the greenish-yellow circle in the centre of China’s physical topography map (pictured below that)? That is the Sichuan basin, which consists of the province of Sichuan (population 81 million) and the city-state of Chongqing (population 30 million).

Close up topography of the Sichuan basin and surrounding areas:

To the west of the Sichuan basin is the sparsely populated Tibetan plateau, which is more than 4000 metres higher above sea level than Sichuan is (to put that into context, the tallest building in Manhattan is only 540 metres tall). South and southeast of Sichuan there are mountains and plateaus that are about 1000 metres higher than Sichuan. To the east there are also mountains, which separate Sichuan from the middle reaches of the Yangtze River valley, where the elevation is about 350 meters below that of Sichuan. And to the north there are a series of high mountain ranges and narrow valleys that have historically helped to insulate Sichuan from the northeastern coastal plain where most Chinese people live.

The Sichuan basin’s geographic insularity and large population (larger than any single Chinese province) have historically made it one of China’s more independent-minded regions. In the 3rd century AD, for instance, during China’s famous Three Kingdoms era, a state basically corresponding to modern-day Sichuan was one of China’s three independent political entities (see left map below). A somewhat similar thing occurred in the 10th century AD (see right map below).

More recently, Sichuan played a significant role during the Xinhai Revolution just prior to WW1, which overthrew China’s last emperor, and during the “Warlord Era” which followed it. Sichuan then became a critical component of the Communist Party’s rebellion against the ruling Chinese Nationalists during the Chinese Civil War from 1927 – 1950. Mao’s infamous “Long March” went through the outskirts of Sichuan province, for example, and one of the two largest original Communist armies during the Civil War, led by Mao’s rival Zhuang Guotao, was based there as well. Finally, after the Communists turned the tables on the Nationalists, gaining the upper hand in the Civil War, Sichuan ended up becoming the last base of the Chinese Nationalist leadership prior to its retreat to the island of Taiwan in 1949.

Sichuan, in other words, often became a centre of resistance against whichever group, whether Chinese or foreign, happened to be ruling China at the time. Indeed, when the Japanese controlled much of China during WW2, Chongqing even became the official capital city of the parts of China that were still free of Japanese control (see map above). Much more recently, during the protests of 1989, there were actually two, rather than just one, major government crackdowns: one in Beijing’s Tiananmen Square, which most people in the West have heard of, and the other in Sichuan’s capital city of Chengdu, which very few people have heard of.

While it is difficult to speculate on the extent to which the Sichuan region may become a nuisance for China’s central government in the future, there have arguably been some troubling signs of late. Most notably, the two most prominent “purges” of high-ranking Communist Party leaders in recent times were both from the Sichuan basin.

The first was Bo Xiliai, the leader of Chongqing, who many had thought might become China’s next top leader, but instead was exiled from the Communist Party and given a life sentence in prison on a corruption charge in 2012, following a curious, alleged incident involving his wife, the Chongqing chief of police, and the murder of a British businessman.

The second was Zhou Yongkang, the former leader of Sichuan province, who was arrested on corruption charges in late 2014, only a few months ago, becoming the first member of China’s seven-person Politburo Standing Committee (the top leadership of the entire country) to be expelled from the Party since the 1980s. Many of Sichuan’s other top leaders have recently been targeted by the central government on corruption investigations as well, because of their associations with Zhou. Of course, the fact that Bo and Zhou were both the most powerful modern leaders the Sichuan basin has seen might just be a coincidence, having more to do with personal politics within the Communist Party than regional geopolitics within China as a whole. But it is somewhat suspicious nonetheless.

Politically, in spite of the region’s large population, not one person born in Sichuan or Chongqing currently holds a position in any of the 43 positions in the Communist Party’s Politburo, Secretariat, or Central Military Commission, at or around the top levels of China’s political hierarchy.

And yet, all of the previous recent Communist Party leaders of Chongqing (none of whom were actually born in the region) have gone on to some of the top jobs in the entire country. Three of the past four have even become members in China’s Politburo Standing Committee, the 7-man group which de facto holds the highest Party positions of all. And before them, Deng Xiaoping, by far the most infamous post-WW2 Chinese leader apart from Mao, served as Mayor of Chongqing, and was born in one of its suburbs. (Though in Deng’s day Chongqing was more important in China than it is today, since its insular location had allowed it to serve as the capital city of “Free China” during the Japanese occupation of eastern China in WW2).

The promotion of former party chiefs of Chongqing (but not Sichuan, even though Sichuan is much larger) to top positions in the central government in Beijing might also be just a coincidence. It does, however, seem suspiciously like a divide and conquer tactic the government has been using to keep Sichuan and Chongqing apart, by winning Chongqing’s favour. Chongqing holds a particularly strategic position, as it is the spot where the Yangtze River flows out of the mountain-enclosed Sichuan basin, entering into the rest of central China and eventually reaching Shanghai on the Pacific.

Indeed, the reason Chongqing was even made a city-state to begin with — one of only four city-states within mainland China, the others being Beijing, Shanghai, and Beijing’s port city of Tianjin — may be because China’s leaders were worried about having to deal with a politically united Sichuan basin, which prior to Chongqing’s independence from Sichuan in 1997 had been China’s most populous province. This is probably also why the “Municipality” of Chongqing, unlike those of Shanghai, Beijing, or Tianjin, is the only one to have been given large rural areas around it to govern, so that it controls a population of 30 million even though its urban areas are home to around just 10 million.

The current Party chiefs of Chongqing and Sichuan are two of the youngest in the entire country. They are 51 and 58 years old, respectively; most other provincial party chiefs in China are in their sixties or seventies, and the 51-year-old Chongqing leader is actually the youngest of all 25 current members in the country’s Communist Party Politburo. Having the youngest provincial party chiefs or governors is usually not a good sign, since Beijing tends to pick the youngest, most ambitious governors for areas it is most concerned with, the idea being that such governors will be willing to do whatever is necessary in order to maintain order, so that they can later be promoted to one of the Communist Party’s highest offices. Hu Jintao, for instance, had served as the party chief of Tibet prior to becoming a major political figure. Indeed, we will continue to see the pattern of relatively young and ambitious party chiefs and governors in the other potentially trouble-making regions we will discuss in this article.

Finally, also notable is the Sichuan Earthquake of 2008. The earthquake, the epicentre of which was only about 80 km from Sichuan province’s main city of Chengdu (population 14 million), killed an estimated 80,000-90,000 people and caused an enormous amount of physical injury and property damage, leaving 5 – 15 million people homeless. It is one of the deadliest natural disasters in the world in modern times, and the deadliest in China in over three decades. By comparison, that is about 20,00 more casualties than the United States experienced in Iraq, Afghanistan, and Vietnam combined.

The Sichuan earthquake was mostly overlooked by people in the West, not only because it took place deep within the unknown Chinese interior, but also because it was overshadowed by a flurry of notable world events that took place during the months immediately following its occurrence, such as the global financial crisis, the first Obama election, the Beijing Olympics, the Russian invasion of Georgia, the first Israeli war against Hamas in Gaza, and the Mumbai terrorist attacks. The same week as the earthquake, in fact, California became the second US state to legalize same-sex marriage, and the debate discussion of this decision even got much more American news coverage than the disaster in Sichuan did.

The earthquake was, however, obviously an event of huge importance within China, and it is still quite fresh in some people’s minds. Its tenth anniversary will be approaching in 2017, the same year as China’s once-a-decade top leadership changeover. Crucially, many Chinese people believe that the central government are at least partly to blame for the earthquake (though it is difficult to know how many people believe this, given Chinese censorship). This is because the government created the gigantic nearby Three Gorges Dam, which finished being constructed just prior to 2008, and many think the weight of the dam – which can produce almost twice the electricity of any other dam in the world – and the reservoir of water it created was the catalyst for the earthquake. (Even before the earthquake, the Dam crushed the previous record for people displaced from their homes by a hydroelectric plant: the number of displaced Chinese was estimated at more than 1.2 million people, most of them from the province of Hubei, which directly borders the Sichuan basin).

And the thing about earthquakes is, of course, that you never fully know when another one is going to happen. If a second large one were to occur and affect Sichuan, it could bring back the memory of 2008 – and potential Sichuanese anger with the central government – along with it. In fact, this may have already happened to a certain extent: China’s highest-magnitude earthquake since the Big One in 2008 occurred again in Sichuan, in 2013, only about 115 km from Chengdu. It killed an estimated 200 people (according to the Chinese government) and injured more than 10,000.

Southeastern China — Population 154 million

In a previous article, we discussed a large number of differences between southern China, where nearly all of the country’s tens of millions of ethnic minorities and hundreds of millions of linguistic minorities live, and northern China, where most of the country’s enormous majority of ethnic Chinese and Mandarin speakers live. So we will try to repeat only some of the basic facts of the region that were discussed there, and then focus specifically on why this part of China could potentially become the most problematic region for the Chinese central government to handle.

Southeastern China consists basically of three provinces: the province of Guangdong (population 107 million), which has the largest population and economy of any Chinese province, and which is the only province which borders Hong Kong; the province of Fujian (population 38 million), which is located directly across the 180 km long Taiwan Straits from Taiwan, speaks the same dialect of Chinese as is spoken in Taiwan, and, in spite of having less than 3 percent of China’s total population, accounts for perhaps 15 percent of all China’s trade with Taiwan (and China trades roughly 40 percent as much with Taiwan alone as it does with the entire US); and finally the province of Hainan (population 9 million), which is the only island province in China. The first bridge linking Hainan to the Chinese mainland (specifically, to Guangdong), is supposed to be finished between 2016 and 2020, and is likely increase Guangdong’s level of influence on the island.

As you can see from the population density map below, southeastern China is very different from northern China, in that its population centres are almost entirely situated on the country’s Pacific coast. The reason for this is that southern China, unlike northern China, has a very difficult climate and topography to deal with – it is extremely hilly, mountainous, often forested, and sub-tropical (see the other two maps below) – so that its population has moved to the only places where economic development was not extremely difficult to achieve, namely the narrow coastal flatlands that sit next to its numerous natural harbours.

or, for a different perspective of the topographic differences between southeastern China and central-eastern China:

Because southern China’s challenging geography has tended to impede internal movement of people and goods – especially in the past, but to a decent extent also in the present – southeastern Chinese coastal cities have also become relatively close to, and dependent on trade with, the outside world, with foreign economies like Japan, the United States, Canada, and Europe, as well as with Taiwan. The relationship between Hong Kong (population 7.2 million) and Britain is of course the most obvious and significant example of this, but it is not the only one. Macau (population 600,000), for instance, on the borders of Guangdong, is a former Portuguese territory that is China’s only “Special Administrative Region” apart from Hong Kong. Macau is also by far the wealthiest of any political subdivision within China, with a per capita nominal income of more than $90,000.

According to the Economist, Guangdong and Fujian alone account for 30-40 percent of all Chinese exports. Most of China’s gigantic global diaspora – which is 50 million strong, perhaps, and is located all over the world, but particularly in places like North America, Australia, Peru, and especially Southeast Asia – is also from Southeastern China. In fact, it has been estimated that one out of every seven Chinese Americans have their roots in the Guangdong area of Taishan, even though Taishan itself only has around 1 million inhabitants today. More recently, in the 1980s, emigrants from Taiwan and Hong Kong came to countries like the US and Canada in very large numbers. If, therefore, globalization forces continue to deepen, and if the economies of Southeast Asia and Taiwan continue to emerge, it could have a huge influence on this part of China, in a sense pulling it away from the rest of China.

Southeast Asia alone is home to an estimated 27 million Chinese people (though admittedly, these statistics vary widely depending on which numbers you trust, and on which criteria you use to define who is and is not “Chinese”, since many have been living in Southeast Asia for many generations now). Southeastern China also directly borders a potentially rapid-growing Vietnamese economy, the capital city of which, Hanoi, is only about 100 -150 km from the southeastern Chinese border, only 400 km from Guangdong’s enormous capital city Guangzhou and Hong Kong, and only 250 km from the Chinese island province of Hainan.

Along with the adjacent provinces of Hunan, Jiangxi, and Zheijang, Southeastern China also has by far the most intra-Chinese linguistic diversity in the country. In it, non-Mandarin Chinese languages are spoken by an estimated 300 million people (though increasingly, most people are also able to speak the standardized, Beijing-region dialect of Mandarin) — see map below. Like Sichuan, this region has also been politically disenfranchised to a certain extent, with not a single one of China’s 43 positions in the Party’s Politburo, Secretariat, or Central Military Commission held by someone born in Guangdong or Hainan, and only one held by someone born in Fujian. Currently Beijing has also given Guangdong the second youngest party chief (aka party secretary) in the country, a 51-year-old who has spent most of his career working in Tibet.

Recently, this region has also been slowing economically as a result of the effect that Europe’s and Japan’s stagnant economies have had on demand for its exports. As a result, and also given the recent (and perhaps ongoing) protests in neighbouring Hong Kong, the province of Guangdong should be watched very closely at this time.

Historically, to be sure, Southeastern China has been a huge pain for Chinese central governments. From roughly 200 AD to 500 AD and from 1000 AD to 1200 AD, for example, there was a general north-south political divide in China (see maps below).

In modern times, during the anti-emperor Xinhai Revolution prior to WW1, Guangdong and Fujian were two of the original centres of the revolution. Later, in 1925, the Chinese Nationalists (the Kuomintang) set up an alternative Chinese capital city in Guangzhou, Guangdong, and from it successfully led a campaign to overthrow the government in Beijing, at which point the Chinese capital was moved to Nanjing (next to Shanghai).

Only a few years after that, in 1930, there was a very deadly civil war within China, the Central Plains War, which among other things pitted Nationalist leader Chiang Kai-Shek, who was ruling out of Nanjing, against Hu Hanmin, who had the support of the Nationalists across Guangdong and the rest of southern China. This rivlary had in fact been presaged by an earlier one in 1922, when the top Nationalist leader at the time, Sun Yat Sen, was forced to flee Guangdong from a different, more regional-minded Nationalist leader, Chen Jiongmin.

Around the same time, the Guangdong capital of Guangzhou was also one of the main bases of the Communist movement in China. The Communists were gaining momentum across various parts of southern China: in 1933, just to give one example, an alliance between a portion of the Communist movement and a portion of the Nationalist movement emerged, leading to the Fujian Rebellion: the creation a self-governing leadership in Fujian province that aimed to overthrow the Nationalist Chinese government of Chiang Kai-Shek. The provinces of Hunan and Jiangxi, directly on the border of Guangdong, also became very important for the Communists.

Finally, when the Communists took over and were about to win the Chinese Civil War, Guangdong became the final base – along with Sichuan – of the Nationalists prior to their retreat to Taiwan.

While it is probably unwise to make generalizations about Chinese history, there does seem to be a bit of a pattern here: Guangdong, or more broadly southern China, tends to resist centralized Chinese leadership. It has always seemed to lead the anti-government movements in the country, whether it be the anti-imperial uprising against the Qing Dynasty at the begining of the 20th century, the Nationalist move to overthrow the Beiyang government (which had replaced the Qing) in the Northern Expedition, the attempt by regional leaders within the Nationalist movement to get rid of the Nationalist central government of Chiang Kai-Shek that ruled out of Nanjing, the emergence of Communist movements opposed to the ruling Nationalists (with whom they had previously been allied), or, finally, the retreat and resistance of the Nationalists in the face of the ruling Communists.

The thing which makes southeastern China so potentially difficult for the central Chinese government, however, is not so much its history as it is its wealth. If you take Guangdong and Fujian, and add in neighbouring Taiwan, Hong Kong, Zheijang, and the Municipality of Shanghai (and we will discuss Shanghai later in part two of this article), you get a coastal region with a GDP that, as recently as 2009, was approximately 80 percent as large as the rest of all of mainland China’s other provinces put together.

Such wealth not only gives southeastern China economic influence, but has also made its internal politics complicated – and potentially dangerous – through the creation of divisions between the native inhabitants of the region’s cities, and the migrants from its rural areas and from the rural areas of poorer Chinese provinces, who are in search of work in its cities. Guangdong alone has an estimated 27 percent of China’s inter-provincial migrant population. And in China, “rural-urban” is not only a geographic or demographic distinction, but also a legal designation with significant financial and social implications. Rural Chinese populations, even when they have moved to urban areas, are generally denied many of the social services, such as subsidized housing or education, which are provided for the native urban populations.

Finally, parts of central-eastern and southeastern China in recent years seem to have become the main centres of China’s potentially enormous transition toward Christianity. Today, according to the Economist, arguably more than 100 million people in China are Christian, up from perhaps as few as 15 million as recently as the 1990’s. If these numbers are accurate, then the growth of Christianity within China during the past two decades represents one of the largest religious adoptions in all of human history. The Economist more recently argued that the relationship between Christianity and the Communist Party in China has been becoming much more tense in the past year.

Neighbouring Hong Kong has long had a significant Christian population, meanwhile, and remains around 10-15 percent Christian today. A number of the Hong Kong protest organizers were practicing Christians, in fact. And, notably, the Chinese government may have begun to crack down on parts of this growing Christian religion within China during the past year or so.

Southwestern China – Population: 120 million

Southwestern China (containing the provinces of Yunnan, Guizhou, and the “Autonomous Region” of Guangxi, one of only two Autonomous Regions apart from Tibet, Xinjiang, and Inner Mongolia) is by far the most mountainous of any populous Chinese region. Partly as a result of this, it also has by far the most ethnic diversity in the country, with a regional population that contains tens of millions of non-Chinese peoples (most notably the 15 million or so Zhuang ethnic group), some of whose homelands extend across the Chinese border with Southeast Asian countries like Myanmar. Like the other regions discussed so far, southwestern China has historically been a challenge for Chinese central governments. During the 1950’s, for instance, in the largest southwestern province, Yunnan, an anti-Communist Islamic guerrilla insurgency took place, orchestrated in part by the Nationalists who were ruling Taiwan. Today, as in Guangdong or Sichuan, not one person who was born in southwestern China is currently serving within the highest echelons of the Chinese government.

Southwestern China is the only part of China to border most of Southeast Asia. It could in the future become particularly close with the northern part of Vietnam, which is nearby, populous, and can serve as an alternative route for southwestern Chinese goods to reach the Pacific. It could also become close with Myanmar, which can serve as a direct route for it to reach the Indian Ocean via the commercially navigable Irrawaddy River (see map below), or to reach India and Bangladesh overland without having to cross the virtually impassable Himalayan Mountains and Tibetan Plateau (see other map below). Notably, Vietnam and Myanmar have seen a great deal of economic growth in recent years, and Myanmar has politically been re-opening itself to the West after decades of isolation. Economic interaction between Southwestern China and these potentially emerging countries could present some challenges for the Chinese central government.

In addition, and also potentially troubling for the Chinese central government, the region of southwestern china also has ties to southeastern China via the Pearl River, which is by far China’s longest commercially navigable river apart from the Yangtze, and which meets the Pacific at the place where Hong Kong and Guangdong’s capital city of Guangzhou are located (see map below). Southwestern China also directly borders both Sichuan and Tibet.

(In the graph above: Kunming, Guiyang, and Nanning are the capital cities of Southwestern China’s provinces. The Greater Guangzhou-Hong Kong area in Southeastern China, which has a total population of perhaps more than 50 million, is arguably the most populous urban area in the entire world)

In part two of this article we will take a look at Shanghai, Xinjiang, the former Manchuria, and Inner Mongolia.

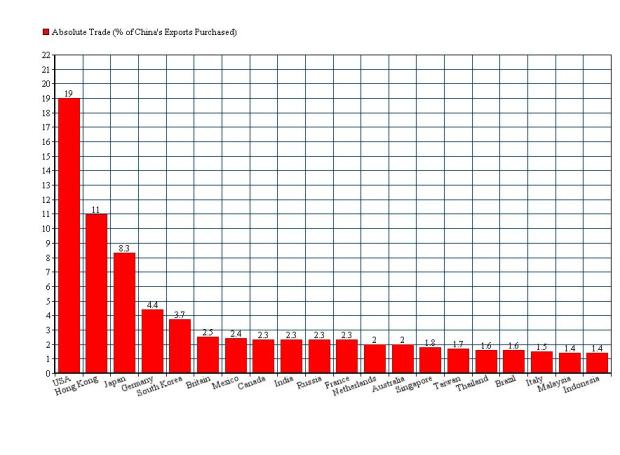

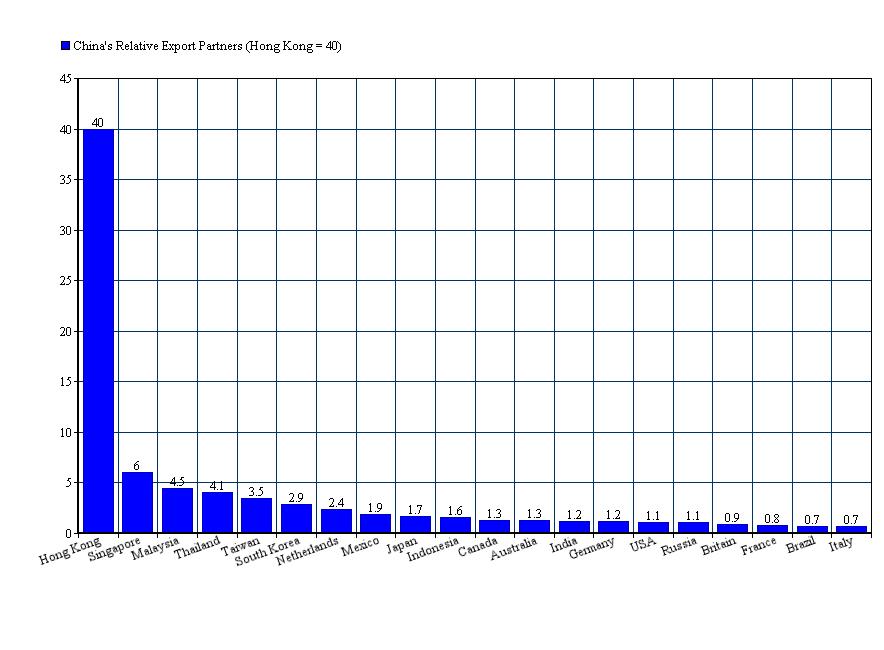

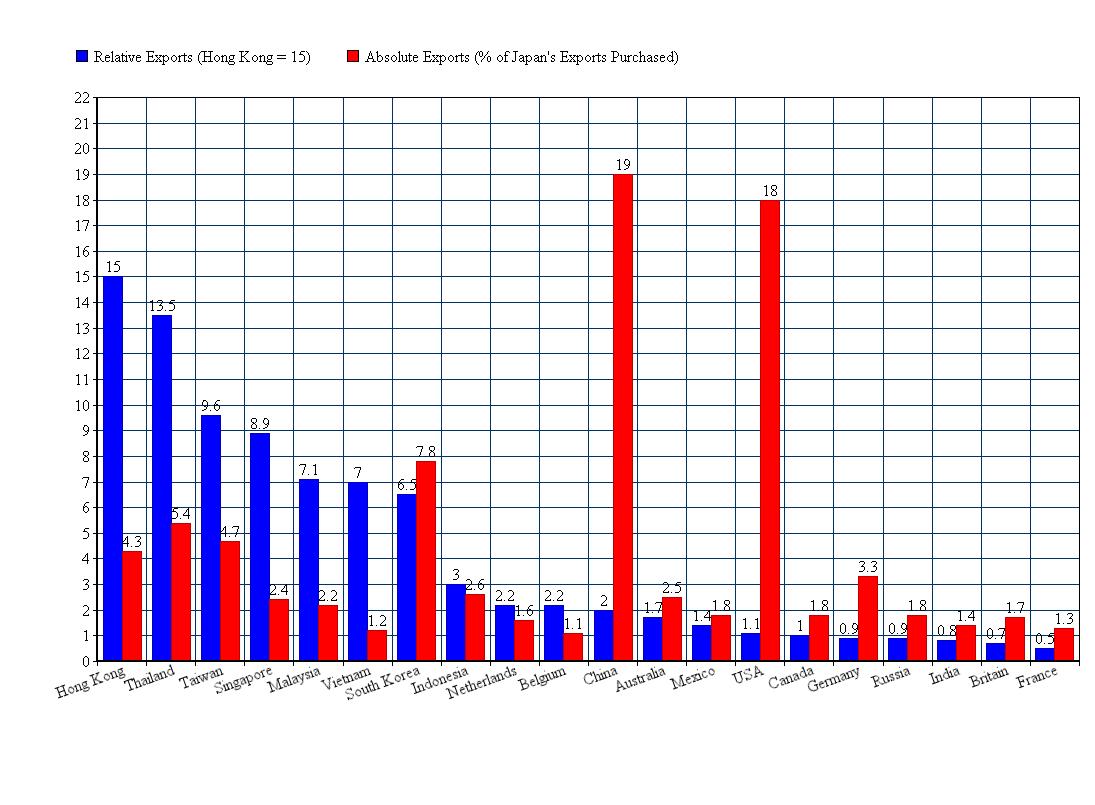

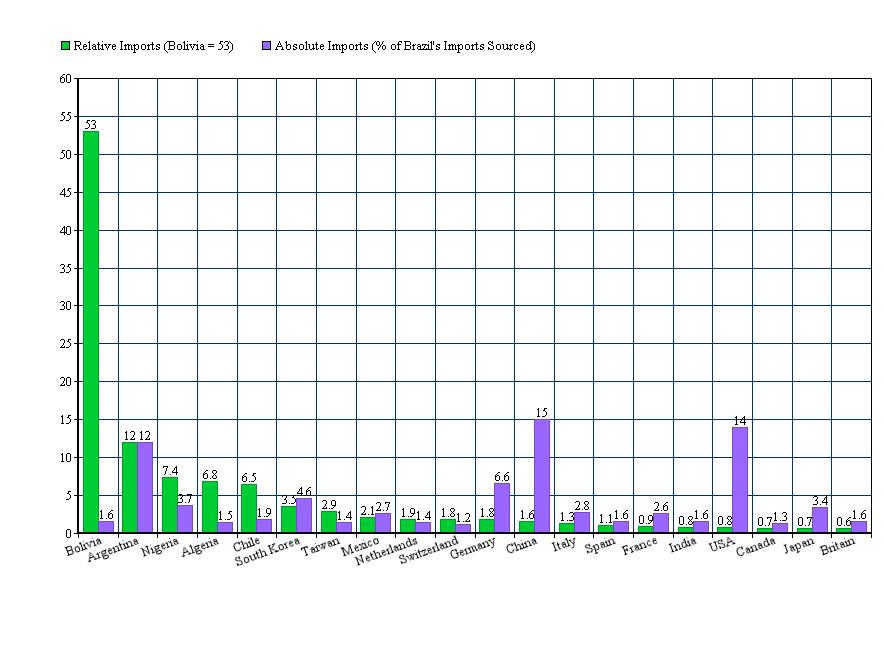

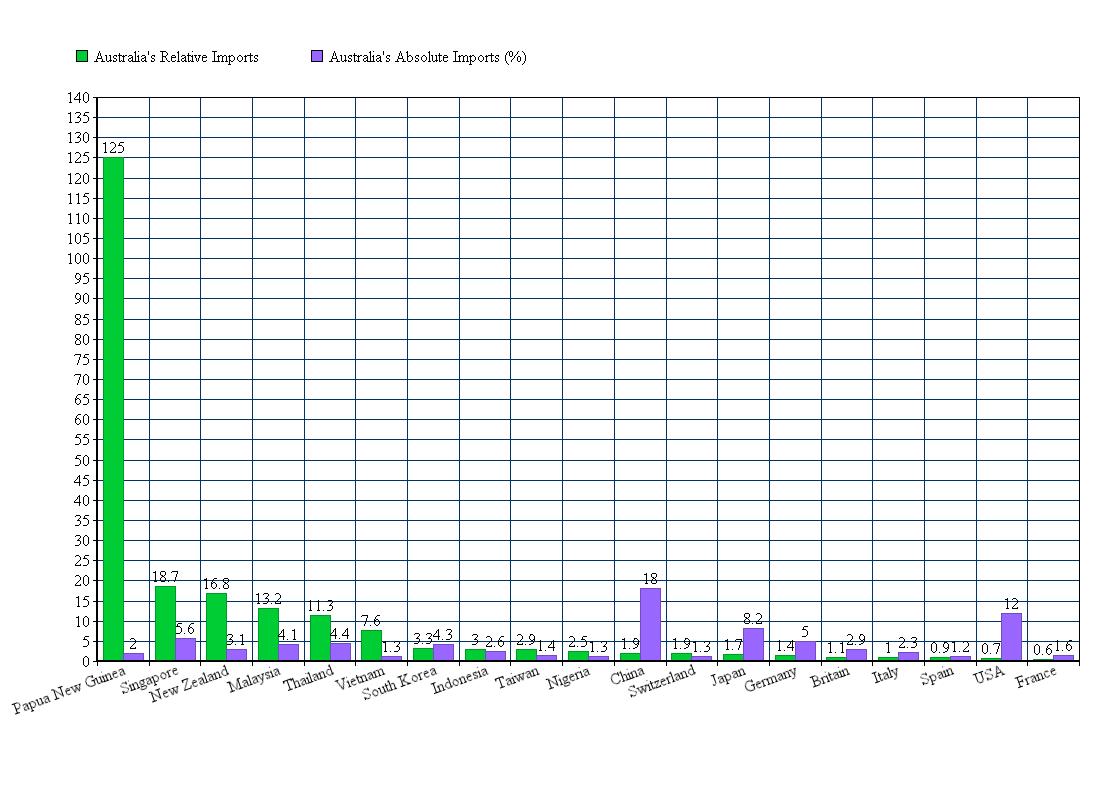

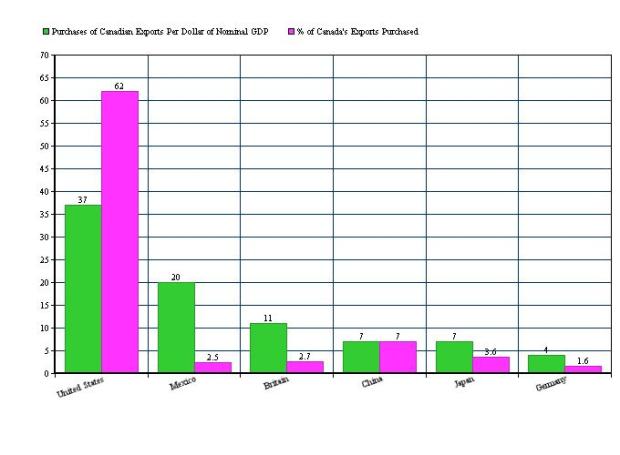

In the graph above we see China’s “absolute” export patterns – in other words, the type of trade patterns we would normally hear about in the media. The US buys an estimated 19 percent of China’s exports, Hong Kong buys an estimated 11 percent of China’s exports, Japan buys 8 percent, and so on. In the graph below, however, we see China’s “relative” export patterns, which tell a very different story:

In the graph above we see China’s “absolute” export patterns – in other words, the type of trade patterns we would normally hear about in the media. The US buys an estimated 19 percent of China’s exports, Hong Kong buys an estimated 11 percent of China’s exports, Japan buys 8 percent, and so on. In the graph below, however, we see China’s “relative” export patterns, which tell a very different story:

Challenge #2: Other Commodities

Challenge #2: Other Commodities